National Grid 2015 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2015 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

|

|

Additional Information

Shareholder information continued

This discussion is not a comprehensive description of all the US

federal income tax and UK tax considerations that may be relevant

to any particular investor (including consequences under the US

alternative minimum tax or net investment income tax) and does

not address state, local, or other tax laws. National Grid has

assumed that shareholders, including US Holders, are familiar

withthe tax rules applicable to investments in securities generally

and with any special rules to which they may be subject. This

discussion deals only with US Holders who hold ADSs or ordinary

shares as capital assets. It does not address the tax treatment of

investors who are subject to special rules, such as:

• financial institutions;

• insurance companies;

• dealers in securities or currencies;

• investors who elect mark-to-market treatment;

• partnerships or other pass-through entities and their partners;

• individual retirement accounts and other tax-deferred accounts;

• tax-exempt organisations;

• investors who own (directly or indirectly) 10% or more of our

voting stock;

• investors who hold ADSs or ordinary shares as a position in a

straddle, hedging transaction or conversion transaction; and

• investors whose functional currency is not the US dollar.

The statements regarding US and UK tax laws and administrative

practices set forth below are based on laws, treaties, judicial

decisions and regulatory interpretations in effect on the date of this

document. These laws and practices are subject to change without

notice, potentially with retroactive effect. In addition, the statements

set forth below are based on the representations of the Depositary

and assume that each party to the Deposit Agreement will perform

its obligations thereunder in accordance with its terms.

US Holders of ADSs will be treated as the owners of the ordinary

shares represented by those ADSs for US federal income tax

purposes. For the purposes of the Tax Convention, the Estate Tax

Convention and UK tax considerations, this discussion assumes

that a US Holder of ADSs will be treated as the owner of the

ordinary shares represented by those ADSs. HMRC has stated

thatit will continue to apply its long-standing practice of treating

aholder of ADSs as holding the beneficial interest in the ordinary

shares represented by the ADSs; however, we note that this is an

area of some uncertainty and may be subject to change.

US Holders should consult their own advisors regarding the tax

consequences of buying, owning and disposing of ADSs or

ordinary shares in light of their particular circumstances, including

the effect of any state, local, or other tax laws.

Taxation of dividends

The UK does not currently impose a withholding tax on dividends

paid to US Holders.

Cash distributions paid out of our current or accumulated earnings

and profits (as determined for US federal income tax purposes)

generally will be taxable to a US Holder as dividend income.

Distributions in excess of current and accumulated earnings and

profits will be treated as a non-taxable return of capital to the extent

of a US Holder’s basis in its ADSs or ordinary shares, as applicable,

and thereafter as a capital gain. However, we do not maintain

calculations of our earnings and profits in accordance with US

federal income tax principles. US Holders should therefore assume

that any distribution by us with respect to ADSs or ordinary shares

will be reported as dividend income.

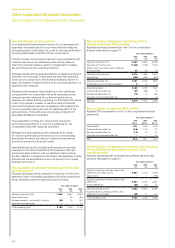

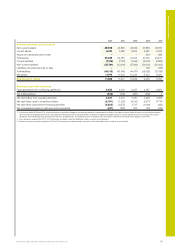

Price history

The following table shows the highest and lowest intraday market

prices for our ordinary shares and ADSs for the periods indicated:

Ordinary share (pence) ADS ($)

High Low High Low

2014/15 965.00 806.22 77. 21 62.25

2013/14 849.50 711.0 0 70.07 55.16

2012/13 770.00 6 27. 0 0 58.33 49.55

2011/12 660.50 545.50 52.18 45.80

2010/111666.00 474.80 51.00 36.72

2014/15 Q4 954.00 842.60 72.41 62.25

Q3 965.00 853.78 75.08 6 7.01

Q2 916.00 835.76 7 7.21 70.37

Q1 8 9 7.9 2 806.22 75.09 67.6 2

2013/14 Q4 842.50 769.00 70.07 63.19

Q3 797. 5 0 725.16 65.39 58.85

Q2 817.75 727.4 5 61.59 55.30

Q1 849.50 711.0 0 64.56 5 5.16

April 2015 910.90 863.60 68.88 64.65

March 2015 8 97. 8 0 842.60 68.22 62.25

February 2015 942.10 868.20 71.13 67.12

January 2015 954.00 890.89 72.41 67.8 7

December 2014 936.90 860.03 73.54 67.01

1. On 20 May 2010, we announced a 2 for 5 rights issue of 990,439,017 ordinary shares at

355 pence per share.

Shareholder analysis

The following table includes a brief analysis of shareholder numbers

and shareholdings as at 31 March 2015.

Size of shareholding

Number of

shareholders

% of

shareholders

Number

of shares

% of

shares

1–50 170,30 0 17.7275 4,916,530 0.1263

51–100 259,888 27. 0 5 3 2 18,391,904 0.4726

101–500 415,128 43.2131 87,234,245 2.2416

501–1,000 57, 9 3 0 6.0303 4 0,551,74 5 1.0420

1,001–10,000 54,252 5.6474 133,804,248 3.4382

10,001–50,000 2,074 0.2159 37,223,848 0.9565

50,001–100,000 196 0.0204 14,049,218 0.3610

100,001–500,000 444 0.0462 107,102,598 2.7521

500,001–1,000,000 133 0.0138 94,059,625 2.4169

1,000,001+ 309 0.0322 3,354,357,939 86.1928

Tot al 960,654 100 3,891,691,900 100

Taxation

The discussion in this section provides information about certain

US federal income tax and UK tax consequences for US Holders

(defined below) of owning ADSs and ordinary shares. A US Holder

is beneficial owner of ADSs or ordinary shares that:

• is (i) an individual citizen or resident of the United States, (ii) a

corporation created or organised under the laws of the United

States, any State thereof or the District of Columbia, (iii) an estate

the income of which is subject to US federal income tax without

regard to its source or (iv) a trust if a court within the United

States is able to exercise primary supervision over the

administration of the trust and one or more US persons have the

authority to control all substantial decisions of the trust, or the

trust has elected to be treated as a domestic trust for US federal

income tax purposes;

• is not resident or ordinarily resident in the UK for UK tax

purposes; and

• does not hold ADSs or ordinary shares in connection with the

conduct of a business or the performance of services in the UK

or otherwise in connection with a branch, agency or permanent

establishment in the UK.

182