Kodak 2015 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2015 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

|

|

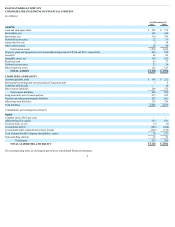

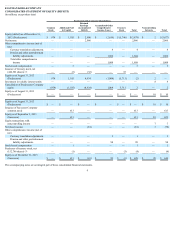

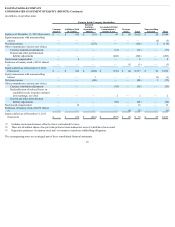

EASTMAN KODAK COMPANY

NOTES TO FINANCIAL STATEMENTS

NOTE 1: BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

BASIS OF PRESENTATION

On January 19, 2012 (the “Petition Date”), Eastman Kodak Company (“EKC” or the “Company”) and its U.S. subsidiaries (collectively, the “Debtors”) filed

voluntary petitions for relief under chapter 11 of the United States Bankruptcy Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the

Southern District of New York (the “Bankruptcy Court”). The cases (the “Chapter 11 Cases”) were jointly administered as Case No. 12-10202 (ALG) under the

caption “In re Eastman Kodak Company.” The Debtors operated their businesses as “debtors-in-possession” under the jurisdiction of the Bankruptcy Court and in

accordance with the applicable provisions of chapter 11 of the Bankruptcy Code and the orders of the Bankruptcy Court until their emergence from

bankruptcy. The Company’s foreign subsidiaries were not part of the Chapter 11 Cases, and continued to operate in the ordinary course of business.

Upon emergence from bankruptcy on September 3, 2013, Kodak adopted fresh-start accounting which resulted in Kodak becoming a new entity for financial

reporting purposes. Kodak applied fresh start accounting as of September 1, 2013. Accordingly, the consolidated financial statements on or after September 1, 2013

are not comparable to the consolidated financial statements prior to that date. Refer to Note 25, “Fresh Start Accounting” for additional information.

Subsequent to the Petition Date, all expenses, gains and losses directly associated with the reorganization proceedings are reported as Reorganization items, net in

the accompanying Consolidated Statement of Operations. In addition, Liabilities subject to compromise during the chapter 11 proceedings were distinguished from

liabilities of the Company’s foreign subsidiaries that were not part of the Chapter 11 Cases, fully-secured liabilities that were not expected to be compromised and

from post-petition liabilities in the accompanying Consolidated Statement of Financial Position.

References to “Successor” or “Successor Company” relate to the reorganized Kodak subsequent to September 3, 2013. References to “Predecessor” or

“Predecessor Company” relate to Kodak prior to September 3, 2013.

Reclassifications

Certain amounts for prior periods have been reclassified to conform to the current period classification due to Kodak’s new organization structure as of January 1,

2015 and for a change in the segment measure of profitability. In addition to the changes in segment reporting under the new organization structure, tenant rental

income for Eastman Business Park previously reported in Cost of Revenues is reported in Revenues. Refer to Note 23, “Segment Information” for more

information about these changes.

ACCOUNTING PRINCIPLES

The consolidated financial statements and accompanying notes are prepared in accordance with accounting principles generally accepted in the United States of

America (“U.S. GAAP”). The following is a description of the significant accounting policies of Kodak.

BASIS OF CONSOLIDATION

The consolidated financial statements include the accounts of EKC and all companies directly or indirectly controlled by EKC, either through majority ownership

or otherwise (collectively “Kodak”). Kodak consolidates variable interest entities if Kodak has a controlling financial interest and is determined to be the primary

beneficiary of the entity.

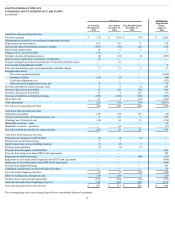

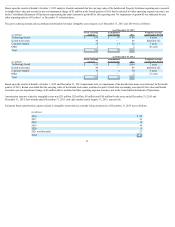

Kodak is the primary beneficiary of a utilities variable interest entity, RED-Rochester, LLC (“RED”). Therefore, Kodak consolidates RED’s assets, liabilities and

results of operations. Consolidated assets and liabilities of RED are $69 million and $13 million, respectively, as of December 31, 2015 and $77 million and $11

million, respectively, as of December 31, 2014. RED’s equity in those net assets as of December 31, 2015 and 2014 is $25 million and $21 million, respectively.

RED’s results of operations are reflected in net income attributable to noncontrolling interest in the accompanying Consolidated Statement of Operations.

USE OF ESTIMATES

The preparation of financial statements in conformity with U.S. GAAP accounting requires management to make estimates and assumptions that affect the reported

amounts of assets and liabilities and disclosure of commitments and contingencies at year end, and the reported amounts of revenues and expenses during the

reporting periods presented. Actual results could differ from these estimates.

13