Cisco 2005 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2005 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

|

|

46

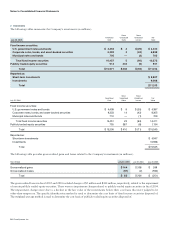

Computation of Net Income Per Share Basic net income per share is computed using the weighted-average number of common shares

outstanding during the period. Diluted net income per share is computed using the weighted-average number of common shares and

dilutive potential common shares outstanding during the period. Diluted net loss per share is computed using the weighted-average

number of common shares and excludes dilutive potential common shares outstanding, as their effect is antidilutive. Dilutive potential

common shares consist primarily of employee stock options and restricted common stock.

Foreign Currency Translation Assets and liabilities of non-U.S. subsidiaries that operate in a local currency environment, where that local

currency is the functional currency, are translated to U.S. dollars at exchange rates in effect at the balance sheet date, with the

resulting translation adjustments directly recorded to a separate component of accumulated other comprehensive income.

Income and expense accounts are translated at average exchange rates during the year. Translation adjustments are recorded in other

income (loss), net, where the U.S. dollar is the functional currency.

Derivative Instruments The Company recognizes derivative instruments as either assets or liabilities in the Consolidated Balance Sheets

and measures those instruments at fair value. The accounting for changes in the fair value of a derivative depends on the intended use

of the derivative and the resulting designation.

For a derivative instrument designated as a fair value hedge, the gain or loss is recognized in earnings in the period of change

together with the offsetting loss or gain on the hedged item attributed to the risk being hedged. For a derivative instrument designated

as a cash flow hedge, the effective portion of the derivative’s gain or loss is initially reported as a component of accumulated other

comprehensive income and subsequently reclassified into earnings when the hedged exposure affects earnings. The ineffective portion

of the gain or loss is reported in earnings immediately. For derivative instruments that are not designated as accounting hedges,

changes in fair value are recognized in earnings in the period of change.

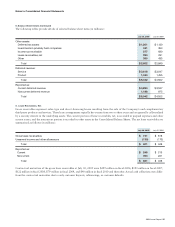

The fair value of derivative instruments as of July 30, 2005 was $41 million and the amount was not material as of July 31, 2004.

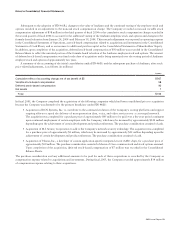

The changes in fair value during fiscal 2005 and 2004 were not material. During fiscal 2005 and 2004, there were no significant gains

or losses recognized in earnings for hedge ineffectiveness. The Company did not discontinue any hedges because it was probable that

the original forecasted transactions would not occur.

Consolidation of Variable Interest Entities Financial Accounting Standards Board (FASB) Interpretation No. 46, “Consolidation of Variable

Interest Entities” (“FIN 46”), was issued in January 2003. FIN 46 requires that if an entity is the primary beneficiary of a variable

interest entity, the assets, liabilities, and results of operations of the variable interest entity should be included in the consolidated

financial statements of the entity. FASB Interpretation No. 46(R), “Consolidation of Variable Interest Entities” (“FIN 46(R)”),

was issued in December 2003. The Company adopted FIN 46(R) effective January 24, 2004, and recorded a noncash cumulative

stock compensation charge of $567 million, net of tax, relating to the consolidation of Andiamo Systems, Inc. (“Andiamo”).

For additional information regarding Andiamo, see Note 3 to these Consolidated Financial Statements. For additional information

regarding variable interest entities, see Note 8 to these Consolidated Financial Statements.

Minority Interest The Company consolidated its investment in a venture fund managed by SOFTBANK Corp. and its affiliates

(“SOFTBANK”). As of July 30, 2005, minority interest of $7 million represents SOFTBANK’s share of the venture fund. The remaining

minority interest of $3 million represents the preferred stockholders’ proportionate share of the equity of Cisco Systems, K.K. (Japan).

At July 30, 2005, the Company owned all issued and outstanding common stock, amounting to 99.0% of the aggregate voting rights

of Cisco Systems, K.K. (Japan). Each share of preferred stock is convertible into one share of common stock of Cisco Systems, K.K.

(Japan) at any time at the option of the holder.

Use of Estimates The preparation of financial statements and related disclosures in conformity with accounting principles generally

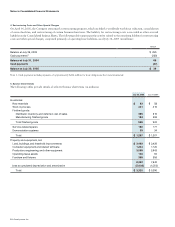

accepted in the United States requires management to make estimates and judgments that affect the amounts reported in the

Consolidated Financial Statements and accompanying notes. Estimates are used for revenue recognition, allowance for doubtful

accounts and sales returns, allowance for inventory, warranty costs, investment impairments, goodwill impairments, income taxes,

and loss contingencies, among others. The actual results experienced by the Company may differ materially from management’s estimates.

Impairment of Long-Lived Assets Long-lived assets and certain identifiable intangible assets to be held and used are reviewed for

impairment whenever events or changes in circumstances indicate that the carrying amount of such assets may not be recoverable.

Determination of recoverability of long-lived assets is based on an estimate of undiscounted future cash flows resulting from the use

of the asset and its eventual disposition. Measurement of an impairment loss for long-lived assets and certain identifiable intangible

assets that management expects to hold and use is based on the fair value of the asset. Long-lived assets and certain identifiable

intangible assets to be disposed of are reported at the lower of carrying amount or fair value less costs to sell.

Notes to Consolidated Financial Statements