Royal Caribbean Cruise Lines 2014 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2014 Royal Caribbean Cruise Lines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

Royal Caribbean Cruises Ltd. 79

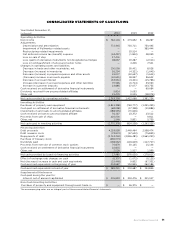

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

In 2012, we determined the implied fair value of good-

will for the Pullmantur reporting unit was $145.5 mil-

lion and recognized an impairment charge of $319.2

million based on a probability-weighted discounted

cash flow model further discussed below. This impair-

ment charge was recognized in earnings during the

fourth quarter of 2012 and is reported within Impair-

ment of Pullmantur related assets within our consoli-

dated statements of comprehensive income (loss).

During the fourth quarter of 2014, we performed a

qualitative assessment of whether it was more-likely-

than-not that our Royal Caribbean International

reporting unit’s fair value was less than its carrying

amount before applying the two-step goodwill impair-

ment test. The qualitative analysis included assessing

the impact of certain factors such as general economic

conditions, limitations on accessing capital, changes

in forecasted operating results, changes in fuel prices

and fluctuations in foreign exchange rates. Based on

our qualitative assessment, we concluded that it was

more-likely-than-not that the estimated fair value

of the Royal Caribbean International reporting unit

exceeded its carrying value and thus, we did not pro-

ceed to the two-step goodwill impairment test. No

indicators of impairment exist primarily because the

reporting unit’s fair value has consistently exceeded

its carrying value by a significant margin, its financial

performance has been solid in the face of mixed

economic environments and forecasts of operating

results generated by the reporting unit appear suffi-

cient to support its carrying value.

We also performed our annual impairment review

of goodwill for Pullmantur’s reporting unit during the

fourth quarter of 2014. We did not perform a quali-

tative assessment but instead proceeded directly to

the two-step goodwill impairment test. We estimated

the fair value of the Pullmantur reporting unit using

a probability-weighted discounted cash flow model.

The principal assumptions used in the discounted cash

flow model are projected operating results, weighted-

average cost of capital, and terminal value. Signifi-

cantly impacting these assumptions are the transfer

of vessels from our other cruise brands to Pullmantur.

The discounted cash flow model used our 2015 pro-

jected operating results as a base. To that base, we

added future years’ cash flows assuming multiple rev-

enue and expense scenarios that reflect the impact

of different global economic environments beyond

2015 on Pullmantur’s reporting unit. We assigned a

probability to each revenue and expense scenario.

We discounted the projected cash flows using rates

specific to Pullmantur’s reporting unit based on

its weighted-average cost of capital. Based on the

probability-weighted discounted cash flows, we deter-

mined the fair value of the Pullmantur reporting unit

exceeded its carrying value by approximately 52%

resulting in no impairment to Pullmantur’s goodwill.

Pullmantur is a brand targeted primarily at the Spanish,

Portuguese and Latin American markets, with an

increasing focus on Latin America. The persistent

economic instability in these markets has created sig-

nificant uncertainties in forecasting operating results

and future cash flows used in our impairment analyses.

We continue to monitor economic events in these

markets for their potential impact on Pullmantur’s

business and valuation. Further, the estimation of fair

value utilizing discounted expected future cash flows

includes numerous uncertainties which require our

significant judgment when making assumptions of

expected revenues, operating costs, marketing, sell-

ing and administrative expenses, interest rates, ship

additions and retirements as well as assumptions

regarding the cruise vacation industry’s competitive

environment and general economic and business

conditions, among other factors.

If there are changes to the projected future cash

flows used in the impairment analyses, especially in

Net Yields or if certain transfers of vessels from our

other cruise brands to the Pullmantur fleet do not

take place, it is possible that an impairment charge

of Pullmantur’s reporting unit’s goodwill may be

required. Of these factors, the planned transfers of

vessels to the Pullmantur fleet is most significant to

the projected future cash flows. If the transfers do not

occur, we will likely fail step one of the impairment test.

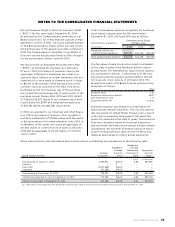

NOTE 4. INTANGIBLE ASSETS

Intangible assets are reported in Other assets in our

consolidated balance sheets and consist of the follow-

ing (in thousands):

Indefinite-life intangible asset—

Pullmantur trademarks and

trade names

Foreign currency translation

adjustment ()

Total

During the fourth quarter of 2014, 2013 and 2012, we

performed the annual impairment review of Pullmantur’s

trademarks and trade names using a discounted cash

flow model and the relief-from-royalty method to

compare the fair value of these indefinite-lived intan-

gible assets to its carrying value. The royalty rate

used is based on comparable royalty agreements in

the tourism and hospitality industry. We used a dis-

count rate comparable to the rate used in valuing the

Pullmantur reporting unit in our goodwill impairment

test. Based on the results of our testing, we did not