Hyundai 2005 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2005 Hyundai annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

|

|

76

HYUNDAI MOTOR COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2005 AND 2004

The Company assesses any possible recognition of impairment loss when there is an indication that expected future economic

benefits of a tangible asset is considerably less than its carrying amount, as a result of technological obsolescence, rapid

declines in market value or other causes of impairment. When it is determined that an asset may have been impaired and that

its estimated total future cash flows from continued use or disposal is less than its carrying amount, the carrying amount of a

tangible asset is reduced to its recoverable amount and the difference is recognized as an impairment loss. If the recoverable

amount of the impaired asset exceeds its carrying amount in subsequent reporting period, the amount equal to the excess is

treated as the reversal of the impairment loss; however, it cannot exceed the carrying amount that would have been

determined had no impairment loss been recognized.

Intangibles

Intangible assets are stated at cost, net of accumulated amortization. Subsequent expenditures on intangible assets after their

purchases or completions, which will probably enable the assets to generate future economic benefits and can be measured

and attributed to the assets reliably, are treated as additions to intangible assets.

Amortization is computed using the straight-line method based on the estimated useful lives of the assets as follows:

If the recoverable amount of an intangible asset becomes less than its carrying amount as a result of obsolescence, sharp

decline in market value or other causes of impairment, the carrying amount of an intangible asset is adjusted to its recoverable

amount and the reduced amount is recognized as impairment loss. If the recoverable amount of a previously impaired

intangible asset exceeds its carrying amount in subsequent periods, an amount equal to the excess is recorded as reversal of

impairment loss; however, it cannot exceed the carrying amount that would have been determined had no impairment loss

been recognized in prior years.

Financing Costs

The Company recognizes all financing costs including interest expense and similar expenses in current operations.

Valuation of Receivables and Payables at Present Value

Receivables and payables arising from long-term installment transactions, long-term cash loans (borrowings) and other similar

loan (borrowing) transactions are stated at present value, if the difference between nominal value and present value is material.

The present value discount is amortized using the effective interest rate method.

Discount on Debentures

Discount on debentures is the difference between the issued amount and the face value of debentures. It is presented as a

deduction from to the face value of debentures and amortized over the redemption period of the debentures using the effective

interest rate method. Amortization of discount is recognized as interest expense on the debentures.

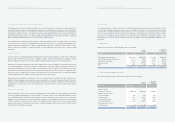

Useful lives (years)

Goodwill (Negative goodwill) 5 – 20

Industrial property rights 2 – 40

Development costs 3 – 10

Other 2 – 50

75

HYUNDAI MOTOR COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2005 AND 2004

Investment Securities Accounted for Using the Equity Method

Equity securities held for investment in companies in which the Company is able to exercise significant influence over the

operating and financial policies of the investees are accounted for using the equity method. The Company’s share in the net

income or net loss of investees is reflected in current operations. The changes in the retained earnings, capital surplus or other

capital accounts of investees are accounted for as an adjustment to retained earnings, to capital surplus or to capital

adjustments.

The difference between the cost of the investment and the investor’s share of the net fair value of the investee’s identifiable

assets and liabilities at the date of acquisition is amortized over 20 years for goodwill or reversed over the remaining weighted

average useful life of the identifiable acquired depreciable assets for negative goodwill, which does not exceed the fair value of

non-monetary assets acquired, using the straight-line method. Negative goodwill that exceeds the fair value of non-monetary

assets acquired is credited to operations in the year of purchase.

The Company’s portion of profits and losses resulting from inter-company transactions that are recognized in assets, such as

inventories and fixed assets, are eliminated and charged to equity securities accounted for using the equity method. However,

if the investee is a consolidated subsidiary, unrealized profits and losses resulting from sales of assets from the Company to

investee are eliminated in full. Also, if the investee is a consolidated subsidiary, the differences between the cost of the

investment and the investor’s share of the net fair value of the investee’s identifiable assets and liabilities, which occurred from

additional purchases of investee’s shares or changes in ratio of shareholding due to capital increase in investee, are reflected in

capital adjustments. The differences between the sale amount and book value of the investment securities where the investee

remains as a consolidated subsidiary after sales of some portion of investment securities in the consolidation subsidiary are

reflected in capital adjustments.

If an investor’s share of losses of an investee equals or exceeds its interest in the investee, the investor discontinues

recognizing its share of further losses. If the investee subsequently reports profits, the investor resumes recognizing its share

of those profits only after its share of the profits equals the share of losses not recognized. Also, if the recoverable amount of

investments in investee becomes less than its carrying amount, the Company recognizes impairment loss.

Property, Plant and Equipment and Related Depreciation

Property, plant and equipment are recorded at cost, except for assets revalued upward in accordance with the Asset

Revaluation Law of Korea. Routine maintenance and repairs are expensed as incurred. Expenditures that result in the

enhancement of the value or extension of the useful lives of the facilities involved are treated as additions to property, plant and

equipment.

Depreciation is computed using the straight-line method based on the estimated useful lives of the assets as follows:

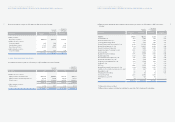

Useful lives (years)

Buildings and structures 2 – 60

Machinery and equipment 2 – 16

Vehicles 3 – 10

Tools, dies and molds 2 – 16

Other equipment 3 – 10