Abercrombie & Fitch 2008 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2008 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

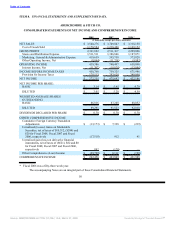

Table of Contents

In June 2006, the FASB issued FASB Interpretation No. 48, “Accounting for Uncertainty in Income

Taxes — an Interpretation of FASB Statement No. 109” (“FIN 48”). FIN 48 clarifies the accounting for

uncertainty in income taxes recognized in a Company’s financial statements in accordance with

SFAS No. 109. This interpretation prescribes a recognition threshold and measurement attribute for the

financial statement recognition and measurement of a tax position taken or expected to be taken in a tax

return. This interpretation also provides guidance on derecognition, classification, interest and penalties,

accounting in interim periods, disclosure and transition. The Company recognizes accrued interest and

penalties related to unrecognized tax benefits as a component of tax expense.

The provision for income taxes is based on the current estimate of the annual effective tax rate

adjusted to reflect the tax impact of items discrete to the quarter. The Company records tax expense or

benefit that does not relate to ordinary income in the current fiscal year discretely in the period in which it

occurs pursuant to the requirements of Accounting Principles Board (“APB”) Opinion No. 28, “Interim

Financial Reporting” and FASB Interpretation No. 18, “Accounting for Income Taxes in Interim

Periods — an Interpretation of APB Opinion No. 28” (“FIN 18”). Examples of such types of discrete

items include, but are not limited to, changes in estimates of the outcome of tax matters related to prior

years, provision-to-return adjustments, tax-exempt income and the settlement of tax audits.

Foreign Currency Translation

The majority of the Company’s international operations use local currencies as the functional

currency. In accordance with SFAS No. 52, “Foreign Currency Translation,” assets and liabilities

denominated in foreign currencies were translated into U.S. dollars (the reporting currency) at the

exchange rate prevailing at the Consolidated Balance Sheet date. Equity accounts denominated in foreign

currencies were translated into U.S. dollars at historical exchange rates. Revenues and expenses

denominated in foreign currencies were translated into U.S. dollars at the monthly average exchange rate

for the period. Gains and losses resulting from foreign currency transactions are included in the results of

operations; whereas, translation adjustments are reported as an element of other comprehensive income in

accordance with SFAS No. 130, “Reporting Comprehensive Income.”

Contingencies

In the normal course of business, the Company must make continuing estimates of potential future

legal obligations and liabilities, which requires the use of management’s judgment on the outcome of

various issues. Management may also use outside legal advice to assist in the estimating process.

However, the ultimate outcome of various legal issues could be different than management estimates, and

adjustments may be required.

Equity Compensation Expense

The Company’s equity compensation expense related to restricted stock units is estimated by

calculating the fair value of the restricted stock units granted as the market price of the underlying

Common Stock on the date of grant, adjusted for expected dividend payments during the vesting period.

The Company’s equity compensation expense related to stock options is estimated using the

Black-Scholes option-pricing model to determine the fair value of the stock option grants, which requires

the Company to estimate the expected term of the stock option grants and expected future stock price

volatility over the expected term. Estimates of the expected term, which represents the expected period of

time the Company believes the stock options will be outstanding, are based on historical information.

Estimates of the expected future stock price volatility are

46

Source: ABERCROMBIE & FITCH CO /DE/, 10-K, March 27, 2009 Powered by Morningstar® Document Research℠