Family Dollar 2013 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2013 Family Dollar annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

Insurance Liabilities:

We are primarily self-insured for health care, property loss, workers’ compensation, general liability, and

auto liability costs. These costs are significant primarily due to the large number of our retail locations and

employees. Our self-insurance liabilities are based on the total estimated costs of claims filed and estimates of

claims incurred but not reported, less amounts paid against such claims, and are not discounted. We review

current and historical claims data in developing our estimates. We also use information provided by outside

actuaries with respect to medical, workers’ compensation, general liability, and auto liability claims. The

insurance liabilities we record are mainly influenced by changes in payroll expense, sales, number of vehicles,

and the frequency and severity of claims. The estimates of more recent claims are more volatile and more likely

to change than older claims. If the underlying facts and circumstances of the claims change or if the historical

trend is not indicative of future trends, then we may be required to record additional expense or a reduction in

expense, which could be material to our reported financial condition and results of operations.

We record our liabilities for workers’ compensation, general liability and auto liability costs on a gross

basis, and record a separate insurance asset for amounts recoverable under stop-loss insurance policies on the

Consolidated Balance Sheets. In addition, our gross liabilities and the related insurance asset are separated into

current and non-current amounts on the Consolidated Balance Sheets.

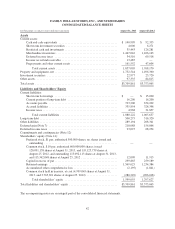

Our total liabilities for workers’ compensation, general liability and auto liability costs were $232.1 million

($52.2 million current and $179.9 million non-current) as of the end of fiscal 2013 and $236.7 million

($52.0 million current and $184.6 million non-current) as of the end of fiscal 2012. The current portion of the

liabilities is included in Accrued Liabilities on the Consolidated Balance Sheets, and the non-current portion is

included in Other Liabilities. The insurance assets related to these amounts totaled $31.7 million ($2.5 million

current and $29.2 million non-current) as of the end of fiscal 2013 and $34.8 million ($2.9 million current and

$31.9 million non-current) as of the end of fiscal 2012. The current portion of the assets is included in

prepayments and Other Current Assets on the Consolidated Balance Sheets, and the non-current portion is

included in Other Assets. There were no other material estimates for insurance liabilities during fiscal 2013 or

fiscal 2012. Our insurance expense during fiscal 2013, fiscal 2012 and fiscal 2011 was impacted by changes in

our liabilities for workers’ compensation, general liability and auto liability costs.

Contingent Income Tax Liabilities:

We are subject to routine income tax audits that occur periodically in the normal course of business, and we

record contingent income tax liabilities related to our uncertain tax positions. Our liabilities related to uncertain

tax positions require an assessment of the probability of the income-tax-related exposures and settlements and are

influenced by our historical audit experiences with various taxing authorities as well as by current income tax

trends. If circumstances change, we may be required to record adjustments that could be material to our reported

financial condition and results of operations. Our liabilities related to uncertain tax positions were $30.2 million

as of the end of fiscal 2013 and $22.4 million as of the end of fiscal 2012. There were no material changes in the

estimates or assumptions used to determine contingent income tax liabilities during fiscal 2013. See Note 10 to

the Consolidated Financial Statements included in this Report for more information on our contingent income tax

liabilities.

Contingent Legal Liabilities:

We are involved in numerous legal proceedings and claims. Our accruals, if any, related to these

proceedings and claims are based on a determination of whether or not the loss is both probable and estimable.

We review outstanding claims and proceedings with external counsel to assess probability and estimates of loss.

We re-evaluate the claims and proceedings each quarter or as new and significant information becomes available,

and we adjust or establish accruals, if necessary. If circumstances change, we may be required to record

adjustments that could be material to our reported financial condition and results of operations. Our total legal

liabilities were not material as of the end of fiscal 2013 or fiscal 2012. There were no material changes in the

36