Hyundai 2005 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2005 Hyundai annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

|

|

74

HYUNDAI MOTOR COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2005 AND 2004

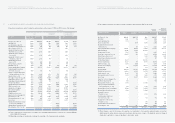

Valuation of Securities

Securities are recognized initially at cost, which includes the market price of the consideration given to acquire them and

incidental expenses. If the market price of the consideration is not reliably determinable, the market prices of the securities

purchased are used as the basis for measurement. If neither the market prices of the consideration given nor those of the

acquired securities are available, the acquisition cost is measured at the best estimates of its fair value.

After initial recognition, held-to-maturity securities are stated at amortized cost. The difference between their acquisition costs

and face values of held-to-maturity securities is amortized over the remaining term of the securities by applying the effective

interest method and added to or subtracted from the acquisition costs and interest income of the remaining period. Trading

securities are valued at fair value, with unrealized gains or losses included in current operations. Available-for-sales securities

are also valued at fair value, with unrealized gains or losses included in capital adjustments, until the securities are sold and if

the securities are determined to be impaired, the lump-sum cumulative amount of capital adjustments are included in current

operations. However, available-for-sales securities that are not traded in an active market and whose fair values cannot be

reliably estimated are accounted for at their acquisition costs. For those securities that are traded in an active market, fair

values refer to those quoted market prices, which are measured as the closing price at the balance sheet date. The fair value

of non-marketable debt securities are measured at the discounted future cash flows by using the discount rate that

appropriately reflects the credit rating of issuing entity assessed by a publicly reliable independent credit rating agency. If

application of such measurement method is not feasible, estimates of the fair values may be made using a reasonable

valuation model or quoted market prices of similar debt securities issued by entities conducting similar business in similar

industries.

Securities are evaluated at each balance sheet date to determine whether there is any objective evidence of impairment loss.

When any such evidence exists, unless there is a clear counter-evidence that recognition of impairment is unnecessary, the

Company estimates the recoverable amount of the impaired security and recognizes any impairment loss in current operations.

The amount of impairment loss of the held-to-maturity security or non-marketable equity security is measured as the difference

between the recoverable amount and the carrying amount. The recoverable amount of held-to maturity security is the present

value of expected future cash flows discounted at the securities’ original effective interest rate. For available-for-sale debt or

equity security stated at fair value, the amount of impairment loss to be recognized in the current period is determined by

subtracting the amount of impairment loss of debt or equity security already recognized in prior period from the amount of

amortized cost in excess of the recoverable amount for debt security or the amount of the acquisition cost in excess of the fair

value for equity security. For non-marketable equity securities accounted for at acquisition costs, the impairment loss is equal

to the difference between the recoverable amount and the carrying amount.

If the realizable value subsequently recovers, in case of a security stated at fair value, the increase in value is recorded in

current operations, up to the amount of the previously recognized impairment loss, while for the security stated at amortized

cost or acquisition cost, the increase in value is recorded in current operation, so that its recovered value does not exceed

what its amortized cost would be as of the recovery date if there had been no impairment loss.

When transfers of securities between categories are needed because of changes in an entity’s intention and ability to hold

those securities, such transfer is accounted for as follows: trading securities cannot be reclassified into available-for-sale and

held-to-maturity securities, and vice versa, except when certain trading securities lose their marketability. Available-for-sale

securities and held-to-maturity securities can be reclassified into each other after fair value recognition. When held-to-maturity

security is reclassified into available-for-sale security, the difference between the book value and fair value is reported in capital

adjustments. Whereas, in case available-for-sale security is reclassified into held-to-maturity securities, the difference is

reported in capital adjustments and amortized over the remaining term of the securities using the effective interest method.

The lower of the fair value of treasury stock included in treasury stock fund and the fair value of investments in treasury stock

funds is accounted for as treasury stock in capital adjustment.

73

HYUNDAI MOTOR COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2005 AND 2004

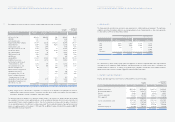

When consolidated companies are merged together during a fiscal year, for purposes of consolidation, the merger is regarded

as additional acquisition of ownership. The net income for the acquiree as of the merger date is reflected in the consolidated

statement of income.

Inter-company receivables, payables, revenues and expenses arising from transactions between the Company and its

subsidiaries or among subsidiaries are eliminated against each other in the consolidated financial statements. On sales from

the Company to its subsidiaries (downstream sales), the full amounts of unrealized gains or loss are eliminated in the

consolidated income and charged (credited) to the majority interests. On sales from a subsidiary to the Company (upstream

sales), unrealized gains and losses are eliminated and allocated proportionately between majority and minority interests.

The accounting methods adopted by the Company and its subsidiaries for similar transactions and circumstances are

generally the same. However, if the differences resulting from applying different accounting methods are not material, such

different methods are applied. Financial statements of a subsidiary as of the same closing date of the Company are used in

preparing the consolidation.

Revenue Recognition

Sales of goods is recognized at the time of shipment only if it meet the conditions that significant risks and rewards of

ownership of the goods have been transferred to the customer, and neither continuing managerial involvement nor effective

control over the goods sold is retained. Revenue arising from rendering of services is generally recognized by the percentage-

of-completion method at the balance sheet date. In addition, revenue arising from interest, dividends or royalties is recognized

when it is probable that future economic benefits will flow into the Company and those benefits can be measured reliably.

In the case of subsidiaries in financial business, interest revenues earned on financial assets are recognized as time passes

using the level yield method, and fees and commissions in return for services rendered are recognized as services are

provided.

Allowance for Doubtful Accounts

The Company provides an allowance for doubtful accounts based on management’s estimated loss on uncollectible accounts.

Inventories

Inventories are stated at the lower of cost or net realizable value, cost being determined by the moving average cost method,

except for materials in transit for which cost is determined using the specific identification method. Valuation loss incurred

when the market value of an inventory falls below its carrying amount is added to the cost of goods sold.

Investments in Securities Other Than Those Accounted for Using the Equity Method

Classification of Securities

At acquisition, the Company classifies securities into one of the three categories; trading, held-to-maturity or available-for-sale.

Trading securities are those that were acquired principally to generate profits from short-term fluctuations in prices. Held-to-

maturity securities are those with fixed or determinable payments and fixed maturity that the Company has the positive intent

and ability to hold to maturity. Available-for-sale securities are those not classified as either held-to-maturity or trading

securities. Trading securities are classified as short-term investment securities, whereas available-for-sale and held-to-maturity

securities are classified as long-term investment securities, except for those whose maturity dates or whose likelihood of being

disposed of are within one year from balance sheet date, which are classified as short-term investment securities.