Royal Caribbean Cruise Lines 2014 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2014 Royal Caribbean Cruise Lines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

|

|

Royal Caribbean Cruises Ltd. 87

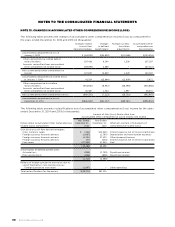

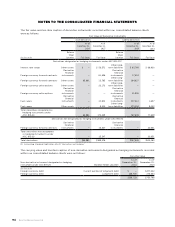

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

NOTE 11. RETIREMENT PLAN

We maintain a defined contribution pension plan

covering full-time shoreside employees who have

completed the minimum period of continuous service.

Annual contributions to the plan are discretionary

and are based on fixed percentages of participants’

salaries and years of service, not to exceed certain

maximums. Pension expenses were $15.4 million,

$13.0 million and $15.2 million for the years ended

December 31, 2014, 2013 and 2012, respectively.

NOTE 12. INCOME TAXES

We are subject to corporate income taxes in countries

where we have operations or subsidiaries. We and

the majority of our ship-operating and vessel-owning

subsidiaries are currently exempt from United States

corporate tax on United States source income from

the international operation of ships pursuant to Section

883 of the Internal Revenue Code. Regulations under

Section 883 have limited the activities that are con-

sidered the international operation of a ship or inci-

dental thereto. Accordingly, our provision for United

States federal and state income taxes includes taxes

on certain activities not considered incidental to the

international operation of our ships.

Additionally, some of our ship-operating subsidiaries

are subject to income tax under the tonnage tax

regimes of Malta or the United Kingdom. Under these

regimes, income from qualifying activities is not sub-

ject to corporate income tax. Instead, these subsidiaries

are subject to a tonnage tax computed by reference

to the tonnage of the ship or ships registered under

the relevant provisions of the tax regimes. Income

from activities not considered qualifying activities,

which we do not consider significant, remains subject

to Maltese or United Kingdom corporate income tax.

Income tax (benefit) expense for items not qualifying

under Section 883, tonnage taxes and income taxes

for the remainder of our subsidiaries was approxi-

mately $(20.9) million, $24.9 million and $55.5 million

and was recorded within Other income (expense) for

the years ended December 31, 2014, 2013 and 2012,

respectively. In addition, all interest expense and pen-

alties related to income tax liabilities are classified as

income tax expense within Other income (expense).

We do not expect to incur income taxes on future dis-

tributions of undistributed earnings of foreign subsid-

iaries. Consequently, no deferred income taxes have

been provided for the distribution of these earnings.

Net deferred tax assets and deferred tax liabilities and

corresponding valuation allowances related to our

operations were not material as of December 31, 2014

and 2013.

We regularly review deferred tax assets for recover-

ability based on our history of earnings, expectations

of future earnings, and tax planning strategies. Reali-

zation of deferred tax assets ultimately depends on

the existence of sufficient taxable income to support

the amount of deferred taxes. A valuation allowance

is recorded in those circumstances in which we con-

clude it is not more-likely-than-not we will recover the

deferred tax assets prior to their expiration. During

2012, we determined that a 100% valuation allowance

of our deferred tax assets was required resulting in a

deferred income tax expense of $33.7 million. In addi-

tion, Pullmantur has a deferred tax liability that was

recorded at the time of acquisition. This liability rep-

resents the tax effect of the basis difference between

the tax and book values of the trademarks and trade

names that were acquired at the time of the acquisi-

tion. Due to the impairment charge related to these

intangible assets, we reduced the deferred tax liability

and recorded a deferred tax benefit of $5.2 million.

The net $28.5 million impact of these adjustments was

recognized in earnings during the fourth quarter of

2012 and was reported within Other income (expense)

in our statements of comprehensive income (loss).

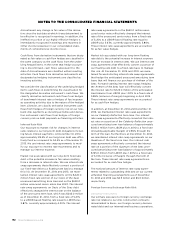

During the fourth quarter of 2014, Spain adopted

tax reform legislation, which included among other

things, a reduction of the corporate income tax rate

from 30% to 28% in 2015 and a further reduction to

25% in 2016. As a result, we adjusted our deferred tax

assets and deferred tax liabilities in Spain to reflect the

new tax rate at which we believe they will be realized.

This change resulted in a net deferred income tax

benefit of $10.0 million. The tax reform also amended

the net operating loss carryforward rules by changing

the carryforward period from 18 years to unlimited

and by changing the annual utilization limitation from

25% of taxable income to 70% of taxable income for

certain taxpayers, including Pullmantur. As a result

of the change of the net operating loss carryforward

period, we reversed a portion of the valuation allow-

ance recorded in 2012 to the extent of 70% of the

rate-adjusted deferred tax liability recorded for the

basis difference between the tax and book values of

the trademarks and trade names recorded at the time

of the Pullmantur acquisition and other indefinite lived

assets recorded. The amount of the valuation allow-

ance reversed in the fourth quarter was $33.5 million

which was recorded as a deferred tax benefit. These

deferred tax adjustments were reported within Other

income (expense) in our statements of comprehensive

income (loss).