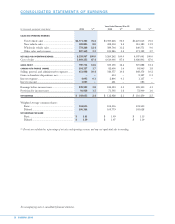

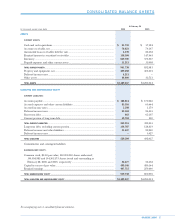

CarMax 2006 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2006 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

CARMAX 2006

45

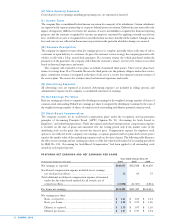

Reserve Accounts. The company is required to fund various reserve accounts established for the benefit

of the securitization investors. In the event that the cash generated by the securitized receivables in a given

period was insufficient to pay the interest, principal, and other required payments, the balances on deposit in

the reserve accounts would be used to pay those amounts. In general, each of the company’s securitizations

requires that an amount equal to a specified percentage of the original balance of the securitized receivables

be deposited in a reserve account on the closing date and that any excess cash generated by the receivables

be used to fund the reserve account to the extent necessary to maintain the required amount. If the amount

on deposit in the reserve account exceeds the required amount, the excess is released through the special

purpose entity to the company. In the public securitizations, the amount required to be on deposit in the

reserve account must equal or exceed a specified floor amount. The reserve account remains funded until

the investors are paid in full, at which time the remaining balance is released through the special purpose

entity to the company. The amount required to be maintained in the public securitization reserve accounts

may increase depending upon the performance of the securitized receivables. The amount on deposit in

reserve accounts was $29.0 million as of February 28, 2006, and $33.5 million as of February 28, 2005.

Required Excess Receivables. A majority of the securitizations require that the total value of the

securitized receivables exceed, by a specified amount, the principal amount owed to the investors. The

required excess receivables balance represents this specified amount. Any cash flows generated by the

required excess receivables are used, if needed, to make payments to the investors. Any remaining cash flows

from the required excess receivables are released through the special purpose entity to the company. The

unpaid principal balance related to the required excess receivables was $52.2 million as of February 28, 2006,

and $44.3 million as of February 28, 2005.

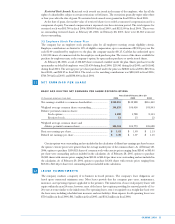

Key Assumptions Used in Measuring the Retained Interest and Sensitivity Analysis

The following table shows the key economic assumptions used in measuring the fair value of the retained

interest at February 28, 2006, and a sensitivity analysis showing the hypothetical effect on the retained

interest if there were unfavorable variations from the assumptions used. These sensitivity analyses are

hypothetical and should be used with caution. In this table, the effect of a variation in a particular

assumption on the fair value of the retained interest is calculated without changing any other assumption; in

actual circumstances, changes in one factor may result in changes in another, which might magnify or

counteract the sensitivities.

Impact on Fair Value of Impact on Fair Value of

(In millions) Assumptions Used 10% Adverse Change 20% Adverse Change

Prepayment rate........................................ 1.43% –1.50% $5.5 $10.8

Cumulative default rate............................ 1.40%–2.15% $4.7 $ 9.4

Annual discount rate ................................ 12.0% $2.3 $ 4.5

Prepayment Rate. The company uses the Absolute Prepayment Model or “ABS” to estimate prepayments.

This model assumes a rate of prepayment each month relative to the original number of receivables in a pool

of receivables. ABS further assumes that all the receivables are the same size and amortize at the same rate

and that each receivable in each month of its life will either be paid as scheduled or prepaid in full. For

example, in a pool of receivables originally containing 10,000 receivables, a 1% ABS rate means that 100

receivables prepay each month.

Cumulative Default Rate. The cumulative default rate, or “static pool” net losses, is calculated by dividing

the total projected credit losses of a pool of receivables by the original pool balance. Projected credit losses are

estimated using the losses experienced to date, the credit quality of the receivables, economic factors, and the

performance history of similar receivables.

Continuing Involvement with Securitized Receivables

The company continues to manage the automobile finance receivables that it securitizes. The company

receives servicing fees of approximately 1% of the outstanding principal balance of the securitized

receivables. The servicing fees specified in the securitization agreements adequately compensate the

company for servicing the securitized receivables. No servicing asset or liability has been recorded. The

company is at risk for the retained interest in the securitized receivables, and if the securitized receivables do

not perform as originally projected, the value of the retained interest would be impacted.