National Grid 2015 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2015 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

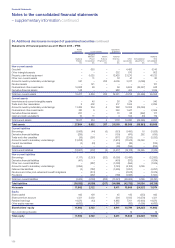

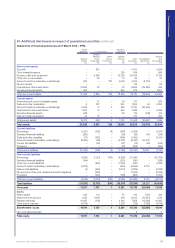

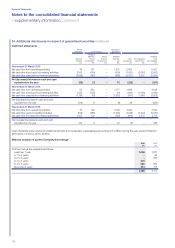

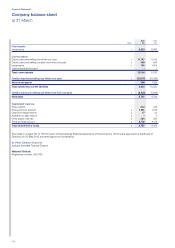

Additional Information

The business in detail continued

UK regulation

Our licences are established under the Gas Act 1986 and

Electricity Act 1989, as amended (the Acts). They require us to

develop, maintain and operate economic and efficient networks

and to facilitate competition in the supply of gas and electricity in

Great Britain. They also give us statutory powers. These include

theright to bury our pipes or cables under public highways and

theability to use compulsory powers to purchase land so we can

conduct our business.

Our networks are regulated by Ofgem, which has established

pricecontrol mechanisms that set the amount of revenue that our

regulated businesses can earn. Price control regulation is designed

to make sure our interests, as a monopoly, are balanced with those

of our customers. Ofgem allows us to charge reasonable, but not

excessive, prices. This gives us a future level of revenue that is

sufficient to meet our statutory duties and licence obligations,

andmakes a reasonable return on our investment.

The price control includes a number of mechanisms designed to

help achieve its objectives. These include financial incentives that

encourage us to:

• continuously improve the cost and effectiveness of our services;

• manage and operate our networks efficiently;

• deliver high-quality services to our customers and wider

stakeholder community; and

• invest in developing the network in a way that ensures long-term

security of supply.

Our UK Electricity Transmission (UK ET), UK Gas Transmission

(UKGT) and UK Gas Distribution (UK GD) businesses operate

under eight separate price controls in the UK. These comprise two

for our UK ET operations, one covering our role as transmission

owner (TO) and the other for our role as system operator (SO);

twofor our UK GT operations, again one as TO and one as SO;

andone for each of our four regional gas distribution networks.

While each of the eight price controls may have differing terms,

they are based on a consistent regulatory framework.

In addition to the eight price controls, our LNG storage business

has a price control covering some aspects of its operations.

Thereis also a tariff cap price control applied to certain elements

ofdomestic metering and daily meter reading activities carried out

by National Grid Metering.

Interconnectors derive their revenues from congestion revenues.

Congestion revenues depend on the existence of price

differentialsbetween markets at either end of the interconnector.

European legislation governs how capacity is allocated. It requires

all interconnection capacity to be allocated to the market

throughauctions.

There are a range of different regulatory models available for

interconnector projects. These involve various levels of regulatory

insight ranging from fully merchant (the project is reliant on

revenues selling interconnector capacity) to ‘cap and floor’

(whererevenues above the cap are returned to system users

andrevenues below the floor are topped by system users thus

reducing the overall project risk).

RIIO price controls

On 1 April 2013, our UK regulator introduced a new regulatory

framework called RIIO (revenue = incentives + innovation +

outputs), which lasts for eight years. The building blocks of the

RIIOprice control are broadly similar to the historical price controls

used in the UK. However, there are some significant differences

inthe mechanics of the calculations.

How is revenue calculated?

Under RIIO the outputs we deliver are clearly articulated and are

integrally linked to the calculation of our allowed revenue. These

outputs have been determined through an extensive consultation

process, which has given stakeholders a greater opportunity to

influence the decisions. The clarity around outputs should lead

togreater transparency in how we deliver them.

The six output categories are:

Safety: ensuring the provision of a safe energy network.

Reliability (and availability): promoting networks capable of

delivering long-term reliability, as well as minimising the number

and duration of interruptions experienced over the price control

period, and ensuring adaptation to climate change.

Environmental impact: encouraging companies to play their role

inachieving broader environmental objectives – specifically,

facilitating the reduction of carbon emissions – as well as

minimising their own carbon footprint.

Customer and stakeholder satisfaction: maintaining high levels of

customer satisfaction and stakeholder engagement, and improving

service levels.

Customer connections: encouraging networks to connect

customers quickly and efficiently.

Social obligations (UK Gas Distribution only): extending the gas

network to communities that are fuel poor where it is efficient to

doso, and introducing measures to address carbon monoxide

poisoning incidents.

Within each of these output categories are a number of primary

and secondary deliverables, reflecting what our stakeholders

wantus to deliver over the coming price control period. The nature

and number of these deliverables varies according to the output

category, with some being linked directly to our allowed revenue,

some linked to legislation, and others having only a reputational

impact. Ofgem, using information we have submitted, along

withindependent assessments, determines the efficient level

ofexpected costs necessary to deliver them. Under RIIO this is

known as totex, which is total allowable expenditure, and is similar

to the sum of what was controllable opex, capex (and repex

forUKGas Distribution) under the previous price control periods.

A number of assumptions are necessary in setting these outputs,

such as certain prices or the volumes of work that will be needed.

Consequently, there are a number of uncertainty mechanisms

within the RIIO framework that can result in adjustments to totex

ifactual prices or volumes differ from the assumptions. These

mechanisms protect us and our customers from windfall gains

andlosses.

166