NetFlix 2005 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2005 NetFlix annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

Indemnifications

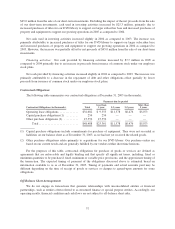

In the ordinary course of business, we enter into contractual arrangements under which we agree to provide

indemnification of varying scope and terms to business partners and other parties with respect to certain matters,

including, but not limited to, losses arising out of our breach of such agreements and out of intellectual property

infringement claims made by third parties. In addition, we have entered into indemnification agreements with our

directors and certain of our officers that will require us, among other things, to indemnify them against certain

liabilities that may arise by reason of their status or service as directors or officers.

The terms of such obligations vary. Generally, a maximum obligation is not explicitly stated, so the overall

maximum amount of the obligations cannot be reasonably estimated. To date, we have not incurred material

costs as a result of such obligations and have not accrued any liabilities related to such indemnification

obligations in our financial statements.

Recent Accounting Pronouncements

In December 2004, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial

Accounting Standards (“SFAS”) No. 123(R), Share-Based Payment, which establishes standards for transactions

in which an entity exchanges its equity instruments for goods or services. This standard replaces SFAS No. 123,

Accounting for Stock-Based Compensation and supersedes APB Opinion No. 25, Accounting for Stock issued to

Employees. This Standard requires a public entity to measure the cost of employee services received in exchange

for an award of equity instruments based on the grant-date fair value of the award. This eliminates the exception

to account for such awards using the intrinsic method previously allowable under APB Opinion No. 25. In March

2005, the Securities and Exchange Commission (“SEC”) issued Staff Accounting Bulletin 107 (SAB 107) which

summarizes the views of the SEC staff regarding the interaction between SFAS 123(R) and certain SEC rules and

regulations and provides the staff’s views regarding the valuation of share-based payment arrangements for

public companies. In April 2005, the SEC issued Release 33-8568 delaying the effective date of SFAS 123(R),

and as such we will be required to implement the provisions of SFAS No. 123(R) beginning January 1, 2006. We

previously adopted the fair value recognition provisions of SFAS No. 123 in the second quarter of 2003, and

restated prior periods at that time. Accordingly, we believe SFAS No. 123(R) will not have a material impact on

our financial position or results of operations.

In accordance with SAB 107, effective January 1, 2006 we will no longer present stock-based compensation

separately on our statements of income. Instead, we will present stock-based compensation in the same lines as

cash compensation paid to the same individuals.

Additionally, SFAS 123(R) requires that cash inflows from financing activities on our statement of cash

flows include the cash retained as a result of the tax deductibility of increases in the value of equity instruments

issued under share-based payment arrangements in excess of any related stock-based compensation recognizable

for financial reporting purposes. These tax benefits shall be determined based on the individual award method.

This cash benefit has been included in the determination of cash provided by operating activities on our

statement of cash flows in 2004. The change in methods will not likely have a significant negative effect on our

cash provided by operating activities in periods after adoption of SFAS 123(R).

In March 2005, the FASB issued FIN 47, Accounting for Conditional Asset Retirement Obligations. FIN 47

clarifies that an entity must record a liability for a “conditional” asset retirement obligation if the fair value of the

obligation can be reasonably estimated. The provision is effective for no later than the end of fiscal years ending

after December 15, 2005. We do not expect the adoption of this standard to have a material effect on our

financial position or results of operations.

In June 2005, the FASB issued SFAS No. 154, Accounting Changes and Error Corrections. SFAS 154

replaces APB Opinion No. 20, Accounting Changes and SFAS No. 3, Reporting Accounting Changes in Interim

Financial Statements. SFAS 154 requires that a voluntary change in accounting principle be applied

38