Chrysler 2007 Annual Report Download - page 257

Download and view the complete annual report

Please find page 257 of the 2007 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

|

|

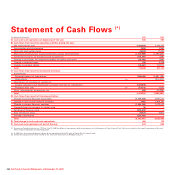

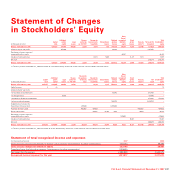

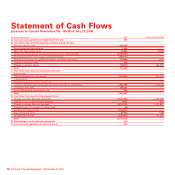

Fiat S.p.A. Financial Statements at December 31, 2007 - Notes to the Financial Statements256

by independent actuaries using the projected unit credit

method. The portion of net actuarial gains and losses at the end

of the previous reporting period that exceeds the greater of 10%

of the present value of the defined benefit obligation and 10%

of the fair value of the plan assets at that date is deferred and

recognised over the remaining working lives of the employees

(the “corridor method”); the portion of actuarial gains and

losses that does not exceed this threshold is deferred.

In the context of IFRS first-time adoption, the company elected

to recognise all cumulative actuarial gains and losses at

January 1, 2004 (date of first-time adoption of IFRS by the Fiat

Group), although it has adopted the corridor method for those

arising subsequently.

The expense related to the reversal of discounting pension

obligations for defined benefit plans are reported separately as

part of the Group’s financial expense.

The liability for obligations arising under defined benefit plans

and due on termination of the employment contract represents

the present value of the obligation adjusted by actuarial gains

and loses deferred as the result of applying the corridor

approach and by past service costs for employee service in

prior periods that will be recognised in future years.

Other long-term benefits

The accounting treatment of other long-term benefits is the

same as that for post-employment benefit plans except for the

fact that actuarial gains and losses and past service costs are

fully recognised in the income statement in the year in which

they arise and the corridor method is not applied.

Equity compensation plans

The company provides additional benefits to certain members

of senior management and to certain employees through equity

compensation plans. Under IFRS 2 -

Share-based Payment

,

these plans are a component of employee remuneration whose

cost is measured by the fair value of the stock options at the

grant date recognised in the income statement on a straight-

line basis from the grant date to the vesting date, with the

offsetting credit recognised directly in equity. Any subsequent

changes to fair value do not have any effect on the initial

measurement.

The company has applied the transitional provisions of IFRS 2

and as a result the Standard is applicable to all stock option

plans granted after November 7, 2002 but which had not yet

vested by January 1, 2005, the effective date of the Standard.

Detailed disclosures are also provided for plans granted before

that date.

The compensation component of the stock option plans based

on Fiat S.p.A. shares but regarding employees of other Group

companies is recognised as a capital contribution to the

subsidiaries for whom the employees beneficiaries of the stock

option plans work, in accordance with Interpretation IFRIC 11,

and as a result is recorded as an increase in the carrying

amount of the investment, with the offsetting credit being

recognized directly in equity.

Provisions

The company recognises provisions when it has a legal or

constructive obligation to third parties, when it is probable that

the settlement of the obligation will require the outflow of

resources and when a reliable estimate can be made for the

amount of the obligation.

Changes in estimates are recognised in the income statement

for the period in which the change occurs.

Treasury shares

Treasury shares are presented as a deduction from equity.

The original cost of treasury shares and the proceeds of any

subsequent sale are presented as movements in equity.

Dividends received and receivable

Dividends received and receivable from investments are

recognised in the income statement when the right to receive

the payment of this income is established and only if declared

from post-acquisition net income.