Hyundai 2005 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2005 Hyundai annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

|

|

72

HYUNDAI MOTOR COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2005 AND 2004

In relation with such change, the amounts of relevant accounts retroactively calculated in prior years’ financial statements are as

follows:

The Company did not retroactively apply SKAS No. 15 and 17 to the prior year financial statements, in accordance with the

provisions in SKAS No.15 and 17. However, the Company recalculated the beginning balance of accrued warranties in

accordance with SKAS No.17, which requires the recalculation of the beginning balance based on this revised standard in case

the retroactive method is not applied. This recalculation decreased the beginning balance of accrued warranties and deferred

tax assets by ₩730,008 million (US$720,640 thousand) and ₩200,753 million (US$198,177 thousand), respectively, and

increased the beginning balance of retained earnings by ₩505,626 million (US$499,137 thousand).

The significant accounting policies followed by the Company in the preparation of its consolidated financial statements are

summarized below.

Principles of Consolidation

The consolidated financial statements include the individual accounts of the Company and its domestic and foreign subsidiaries

over which the Company has control, is the largest shareholder and owns more than 30 percent of the voting shares, except for

companies with total assets of less than ₩7,000 million (US$6,910 thousand) at the end of the preceding fiscal year.

Investments in affiliates in which a consolidated entity is able to exercise significant influence over the operating and financial

policies of a non-consolidated company are accounted for using the equity method. Significant influence is deemed to exist

when the investor owns more than twenty percent of the investee’s voting shares unless there is evidence to the contrary. If the

changes in the investment value due to the changes in the net assets of affiliates, whose individual beginning balance of total

assets or paid-in capital at the date of its establishment is less than ₩7,000 million (US$6,910 thousand), are not material,

investments in affiliates can be excluded from using the equity method.

The investment account of the Company and corresponding equity accounts of subsidiaries are eliminated at the dates the

Company obtained control over the subsidiaries. The difference between the investment cost and the fair value of the

Company’s portion of assets acquired less liabilities assumed of a subsidiary is accounted for as goodwill or negative goodwill.

Goodwill is amortized on a straight-line basis over its useful life, not exceeding twenty years. The amount of negative goodwill

not exceeding the total fair value of acquired identifiable non-monetary assets is recognized as income on a straight-line basis

over the remaining weighted average useful life of the identifiable acquired depreciable assets and the amount of negative

goodwill in excess of the total fair value of the acquired identifiable non-monetary assets is recognized as non-operating gain at

the date of acquisition.

When the Company acquires additional interests in a subsidiary after obtaining control over the subsidiary, the difference

between incremental price paid by the Company and the amount of incremental interest in the shareholders’ equity of the

subsidiary is reflected in the consolidated capital surplus. In case a subsidiary still belongs to a consolidated economic entity

after the Company disposes a portion of the stocks of subsidiaries to non-subsidiary parties, gain or loss on disposal of the

subsidiary’s stock is accounted for as consolidated capital surplus.

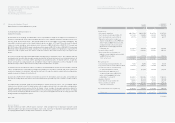

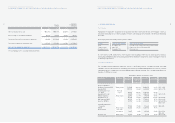

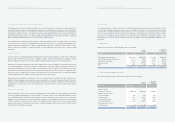

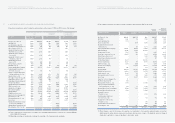

Korean Won (In millions, except per share amounts)

2002 2003 2004

Deferred income tax assets 1,057,244 1,274,817 947,077

Retained earnings 3,628,319 5,029,254 6,328,355

Capital adjustments (244,521) (113,760) (216,453)

Minority interests 2,936,258 3,383,279 4,000,714

Ordinary income 2,770,680 2,714,107 2,719,948

Net income 1,473,261 1,690,481 1,641,941

Ordinary income per common share 6,491 7,441 7,193

Earnings per common share 6,491 7,441 7,193

71

HYUNDAI MOTOR COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2005 AND 2004

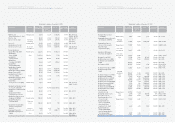

(*) Local currency in foreign subsidiaries is translated into Korean won using the market average exchange rate announced by

Seoul Money Brokerage Services, Ltd. at December 31, 2005.

(**) Shares and ownership are calculated by combining the shares and ownership, which the Company and its subsidiaries hold

as of December 31, 2005. Indirect ownership represents subsidiaries’ holding ownership.

In 2005, the Company added three domestic companies, including Partecs Co., Hyundai Autonet Co., Ltd. and Haevichi Leisure

Co., Ltd., and six overseas companies, including Hyundai Motor (UK) Ltd. (HMUK), Hyundai Motor Europe Technical Center

GmbH (HMETC), Hyundai Assan Otomotive Sannayi Ve Ticaret A.S.(HAOSVT), Hyundai Motor Group (China) Ltd., Hyundai

Jingxian Motor Safeguard Service Co. Ltd. and Wia Automotive Parts (WAP), to its consolidated subsidiaries due to the

acquisition of ownership enabling the Company and its subsidiaries to exercise substantial control or the increase in individual

assets at the end of the preceding year exceeding the required level of ₩7,000 million (US$6,910 thousand) for consolidation

with substantial control.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES:

Basis of Consolidated Financial Statement Presentation

The Company maintains its official accounting records in Korean won and prepares statutory consolidated financial statements

in the Korean language (Hangul) in conformity with the accounting principles generally accepted in the Republic of Korea. Certain

accounting principles applied by the Company that conform with financial accounting standards and accounting principles in the

Republic of Korea may not conform with generally accepted accounting principles in other countries. Accordingly, these financial

statements are intended for use by those who are informed about Korean accounting principles and practices. The accompanying

financial statements have been condensed, restructured and translated into English from the Korean language financial

statements. Certain information included in the Korean language financial statements, but not required for a fair presentation of

the Company and its subsidiaries’ financial position, results of operations or cash flows, is not presented in the accompanying

financial statements.

The accompanying financial statements are stated in Korean Won, the currency of the country in which the Company is

incorporated and operates. The translation of Korean Won amounts into U.S. dollar amounts is included solely for the

convenience of readers outside of the Republic of Korea and has been made at the rate of ₩1,013.00 to US$1.00 at December

31, 2005, the market average exchange rate announced by Seoul Money Brokerage Services, Ltd.. Such translations should

not be construed as representations that the Korean Won amounts could be converted at that or any other rate.

The Company prepared its financial statements as of December 31, 2005 in accordance with Financial Accounting Standards

and Statements of Korea Accounting Standards (“SKAS”) in the Republic of Korea.

In 2005, the Company additionally adopted SKAS No. 15 - “Investments in Associates”, No. 16 - “Income Taxes” and No. 17 -

“Provisions, Contingent Liabilities and Contingent Assets”, which are effective from January 1, 2005.

The accompanying balance sheet as of December 31, 2004 and the accompanying statements of income, changes in

shareholders’ equity and cash flows for year ended December 31, 2004, which are presented for comparative purposes, have

been restated to reflect the adjustments resulting from retroactive application of SKAS No.16. As a result of the restatement,

total assets and net equity as of December 31, 2004 decreased by ₩343,431 million (US$339,024 thousand), and net income

for the year then ended decreased by ₩44,890 million (US$ 44,314 thousand).