Hyundai 2005 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2005 Hyundai annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

|

|

78

HYUNDAI MOTOR COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2005 AND 2004

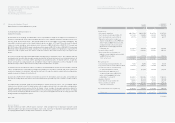

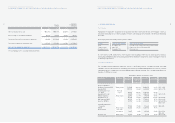

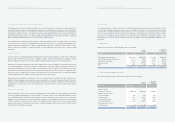

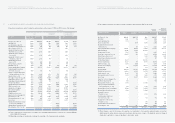

Contract parties Derivatives Period Number of Initial price

KIA shares

Credit Suisse First Boston International Equity swap September 17, 2003 ~

September 8, 2008 12,145,598 US$ 8.2611

Credit Suisse First Boston International Call option (*) " 12,145,598 US$ 11.5300

Credit Suisse First Boston International Equity swap " 21,862,076 US$ 8.2611

JP Morgan Chase Bank, London Branch Equity swap " 1,839,367 US$ 7.8811

Derivative Instruments

All derivative instruments are accounted for at fair value with the valuation gain or loss recorded as an asset or liability. If the

derivative instrument is not part of a transaction qualifying as a hedge, the adjustment to fair value is reflected in current

operations. The accounting for derivative transactions that are part of a qualified hedge based both on the purpose of the

transaction and on meeting the specified criteria for hedge accounting differs depending on whether the transaction is a fair

value hedge or a cash flow hedge. Fair value hedge accounting is applied to a derivative instrument designated as hedging the

exposure to changes in the fair value of an asset or a liability or a firm commitment (hedged item) that is attributable to a

particular risk. The gain or loss both on the hedging derivative instruments and on the hedged item attributable to the hedged

risk is reflected in current operations. Cash flow hedge accounting is applied to a derivative instrument designated as hedging

the exposure to variability in expected future cash flows of an asset or a liability or a forecast transaction that is attributable to a

particular risk. The effective portion of gain or loss on a derivative instrument designated as a cash flow hedge is recorded as a

capital adjustment and the ineffective portion is recorded in current operations. The effective portion of gain or loss recorded

as a capital adjustment is reclassified to current earnings in the same period during which the hedged forecasted transaction

affects earnings. If the hedged transaction results in the acquisition of an asset or the incurrence of a liability, the gain or loss in

capital adjustment is added to or deducted from the asset or the liability.

The Company entered into derivative instrument contracts with the settlement for the difference between the fair value and the

contracted initial price of Kia Motors Corporation shares as follows:

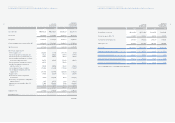

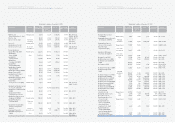

The gain or loss on valuation of these derivatives related to the fair value of KIA shares is recognized in current operations. As

of December 31, 2005, all premiums to be paid by the Company are recorded as accounts payable - other in current liabilities

of ₩23,455 million (US$23,154 thousand) and long-term other accounts payable in long-term liabilities of ₩40,209 million

(US$39,693 thousand), after deducting the present value discount of ₩6,584 million (US$6,500 thousand) and the present

value of all premiums on the effective date of contracts is recorded as deferred derivative assets in other assets. Also, as of

December 31, 2005, all premiums to be received by the Company are recorded as accounts receivable-other in current assets

of ₩3,845 million (US$3,796 thousand) and long-term other accounts receivable in non-current assets of ₩6,536 million

(US$6,452 thousand), after deducting the present value discount of ₩1,154 million (US$1,139 thousand) and the present

value of such premiums on the effective date of contract is recorded as deferred derivatives liabilities in other long-term

liabilities. As of December 31, 2004, all premiums to be paid by the Company are recorded as accounts payable - other in

current liabilities of ₩24,168 million (US$23,858 thousand) and long-term other accounts payable in long-term liabilities of

₩60,492 million (US$ 59,716 thousand), after deducting the present value discount of ₩11,891 million (US$11,738 thousand).

Also, as of December 31, 2004, all premiums to be received by the Company are recorded as accounts receivable-other in

current assets of ₩3,962 million (US$3,911 thousand) and long-term other accounts receivable in non-current assets of

₩9,771 million (US$9,646 thousand), after deducting the present value discount of ₩2,115 million (US$2,088 thousand). The

present value discount is amortized using the effective interest method.

(*) The Company has the position of seller.

77

HYUNDAI MOTOR COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2005 AND 2004

Accounting for Lease Contracts

In case the risk and benefit from the ownership of the leased property is de facto transferred to the lessee, such lease is

classified as a financial lease; otherwise, it is classified as an operating lease.

The lease that is non-cancelable in substance for the entire lease term is classified as a financial lease if at least one of the

following conditions are met: (1) The ownership of the leased property is to be transferred to the lessee at the end or before of

the lease term for free or some agreed price; (2) The lessee has a bargain purchase option; (3) The lease term is not less than

75/100 of the estimated economic life of the leased property; and (4) The present value of the basic lease rentals as of the

inception of the lease using the implicit interest rate is not less than 90/100 of the fair value of the leased property.

The lower of the present value after discounting basic lease rentals by the implicit interest rate and the fair value of leased

property are respectively recorded as assets and liabilities on financial lease. Leased assets are depreciated consistently with

the depreciation of the same or similar tangible assets, which the lessee owns.

In the case of an operating lease, basic lease rentals, in principle, are charged to expenses on a straight-line basis over the

lease term. However, when there is any method that better represents the procedure of allocation of expenses related to

lease, this method may be applied. Contingent rentals are charged to expenses when they are incurred. However, if payment

of contingent rental is uncertain, contingent rental may be charged as expense when it becomes due for payment.

Accrued Severance Benefits

Employees and directors of the Company and its subsidiaries are entitled to receive a lump-sum payment upon termination of

their service based on the applicable severance plan of each company. The accrued severance benefits that would be

payable assuming all eligible employees of the Company and its domestic subsidiaries terminated their employment amount to

₩3,015,591 million (US$2,998,481 thousand) and ₩2,797,232 million (US$2,761,335 thousand) as of December 31, 2005

and 2004, respectively.

Accrued severance benefits are funded through an individual severance insurance plan. Individual severance insurance

deposits, of which a beneficiary is a respective employee, are presented as deduction from accrued severance benefits.

Actual payments of severance benefits amounted to ₩423,551 million (US$418,115 thousand) and ₩538,361 million

(US$531,452 thousand) in 2005 and 2004, respectively.

Accrued Warranties and Product Liabilities

The Company and its subsidiaries generally provide a warranty to the ultimate consumer with each product and accrue

warranty expense at the time of sale based on actual claims history. Also, the Company accrues potential expenses, which

may occur due to product liability suits, pending voluntary recall campaign and other obligation as of the balance sheet date.

Actual costs incurred are charged against the accrual when paid.

Stock Options

The Company and its subsidiaries compute total compensation expense to stock options, which are granted to employees

and directors, by the fair value method using the option-pricing model. The compensation expense has been accounted for as

a charge to current operations and a credit to capital adjustments from the grant date using the straight-line method.