CarMax 2006 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2006 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

CARMAX 2006

41

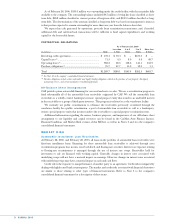

(F) Inventory

Inventory is comprised primarily of vehicles held for sale or undergoing reconditioning and is stated at the

lower of cost or market. Vehicle inventory cost is determined by specific identification. Parts and labor used to

recondition vehicles, as well as transportation and other incremental expenses associated with acquiring and

reconditioning vehicles, are included in inventory. Certain manufacturer incentives and rebates for new car

inventory, including holdbacks, are recognized as a reduction to new car inventory when CarMax purchases

the vehicles. Volume-based incentives are recognized as a reduction to cost of sales when achievement of

qualifying sales volumes is determined to be probable.

(G) Property and Equipment

Property and equipment is stated at cost less accumulated depreciation and amortization. Depreciation and

amortization are calculated using the straight-line method over the shorter of the asset’s estimated useful life or

the lease term, if applicable. Property held under capital lease is stated at the lower of the present value of the

future minimum lease payments at the inception of the lease or fair value. Amortization of capital lease assets is

computed on a straight-line basis over the shorter of the initial lease term or the estimated useful life of the asset

and is included in depreciation expense. Costs incurred during new store construction are capitalized as

construction in progress and reclassified to the appropriate fixed asset category when the store opens.

ESTIMATED USEFUL LIVES

Life

Buildings..................................................................... 25—40 years

Capital leases.............................................................. 10—20 years

Leasehold improvements........................................... 8—15 years

Furniture, fixtures, and equipment ........................... 5—15 years

The company reviews long-lived assets for impairment when circumstances indicate the carrying amount of

an asset may not be recoverable. Impairment is recognized when the sum of undiscounted estimated future

cash flows expected to result from the use of the asset is less than the carrying value.

(H) Other Assets

Computer Software Costs

External direct costs of materials and services used in the development of internal-use software and payroll and

payroll-related costs for employees directly involved in the development of internal-use software are capitalized.

Amounts capitalized are amortized on a straight-line basis over five years.

Goodwill and Intangible Assets

The company reviews goodwill and intangible assets for impairment annually or when circumstances indicate

the carrying amount may not be recoverable. No impairment of goodwill or intangible assets resulted from the

annual impairment tests in fiscal 2006 or fiscal 2005.

Restricted Cash Deposits

Included in other assets at February 28, 2006, and February 28, 2005, were restricted cash deposits of $17.7

million and $12.0 million, respectively, which were associated with certain insurance deductibles. Restricted

cash deposits were previously reported in Cash and Cash Equivalents.

(I) Defined Benefit Plan Obligations

Defined benefit retirement plan obligations are included in accrued expenses and other current liabilities on the

company’s consolidated balance sheets. The defined benefit retirement plan obligations are determined by

independent actuaries using a number of assumptions provided by the company. Key assumptions used in

measuring the plan obligations include the discount rate, the estimated rate of salary increases, and the

estimated future return on plan assets.

(J) Insurance Liabilities

Insurance liabilities are included in accrued expenses and other current liabilities on the company’s

consolidated balance sheets. The company uses a combination of insurance and self-insurance for a number of

risks including workers’ compensation, general liability, and employee-related health care benefits, a portion of

which is paid by associates. Estimated insurance liabilities are determined by considering historical claims

experience, demographic factors, and other actuarial assumptions.