JetBlue Airlines 2004 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2004 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

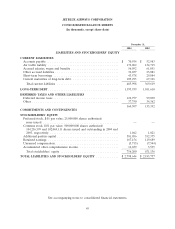

|

|

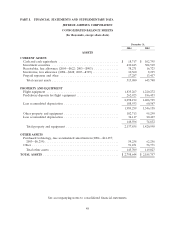

escrow with a depositary. As aircraft are delivered, the cash proceeds are utilized to purchase our

secured equipment notes issued to finance these aircraft.

We currently have shelf registration statements on file with the Securities and Exchange

Commission related to the issuance of $1 billion aggregate amount of common stock, preferred stock,

debt securities and/or pass-through certificates. The net proceeds of any securities we sell under these

registration statements may be used to fund working capital and capital expenditures, including the

purchase of aircraft and construction of facilities on or near airports. Through December 31, 2004, we

had issued $498.2 million in pass-through certificates under these registration statements.

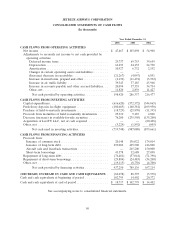

Financing activities during 2003 consisted primarily of (1) the public offering of 4,485,000 shares of

our common stock at $28.33 per share, as adjusted for our November 2003 stock split, raising net

proceeds of $122.5 million, (2) our issuance of $175 million of 31⁄2% convertible notes due 2033, raising

net proceeds of $170.4 million, (3) the sale and leaseback over 20 years of seven aircraft for

$265.2 million with a U.S. leasing institution, (4) the incurrence of $270.5 million of 10- to 12- year

floating rate equipment notes issued to various European banks secured by eight aircraft, (5) net

short-term borrowings of $8.2 million, and (6) the repayment of $57.0 million of debt. Net proceeds

from our equity and notes offerings are being used to fund working capital and capital expenditures,

including capital expenditures related to the purchase of aircraft and construction of facilities on or

near airports.

None of our lenders or lessors are affiliated with us. Our short-term borrowings are part of a

floating rate facility with a group of commercial banks to finance aircraft predelivery deposits.

Capital Resources. We have been able to generate sufficient funds from operations to meet our

working capital requirements. We do not currently have any lines of credit and almost all of our

property and equipment is encumbered. We typically finance our aircraft through either secured debt

or lease financing. At December 31, 2004, we operated a fleet of 69 Airbus A320 aircraft, of which 25

are financed under operating leases with the remaining 44 financed by secured debt. At December 31,

2004, secured debt financing has been arranged for all of our Airbus A320 aircraft deliveries scheduled

for 2005. Lease financing has been arranged for the first 30 of our Embraer E190 aircraft deliveries.

Although we believe that debt and/or lease financing should be available for our remaining aircraft

deliveries, we cannot assure you that we will be able to secure financing on terms attractive to us, if at

all. While these financings may or may not result in an increase in liabilities on our balance sheet, our

fixed costs will increase significantly regardless of the financing method ultimately chosen. To the extent

we cannot secure financing, we may be required to modify our aircraft acquisition plans or incur higher

than anticipated financing costs.

Working Capital. Our working capital was $29.1 million and $276.1 million at December 31, 2004

and December 31, 2003, respectively. We expect to meet our obligations as they become due through

available cash and internally generated funds, supplemented as necessary by debt and/or equity

financings and proceeds from aircraft sale and leaseback transactions. We expect to continue generating

positive working capital through our operations. However, we cannot predict whether current trends

and conditions will continue or what the effect on our business might be from the extremely

competitive environment we are operating in or from events that are beyond our control, such as

increased fuel prices, the impact of airline bankruptcies or consolidations, U.S. military actions, or acts

of terrorism. We have obtained financing for all of our aircraft deliveries scheduled for 2005. Assuming

that we utilize the predelivery short-term borrowing facility available to us, we believe the working

capital available to us will be sufficient to meet our cash requirements for at least the next 12 months.

42