Cisco 2005 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2005 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

|

|

21

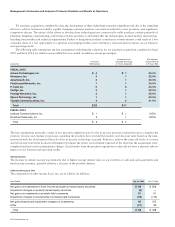

We had no provision for doubtful accounts in fiscal 2005. Our provision (credit) for doubtful accounts was $19 million and

($59) million for fiscal 2004 and 2003, respectively. If a major customer’s creditworthiness deteriorates, or if actual defaults are

higher than our historical experience, or if other circumstances arise, our estimates of the recoverability of amounts due to us could

be overstated, and additional allowances could be required, which could have an adverse impact on our revenue.

A reserve for future sales returns is established based on historical trends in product return rates. The reserve for future sales

returns as of July 30, 2005 and July 31, 2004 was $63 million and $74 million, respectively, and was recorded as a reduction of our

accounts receivable. If the actual future returns were to deviate from the historical data on which the reserve had been established,

our revenue could be adversely affected.

Allowance for Inventory

Our inventory balance was $1.3 billion as of July 30, 2005, compared with $1.2 billion as of July 31, 2004. Our inventory allowance

as of July 30, 2005 was $159 million, compared with $139 million as of July 31, 2004. We provide allowances for inventory based on

excess and obsolete inventories determined primarily by future demand forecasts. The allowance is measured as the difference between

the cost of the inventory and market based upon assumptions about future demand and is charged to the provision for inventory, which

is a component of our cost of sales. At the point of the loss recognition, a new, lower-cost basis for that inventory is established, and

subsequent changes in facts and circumstances do not result in the restoration or increase in that newly established cost basis.

Our provision for inventory was $221 million, $205 million, and $70 million for fiscal 2005, 2004, and 2003, respectively.

If there were to be a sudden and significant decrease in demand for our products, or if there were a higher incidence of inventory

obsolescence because of rapidly changing technology and customer requirements, we could be required to increase our inventory

allowances, and our gross margin could be adversely affected. Inventory management remains an area of focus as we balance the

need to maintain strategic inventory levels to ensure competitive lead times and the risk of inventory obsolescence.

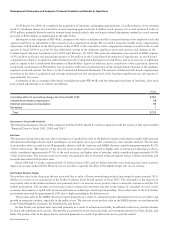

Warranty Costs

The liability for product warranties, included in other accrued liabilities, was $259 million as of July 30, 2005, compared with

$239 million as of July 31, 2004. See Note 8 to the Consolidated Financial Statements. Our products are generally covered by a

warranty for periods ranging from 90 days to five years, and for some products we provide a limited lifetime warranty. We accrue for

warranty costs as part of our cost of sales based on associated material costs, technical support labor costs, and associated overhead.

Material cost is estimated based primarily upon historical trends in the volume of product returns within the warranty period and the

cost to repair or replace the equipment. Technical support labor cost is estimated based primarily upon historical trends in the rate of

customer cases and the cost to support the customer cases within the warranty period. Overhead cost is applied based on estimated

time to support warranty activities.

The provision for product warranties issued during fiscal 2005 and 2004 was $411 million and $333 million, respectively.

The increase in the provision for product warranties was due to a higher shipment volume of our products and an increase in warranty

claims. If we continue to experience an increase in warranty claims compared with our historical experience, or if the cost of servicing

warranty claims is greater than the expectations on which the accrual has been based, our gross margin could be adversely affected.

Investment Impairments

Our publicly traded equity securities are reflected in the Consolidated Balance Sheets at a fair value of $941 million as of July 30, 2005,

compared with $1.1 billion as of July 31, 2004. See Note 7 to the Consolidated Financial Statements. We recognize an impairment

charge when the decline in the fair value of our publicly traded equity securities below their cost basis are judged to be other-than-temporary.

The ultimate value realized on these equity securities, to the extent unhedged, is subject to market price volatility until they are sold.

We consider various factors in determining whether we should recognize an impairment charge, including the length of time and

extent to which the fair value has been less than our cost basis, the financial condition and near-term prospects of the investee, and

our intent and ability to hold the investment for a period of time sufficient to allow for any anticipated recovery in market value.

Our ongoing consideration of these factors could result in additional impairment charges in the future, which could adversely affect our

net income. Our impairment charges on investments in publicly held companies were $5 million and $412 million in fiscal 2005 and

2003, respectively. There were no impairment charges on investments in publicly held companies in fiscal 2004.

We also have investments in privately held companies, some of which are in the startup or development stages. As of July 30,

2005, our investments in privately held companies were $421 million, compared with $354 million as of July 31, 2004, and were

included in other assets. See Note 5 to the Consolidated Financial Statements. We monitor these investments for impairment and make

appropriate reductions in carrying values if we determine an impairment charge is required, based primarily on the financial condition and

near-term prospects of these companies. These investments are inherently risky because the markets for the technologies or products

these companies are developing are typically in the early stages and may never materialize. Our impairment charges on investments in

privately held companies were $39 million, $112 million, and $281 million during fiscal 2005, 2004, and 2003, respectively.

Management’s Discussion and Analysis of Financial Condition and Results of Operations