Panera Bread 2014 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2014 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

PANERA BREAD COMPANY

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (continued)

47

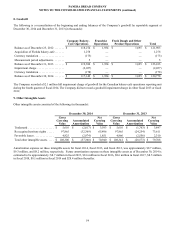

In considering the step one approach to testing goodwill for impairment, the Company utilized a quantitative assessment to test

goodwill for impairment for the Canadian reporting unit during the fourth quarter of fiscal 2014. The fair value of a reporting

unit is the price a willing buyer would pay for the reporting unit and is estimated using a discounted cash flow model. The

Company's discounted cash flow estimate was based upon, among other things, certain assumptions about expected future operating

performance, such as revenue growth rates, operating margins, risk-adjusted discount rates, and future economic and market

conditions. The Company determined the carrying value of the Canadian reporting unit exceeded its fair value and thus step two

of the goodwill impairment test was completed. The step two analysis indicated the entire balance of goodwill for the Canadian

reporting unit was impaired and the Company recorded a full goodwill impairment charge of $2.1 million. This charge was

recorded in other (income) expense, net in the Consolidated Statements of Comprehensive Income.

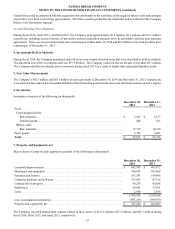

Other Intangible Assets, net

Other intangible assets, net consist primarily of favorable lease agreements, re-acquired territory rights, and trademarks. The

Company amortizes the fair value of favorable lease agreements over the remaining related lease terms at the time of the acquisition,

which ranged from approximately one year to 17 years as of December 30, 2014. The fair value of re-acquired territory rights

was based on the present value of the acquired bakery-cafe cash flows. The Company amortizes the fair value of re-acquired

territory rights over the remaining contractual terms of the re-acquired territory rights at the time of the acquisition, which ranged

from approximately five years to 20 years as of December 30, 2014. The fair value of trademarks is amortized over their estimated

useful life of 22 years.

The Company reviews intangible assets with finite lives for impairment when events or circumstances indicate these assets might

be impaired. When warranted, the Company tests intangible assets with finite lives for impairment using historical cash flows

and other relevant facts and circumstances as the primary basis for an estimate of future cash flows. There were no other intangible

asset impairment charges recorded during fiscal 2014, fiscal 2013, and fiscal 2012. There can be no assurance that future intangible

asset impairment tests will not result in a charge to earnings.

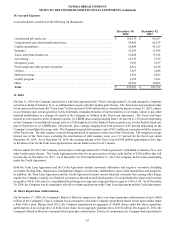

Impairment of Long-Lived Assets

The Company evaluates whether events and circumstances have occurred that indicate the remaining estimated useful life of long-

lived assets may warrant revision or that the remaining balance of an asset may not be recoverable. The Company compares

anticipated undiscounted cash flows from the related long-lived assets of a bakery-cafe or fresh dough facility with their respective

carrying values to determine if the long-lived assets are recoverable. If the sum of the anticipated undiscounted cash flows for

the long-lived assets is less than their carrying value, an impairment loss is recognized for the difference between the anticipated

discounted cash flows, which approximates fair value, and the carrying value of the long-lived assets. In performing this analysis,

management estimates cash flows based upon, among other things, certain assumptions about expected future operating

performance, such as revenue growth rates, operating margins, risk-adjusted discount rates, and future economic and market

conditions. Estimates of cash flow may differ from actual cash flow due to, among other things, economic conditions, changes

to the Company's business model or changes in operating performance. The long-term financial forecasts that management utilizes

represent the best estimate that management has at this time and management believes that the underlying assumptions are

reasonable.

The Company recognized impairment losses of $0.9 million, $0.8 million, and $0.3 million during fiscal 2014, fiscal 2013, and

fiscal 2012, respectively, related to distinct, underperforming Company-owned bakery-cafes. These losses were recorded in other

operating expenses in the Consolidated Statements of Comprehensive Income.

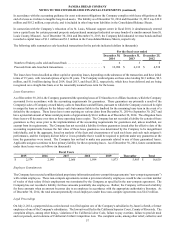

Self-Insurance Reserves

The Company is self-insured for a significant portion of its workers’ compensation, group health, and general, auto, and property

liability insurance with varying deductibles of as much as $0.8 million for individual claims, depending on the type of claim. The

Company also purchases aggregate stop-loss and/or layers of loss insurance in many categories of loss. The Company utilizes

third party actuarial experts’ estimates of expected losses based on statistical analyses of historical industry data, as well as its

own estimates based on the Company’s actual historical data to determine required self-insurance reserves. The assumptions are

closely reviewed, monitored, and adjusted when warranted by changing circumstances. The estimated accruals for these liabilities

could be affected if actual experience related to the number of claims and cost per claim differs from these assumptions and

historical trends. Based on information known at December 30, 2014, the Company believes it has provided adequate reserves

for its self-insurance exposure. As of December 30, 2014 and December 31, 2013, self-insurance reserves were $32.6 million and

$31.5 million, respectively, and were included in accrued expenses in the Consolidated Balance Sheets. The total amounts expensed

for self-insurance were $50.7 million, $46.9 million, and $41.8 million for fiscal 2014, fiscal 2013, and fiscal 2012, respectively.