Dish Network 2007 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2007 Dish Network annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

|

|

Table of Contents

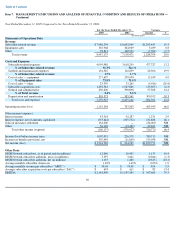

The improvement from 2004 to 2005 was partially offset by the following financing sources of cash:

Other Liquidity Items

Subscriber turnover.

Our percentage monthly subscriber churn for the year ended December 31, 2006 was 1.64%, compared to percentage

subscriber churn for 2005 of 1.65%. Our future subscriber churn may be negatively impacted by a number of factors, including but not limited

to, an increase in competition from existing competitors and new entrants offering more compelling promotions, as well as new advanced

products and services. Competitor bundling of video services with 2-way high speed Internet access and telephone services may contribute

more significantly to churn over time. There can be no assurance that these and other factors will not contribute to relatively higher churn than

we have experienced historically. Additionally, certain of our promotions allow consumers with relatively lower credit scores to become

subscribers, and these subscribers typically churn at a higher rate. However, these subscribers are also acquired at a lower cost resulting in a

smaller economic loss upon disconnect.

Additionally, as the size of our subscriber base increases, even if our churn percentage remains constant or declines, increasing numbers of

gross new DISH Network subscribers are required to sustain net subscriber growth.

Increases in theft of our signal, or our competitors’ signals, also could cause subscriber churn to increase in future periods. We use microchips

embedded in credit card-sized access cards, called “smart cards,” or in security chips in our EchoStar receiver systems to control access to

authorized programming content. Our signal encryption has been compromised by theft of service and could be further compromised in the

future. We continue to respond to compromises of our encryption system with security measures intended to make signal theft of our

programming more difficult. During 2005, we completed the replacement of our smart cards. While the smart card replacement did not fully

secure our system, we continue to implement software patches and other security measures to help protect our service. There can be no

assurance that our security measures will be effective in reducing theft of our programming signals. If we are required to replace existing smart

cards, the cost could exceed $100.0 million.

Subscriber acquisition and retention costs.

Our subscriber acquisition and retention costs can vary significantly from period to period which

can in turn cause significant variability to our net income (loss) and free cash flow between periods. Our “Subscriber acquisition costs,” SAC

and “Subscriber-related expenses” may materially increase to the extent that we introduce more aggressive promotions in the future if we

determine they are necessary to respond to competition, or for other reasons.

Capital expenditures resulting from our equipment lease program for new subscribers have been, and we expect will continue to be, partially

mitigated by, among other things, the redeployment of equipment returned by disconnecting lease program subscribers. However, to remain

competitive we will have to upgrade or replace subscriber equipment periodically as technology changes, and the associated costs may be

substantial. To the extent technological changes render existing equipment obsolete, we would cease to benefit from the SAC reduction

associated with redeployment of that returned lease equipment.

Several years ago, we began deploying satellite receivers capable of exploiting 8PSK modulation technology. Since that technology is now

standard in all of our new satellite receivers, our cost to migrate programming channels to that technology in the future will be substantially

lower than if it were necessary to replace all existing consumer equipment. As we continue to implement 8PSK technology, bandwidth

efficiency will improve, significantly increasing the number of programming channels we can transmit over our existing satellites as an

alternative or supplement to the acquisition of additional spectrum or the construction of additional satellites. New channels we

57

Item 7.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS —

Continued

•

During 2004, we paid a cash dividend of $455.7 million to holders of our Class A and Class B common stock.

• During 2005, we repurchased approximately 13.2 million shares of our Class A common stock in open market transactions for a total

cost of $362.5 million compared to approximately 25.9 million shares at a total cost of $809.6 million during 2004.

• During 2004, we sold $1.0 billion principal amount of our 6 5/8% Senior Notes due 2014 and $25.0 million 3% Convertible

Subordinated Note due 2011 to CenturyTel Service Group L.L.C.