Panera Bread 2014 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2014 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

PANERA BREAD COMPANY

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (continued)

51

and historical experience. Stock-based compensation expense is recognized only for those awards expected to vest, with forfeitures

estimated at the date of grant based on historical experience. The fair value of the awards expected to vest is amortized over the

vesting period. Options and restricted stock generally vest 25 percent after two years and thereafter 25 percent each year for the

next three years and options generally have a six-year term. Stock-based compensation expense is included in general and

administrative expenses in the Consolidated Statements of Comprehensive Income.

Asset Retirement Obligations

The Company recognizes the future cost to comply with lease obligations at the end of a lease as it relates to tangible long-lived

assets in accordance with the accounting standard for the asset retirement and environmental obligations ("ARO") in the Company’s

consolidated financial statements. Most lease agreements require the Company to restore the leased property to its original

condition, including removal of certain long-lived assets the Company has installed, at the end of the lease. A liability for the fair

value of an asset retirement obligation along with a corresponding increase to the carrying value of the related long-lived asset is

recorded at the time a lease agreement is executed. The Company amortizes the amount added to property and equipment, net

and recognizes accretion expense in connection with the discounted liability over the reasonably assured lease term. The estimated

liability is based on the Company’s historical experience in closing bakery-cafes, fresh dough facilities, and support centers and

the related external cost associated with these activities. Revisions to the liability could occur due to changes in estimated retirement

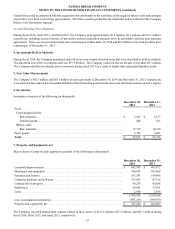

costs or changes in lease terms. As of December 30, 2014 and December 31, 2013, the Company's net ARO asset included in

property and equipment, net was $13.3 million and $4.6 million, respectively, and its net ARO liability included in other long-

term liabilities was $19.8 million and $10.2 million, respectively. ARO accretion expense was $0.6 million, $0.6 million, and

$0.4 million for fiscal 2014, fiscal 2013, and fiscal 2012, respectively.

Variable Interest Entities

The Company applies the guidance issued by the Financial Accounting Standards Board (the “FASB”) on accounting for variable

interest entities (“VIE”), which defines the process for how an enterprise determines which party consolidates a VIE as primarily

a qualitative analysis. The enterprise that consolidates the VIE (the primary beneficiary) is defined as the enterprise with (1) the

power to direct activities of the VIE that most significantly affect the VIE’s economic performance and (2) the obligation to absorb

losses of the VIE or the right to receive benefits from the VIE. The Company does not possess any ownership interests in franchise

entities or other affiliates. The franchise agreements are designed to provide the franchisee with key decision-making ability to

enable it to oversee its operations and to have a significant impact on the success of the franchise, while the Company’s decision-

making rights are related to protecting its brand. Based upon its analysis of all the relevant facts and considerations of the franchise

entities and other affiliates, the Company has concluded that these entities are not variable interest entities and they have not been

consolidated as of December 30, 2014.

Recent Accounting Pronouncements

In August 2014, the FASB issued Accounting Standards Update 2014-15, “Presentation of Financial Statements - Going Concern

(Subtopic 205-40); Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern”. This update requires

management of the Company to evaluate whether there is substantial doubt about the Company’s ability to continue as a going

concern. This update is effective for the annual period ending after December 15, 2016, and for annual and interim periods

thereafter. Early adoption is permitted. The Company is currently evaluating the effect of the standard but its adoption is not

expected to have an impact on the Company’s consolidated financial statements.

In May 2014, the FASB issued Accounting Standards Update 2014-09, “Revenue from Contracts with Customers (Topic 606)”.

This update provides a comprehensive new revenue recognition model that requires a company to recognize revenue to depict the

transfer of goods or services to a customer at an amount that reflects the consideration it expects to receive in exchange for those

goods or services. The guidance also requires additional disclosure about the nature, amount, timing and uncertainty of revenue

and cash flows arising from customer contracts. This update is effective for annual and interim periods beginning after December

15, 2016, which will require the Company to adopt these provisions in the first quarter of fiscal 2017. Early application is not

permitted. This update permits the use of either the retrospective or cumulative effect transition method. The Company is evaluating

the effect this guidance will have on the Company's consolidated financial statements and related disclosures. The Company has

not yet selected a transition method nor has it determined the effect of the standard on its ongoing financial reporting.

In July 2013, the FASB issued Accounting Standards Update No. 2013-11, “Income Taxes (Topic 740): Presentation of an

Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists”.

This guidance requires an unrecognized tax benefit related to a net operating loss carryforward, a similar tax loss or a tax credit

carryforward to be presented as a reduction to a deferred tax asset, unless the tax benefit is not available at the reporting date to

settle any additional income taxes under the tax law of the applicable tax jurisdiction. The guidance became effective at the