Royal Caribbean Cruise Lines 2014 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2014 Royal Caribbean Cruise Lines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

|

|

Royal Caribbean Cruises Ltd. 91

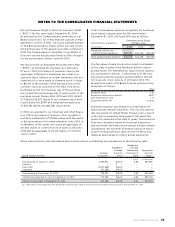

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

The following table presents information about the Company’s offsetting of financial liabilities under master net-

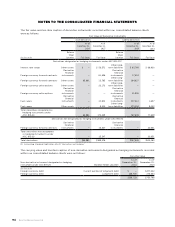

ting agreements with derivative counterparties:

Gross Amounts not Offset in the Consolidated Balance Sheet that are Subject to Master Netting Agreements

As of December 31, 2014 As of December 31, 2013

(In thousands of dollars)

Gross Amount

of Derivative

Liabilities

Presented

in the

Consolidated

Balance Sheet

Gross

Amount of

Eligible

Offsetting

Recognized

Derivative

Assets

Cash

Collateral

Pledged

Net Amount

of Derivative

Liabilities

Gross Amount

of Derivative

Liabilities

Presented

in the

Consolidated

Balance Sheet

Gross

Amount of

Eligible

Offsetting

Recognized

Derivative

Liabilities

Cash

Collateral

Pledged

Net Amount

of Derivative

Liabilities

Derivatives subject

to master netting

agreements () — () () — ()

Total () — () () — ()

DERIVATIVE INSTRUMENTS

We are exposed to market risk attributable to changes

in interest rates, foreign currency exchange rates and

fuel prices. We manage these risks through a combi-

nation of our normal operating and financing activities

and through the use of derivative financial instruments

pursuant to our hedging practices and policies. The

financial impact of these hedging instruments is pri-

marily offset by corresponding changes in the under-

lying exposures being hedged. We achieve this by

closely matching the amount, term and conditions of

the derivative instrument with the underlying risk being

hedged. Although certain of our derivative financial

instruments do not qualify or are not accounted for

under hedge accounting, we do not hold or issue

derivative financial instruments for trading or other

speculative purposes. We monitor our derivative posi-

tions using techniques including market valuations

and sensitivity analyses.

We enter into various forward, swap and option con-

tracts to manage our interest rate exposure and to

limit our exposure to fluctuations in foreign currency

exchange rates and fuel prices. These instruments are

recorded on the balance sheet at their fair value and

the vast majority are designated as hedges. We also

have non-derivative financial instruments designated

as hedges of our net investment in our foreign opera-

tions and investments.

At inception of the hedge relationship, a derivative

instrument that hedges the exposure to changes in

the fair value of a firm commitment or a recognized

asset or liability is designated as a fair value hedge.

A derivative instrument that hedges a forecasted

transaction or the variability of cash flows related

to a recognized asset or liability is designated as a

cash flow hedge.

Changes in the fair value of derivatives that are desig-

nated as fair value hedges are offset against changes

in the fair value of the underlying hedged assets, lia-

bilities or firm commitments. Gains and losses on

derivatives that are designated as cash flow hedges

are recorded as a component of Accumulated other

comprehensive (loss) income until the underlying

hedged transactions are recognized in earnings. The

foreign currency transaction gain or loss of our non-

derivative financial instruments and the changes in

the fair value of derivatives designated as hedges of

our net investment in foreign operations and invest-

ments are recognized as a component of Accumu-

lated other comprehensive (loss) income along with

the associated foreign currency translation adjust-

ment of the foreign operation.

On an ongoing basis, we assess whether derivatives

used in hedging transactions are “highly effective”

in offsetting changes in the fair value or cash flow of

hedged items. We use the long-haul method to assess

hedge effectiveness using regression analysis for each

hedge relationship under our interest rate, foreign

currency and fuel hedging programs. We apply the

same methodology on a consistent basis for assessing

hedge effectiveness to all hedges within each hedging

program (i.e., interest rate, foreign currency and fuel).

We perform regression analyses over an observation

period of up to three years, utilizing market data rele-

vant to the hedge horizon of each hedge relationship.

High effectiveness is achieved when a statistically

valid relationship reflects a high degree of offset and

correlation between the changes in the fair values

of the derivative instrument and the hedged item.

The determination of ineffectiveness is based on the

amount of dollar offset between the change in fair

value of the derivative instrument and the change in

fair value of the hedged item at the end of the report-

ing period. If it is determined that a derivative is not

highly effective as a hedge or hedge accounting is