Royal Caribbean Cruise Lines 2011 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2011 Royal Caribbean Cruise Lines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

|

|

2011 ANNUAL REPORT 44

PART II

we do not believe that reconciling information for such

projected figures would be meaningful.

Net Debt-to-Capital is a ratio which represents total

long-term debt, including current portion of long-term

debt, less cash and cash equivalents (“Net Debt”)

divided by the sum of Net Debt and total shareholders’

equity. We believe Net Debt and Net Debt-to-Capital,

along with total long-term debt and shareholders’

equity are useful measures of our capital structure.

A reconciliation of historical Debt-to-Capital to Net

Debt-to-Capital is provided below under Results

of Operations.

Net Revenues represent total revenues less commis-

sions, transportation and other expenses and onboard

and other expenses (each of which is described under

the Description of Certain Line Items heading).

Net Yields represent Net Revenues per APCD. We uti-

lize Net Revenues and Net Yields to manage our busi-

ness on a day-to-day basis as we believe that it is the

most relevant measure of our pricing performance

because it reflects the cruise revenues earned by us

net of our most significant variable costs, which are

commissions, transportation and other expenses and

onboard and other expenses. A reconciliation of his-

torical Gross Yields to Net Yields is provided below

under Results of Operations. We have not provided a

quantitative reconciliation of projected Gross Yields

to projected Net Yields due to the significant uncer-

tainty in projecting the costs deducted to arrive at

this measure. Accordingly, we do not believe that rec-

onciling information for such projected figures would

be meaningful.

Occupancy, in accordance with cruise vacation indus-

try practice, is calculated by dividing Passenger

Cruise Days by APCD. A percentage in excess of 100%

indicates that three or more passengers occupied

some cabins.

Passenger Cruise Days represent the number of

passengers carried for the period multiplied by the

number of days of their respective cruises.

We believe Net Yields, Net Cruise Costs and Net Cruise

Costs Excluding Fuel are our most relevant non-GAAP

financial measures. However, a significant portion of

our revenue and expenses are denominated in curren-

cies other than the United States dollar. Because our

reporting currency is the United States dollar, the

value of these revenues and expenses can be affected

by changes in currency exchange rates. Although

such changes in local currency prices is just one of

many elements impacting our revenues and expenses,

it can be an important element. For this reason, we

also monitor Net Yields, Net Cruise Costs and Net

Cruise Costs Excluding Fuel as if the current periods’

currency exchange rates had remained constant with

the comparable prior periods’ rates, or on a “Constant

Currency” basis.

It should be emphasized that Constant Currency is

primarily used for comparing short-term changes

and/or projections. Over the longer term, changes in

guest sourcing and shifting the amount of purchases

between currencies can significantly change the

impact of the purely currency-based fluctuations.

The use of certain significant non-GAAP measures,

such as Net Yields, Net Cruise Costs and Net Cruise

Costs Excluding Fuel, allow us to perform capacity

and rate analysis to separate the impact of known

capacity changes from other less predictable changes

which affect our business. We believe these non-GAAP

measures provide expanded insight to measure reve-

nue and cost performance in addition to the standard

United States GAAP based financial measures. There

are no specific rules or regulations for determining

non-GAAP and Constant Currency measures, and as

such, there exists the possibility that they may not be

comparable to other companies within the industry.

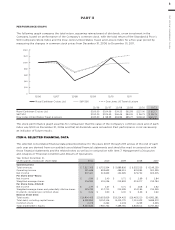

EXECUTIVE OVERVIEW

During 2011, our business demonstrated its fundamen-

tal strength and the efficacy of our business model.

Despite the impact of geopolitical events including

the political unrest in the Eastern Mediterranean and

Northern Africa and the earthquake and related events

in Japan as well as the uncertain global economic

environment, our net income for 2011 increased approx-

imately 18% to $607.4 million in 2011 from $515.7 million

in 2010 and our Net Yields increased 4.1%.

Prior to the recent tragedy in Italy involving the Costa

Concordia, booking patterns for 2012 were strong and

WAVE season (traditionally the first two months of

the year where cruise lines experience disproportion-

ately higher volume cruise sales) was off to an excel-

lent start. However, the Costa Concordia incident is

having a near-term effect on our bookings and the

impact on our earnings in 2012 and beyond remains

uncertain. Refer to our Outlook section for a further

discussion on our expected future results.

The globalization of our operations continues to be a

major initiative for 2012 and beyond, especially within

developmental markets. During 2012, we expect a sig-

nificant amount of our passenger ticket revenues from

outside of the United States. In 2012, Royal Caribbean

International will focus on the development of key

markets in Southern Europe and Asia, where we have

established a leading position in the Chinese market.

In furtherance of this, during 2012, Royal Caribbean

International will seasonally add a second ship in Asia

and a third ship in Australia, add new departure ports