Family Dollar 2013 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2013 Family Dollar annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

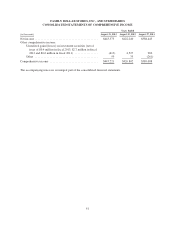

(“ASU 2013-02”). ASU 2013-02 requires an entity to provide information about the amounts reclassified out of

accumulated other comprehensive income by component. The ASU is effective for annual periods and interim

periods within those periods beginning after December 15, 2012. The ASU will be effective for us beginning in

the first quarter of fiscal 2014 and is not expected to have a material impact on our Consolidated Financial

Statements.

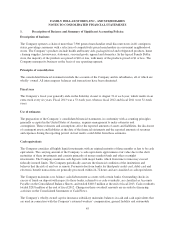

Critical Accounting Policies

Our financial statements have been prepared in accordance with accounting policies generally accepted in

the United States of America. Our discussion and analysis of our financial condition and results of operations are

based on these financial statements. The preparation of these financial statements requires the application of

accounting policies in addition to certain estimates and judgments by our management. Our estimates and

judgments are based on currently available information, historical results and other assumptions we believe are

reasonable. Actual results could differ from these estimates.

We believe the following accounting principles are critical because they involve significant judgments,

assumptions and estimates used in the preparation of our Consolidated Financial Statements.

Merchandise Inventories:

Our inventories are valued using the retail method, based on retail prices less mark-on percentages, which

approximates the lower of first-in, first-out (FIFO) cost or market. We record adjustments to inventory through

cost of sales when retail price reductions, or markdowns, are taken against on-hand inventory. In addition, we

make estimates and judgments regarding, among other things, initial markups, markdowns, future demand for

specific product categories and market conditions, all of which can significantly impact inventory valuation.

These estimates and judgments are based on the application of a consistent methodology each period. While we

believe that we have sufficient current and historical knowledge to record reasonable estimates for these

components, if actual demand or market conditions are different than our projections, it is possible that actual

results could differ from recorded estimates. This risk is generally higher for seasonal merchandise than for non-

seasonal merchandise. We estimate inventory losses for damaged, lost or stolen inventory (inventory shrinkage)

for the period from the most recent physical inventory to the financial statement date. The accrual for estimated

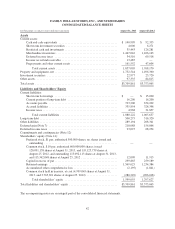

inventory shrinkage was $77.5 million as of the end of fiscal 2013 and $58.8 million as of the end of fiscal 2012.

The accrual for estimated inventory shrinkage is based on the trailing twelve-month actual inventory shrinkage

rate and can fluctuate from period to period based on the timing of the physical inventory counts. Stores receive a

physical inventory at least annually. There were no material changes in the estimates or assumptions related to

the valuation of inventory during fiscal 2013.

Property and Equipment:

We state property and equipment at cost. We calculate depreciation for financial reporting purposes using

the straight-line method over the estimated useful lives of the related assets. For leasehold improvements, this

depreciation is over the shorter of the term of the related lease (generally between five and fifteen years),

including reasonably assured renewal options, or the asset’s useful economic life. The valuation and

classification of these assets and the assignment of useful depreciable lives involves significant judgments and

the use of estimates. The increase in gross property and equipment, before depreciation, is not commensurate

with capital expenditures due to the significant amount of assets sold during the year under sale-leaseback

transactions. We generally do not assign salvage value to property and equipment. We review property and

equipment for impairment whenever events or changes in circumstances indicate that the carrying amount of an

asset may not be recoverable. Historically, our impairment losses on fixed assets, which typically relate to

normal store closings, have not been material to our financial position and results of operations. There were no

material changes in the estimates or assumptions related to the valuation and classification of property and

equipment during fiscal 2013. See Notes 1 and 5 to the Consolidated Financial Statements included in this Report

for more information on property and equipment.

35