Cisco 2005 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2005 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

|

|

29

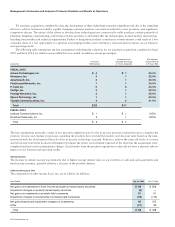

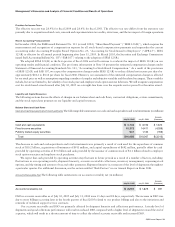

Provision for Income Taxes

The effective tax rate was 28.6% for fiscal 2005 and 28.9% for fiscal 2004. The effective tax rate differs from the statutory rate

primarily due to acquisition-related costs, research and experimentation tax credits, state taxes, and the tax impact of foreign operations.

During the fourth quarter of fiscal 2005, the Internal Revenue Service completed its examination of our federal income tax

returns for the fiscal years ended July 25, 1998 through July 28, 2001. Based on the results of the examination, we have decreased

previously recorded tax reserves by approximately $110 million and decreased income tax expense by a corresponding amount.

This decrease to the provision for income taxes was offset by increases to the provision for income taxes of $57 million related to a

fourth quarter fiscal 2005 intercompany restructuring of certain of our foreign operations and $70 million related to the effects of new

U.S. tax regulations effective in fiscal 2005 that require intercompany reimbursement of certain stock-based compensation expenses.

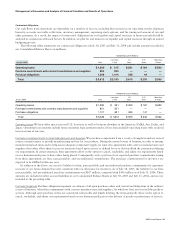

Our future effective tax rates could be adversely affected by earnings being lower than anticipated in countries where we have

lower statutory rates and higher than anticipated in countries where we have higher statutory rates, by changes in the valuation of our

deferred tax assets or liabilities, or by changes in tax laws, regulations, accounting principles, or interpretations thereof. In addition,

we are subject to the continuous examination of our income tax returns by the Internal Revenue Service and other tax authorities.

We regularly assess the likelihood of adverse outcomes resulting from these examinations to determine the adequacy of our

provision for income taxes.

On October 22, 2004, the American Jobs Creation Act of 2004 (the “Jobs Creation Act”) was signed into law. The Jobs

Creation Act creates a temporary incentive for U.S. corporations to repatriate accumulated income earned abroad by providing an

85 percent dividends received deduction for certain dividends from controlled foreign corporations. In the first quarter of fiscal 2006,

we distributed cash from our foreign subsidiaries and will report an extraordinary dividend (as defined in the Jobs Creation Act) of

$1.2 billion and a related tax liability of approximately $63 million in our fiscal 2006 federal income tax return. This amount was

previously provided for in the provision for income taxes and is included in income taxes payable.

In July 2005, the Financial Accounting Standards Board (FASB) issued an Exposure Draft of a proposed Interpretation

“Accounting for Uncertain Tax Positions - an interpretation of FASB Statement No. 109.” Under the proposed Interpretation,

a company would recognize in its financial statements its best estimate of the benefit of a tax position, only if the tax position

is considered probable of being sustained on audit based solely on the technical merits of the tax position. In evaluating whether

the probable recognition threshold has been met, the proposed Interpretation would require the presumption that the tax position

will be evaluated during an audit by taxing authorities. The proposed Interpretation would be effective as of the end of the first fiscal

year ending after December 15, 2005, with a cumulative effect of a change in accounting principle to be recorded upon the initial

adoption. The proposed Interpretation would apply to all tax positions and only benefits from tax positions that meet the probable

recognition threshold at or after the effective date would be recognized. We are currently analyzing the proposed Interpretation and

have not determined its potential impact on our Consolidated Financial Statements. While we cannot predict with certainty the

rules in the final Interpretation, there is risk that the final Interpretation could result in a cumulative effect charge to earnings upon

adoption, increases in future effective tax rates, and/or increases in future interperiod effective tax rate volatility.

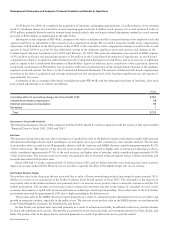

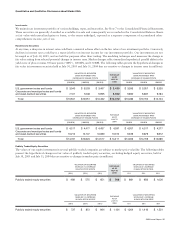

Cumulative Effect of Accounting Change, Net of Tax

In April 2001, we entered into a commitment to provide convertible debt funding of approximately $84 million to Andiamo

Systems, Inc. (“Andiamo”), a privately held storage switch developer. This debt was convertible into approximately 44% of the

equity of Andiamo. In connection with this investment, we obtained a call option that provided us the right to purchase Andiamo.

The purchase price under the call option was based on a valuation of Andiamo using a negotiated formula. On August 19, 2002,

we entered into a definitive agreement to acquire Andiamo, which represented the exercise of our rights under the call option. We also

entered into a commitment to provide nonconvertible debt funding to Andiamo of approximately $100 million through the close of

the acquisition. Substantially all of the convertible debt funding of $84 million and nonconvertible debt funding of $100 million

was expensed as R&D costs.

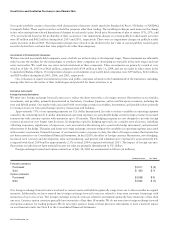

We adopted FASB Interpretation No. 46(R), “Consolidation of Variable Interest Entities” (“FIN 46(R)”), effective January

24, 2004. We evaluated our debt investment in Andiamo and determined that Andiamo was a variable interest entity under FIN

46(R). We concluded that we were the primary beneficiary as defined by FIN 46(R) and, therefore, accounted for Andiamo as if we

had consolidated Andiamo since our initial investment in April 2001. The consolidation of Andiamo from the date of our initial

investment required accounting for the call option as a repurchase right. Under FASB Interpretation No. 44, “Accounting for Certain

Transactions Involving Stock Compensation,” and related interpretations, variable accounting was required for substantially

all Andiamo employee stock and options because the ending purchase price was primarily derived from a revenue-based formula.

Effective January 24, 2004, the last day of the second quarter of fiscal 2004, we recorded a noncash cumulative stock compensation

charge of $567 million, net of tax (representing the amount of variable compensation from April 2001 through January 2004).

This charge was reported as a separate line item in the Consolidated Statements of Operations as a cumulative effect of accounting

change, net of tax. The charge was based on the value of the Andiamo employee stock and options and their vesting from the adoption

of FIN 46(R) pursuant to the formula-based valuation.

Management’s Discussion and Analysis of Financial Condition and Results of Operations