Family Dollar 2013 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2013 Family Dollar annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

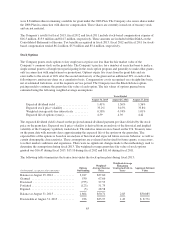

provides for two, one-year extensions that require lender consent. Any borrowings under the credit facility accrue

interest at a variable rate based on short-term market interest rates. The credit facility replaced the previous

364-day $250 million unsecured revolving credit facility.

On August 17, 2011, the Company entered into a new five-year unsecured revolving credit facility with a

syndicate of lenders for borrowings of up to $300 million. The credit facility matures on August 17, 2016, and

provides for two, one-year extensions that require lender consent. Any borrowings under the credit facility accrue

interest at a variable rate based on short-term market interest rates. The credit facility replaced the Company’s

previous five-year $200 million unsecured credit facility.

As of August 31, 2013, the Company had no outstanding borrowings under the credit facilities. As of August 25,

2012, the Company had $15.0 million in outstanding borrowings under the credit facilities. During fiscal 2013,

the Company had an average daily outstanding balance of $141.5 million at an annualized weighted-average

interest rate of 1.5% under its unsecured revolving credit facilities. The credit facilities contain certain restrictive

financial covenants, which include a consolidated debt to consolidated total capitalization ratio, a fixed charge

coverage ratio, and a priority debt to consolidated net worth ratio. As of August 31, 2013, the Company was in

compliance with all such covenants.

7. Sale-Leaseback Transactions

During fiscal 2013, the Company completed sale-leaseback transactions under which it sold a total of 256 stores

to unrelated third-parties. Net proceeds from these sales were approximately $335.0 million. Upon closing of the

transactions, the Company realized a gain on the sale of the stores of $84.7 million, of which approximately

$2.4 million was recognized immediately and approximately $82.3 million was deferred and will be amortized

over the initial lease term.

During fiscal 2012, the Company completed sale-leaseback transactions under which it sold a total of 276 stores

to unrelated third-parties. Net proceeds from these sales were $359.7 million. Upon closing of the transactions,

the Company deferred a gain of approximately $171.6 million realized on the sale of the stores and will amortize

the gain over the initial lease term.

Concurrent with these sales in fiscal 2013 and 2012, the Company entered into agreements to lease the properties

back from the purchasers over initial lease terms of 15 years. The master leases for the 532 stores includes an

initial term of 15 years and four, five-year renewal options and provides for the Company to evaluate each store

individually upon certain events during the life of the lease, including individual renewal options. The Company

classified these leases as operating leases, actively uses the leased properties and considers the leases as normal

leasebacks under ASC 840. The deferred gain on these transactions includes both a current and non-current

portion, with the current portion based on the amount that is expected to amortize over the next 12 months. The

current and non-current portions are included in Accrued Liabilities and Deferred Gain, respectively, on the

Consolidated Balance Sheets.

Additionally, in fiscal 2013 the Company entered into an agreement with an unrelated third-party to construct

new stores to lease under a build-to-suit structure. The transaction allows for the construction of stores up to

$125 million through June 19, 2014. Under this agreement, the unrelated third-party will fund the construction of

the stores, and the Company will act as the construction agent during the construction period. Upon the

completion of the stores’ construction, the Company will lease the property under a 15-year operating lease. Each

of the assets currently included in the portfolio are classified as operating leases under ASC 840, and all new

transactions associated with this agreement will be assessed for classification as an operating lease. In connection

with this agreement, the Company has sold 29 parcels of land to the unrelated third-party for proceeds of

approximately $10.2 million. These sales qualify as sale-leaseback transactions under ASC 840.

55