Abercrombie & Fitch 2008 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2008 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

Table of Contents

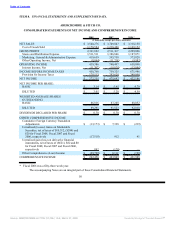

$14.0 million other-than-temporary impairment related to the Company’s trading ARS. See further

discussion in Note 5, “Cash and Equivalents and Investments” and Note 6, “Fair Value” of the Notes to

Consolidated Financial Statements located in “ITEM 8. FINANCIAL STATEMENTS AND

SUPPLEMENTARY DATA” of this Annual Report on Form 10-K.

Financial Accounting Standards Board (“FASB”) Staff Positions FAS 115-1 and FAS 124-1, “The

Meaning of Other-Than-Temporary Impairment and Its Application to Certain Investments,” states that an

investment is considered impaired when the fair value is less than cost. Significant judgment is required to

determine if impairment is other-than-temporary. The Company deemed the unrealized loss to be

temporary based primarily on the following: (1) the Company had the ability and intent to hold the

impaired securities to maturity; (2) the lack of deterioration in the financial performance, credit rating or

business prospects of the issuers; (3) the lack of evident factors that raise significant concerns about the

issuers’ ability to continue as a going concern; and (4) the lack of significant changes in the regulatory,

economic or technological environment of the issuers. If it becomes probable that the Company will not

receive 100% of the principal and interest as to any of the available-for-sale ARS or if events occur to

change any of the factors described above, the Company will be required to recognize an

other-than-temporary impairment charge against net income.

Assuming all other assumptions disclosed in Note 6, “Fair Value” of the Notes to Consolidated

Financial Statements, being equal, a 50 basis point increase in the market required rate of return will yield

an 11% decrease in fair value and a 50 basis point decrease in the market required rate of return will yield

an 11% increase in fair value.

Inventory Valuation

Inventories are principally valued at the lower of average cost or market utilizing the retail method.

The Company determines market value as the anticipated future selling price of the merchandise less a

normal margin. An initial markup is applied to inventory at cost in order to establish a cost-to-retail ratio.

Permanent markdowns, when taken, reduce both the retail and cost components of inventory on hand so

as to maintain the already established cost-to-retail relationship. At first and third fiscal quarter end, the

Company reduces inventory value by recording a valuation reserve that represents the estimated future

anticipated selling price decreases necessary to sell-through the current season inventory. At second and

fourth fiscal quarter end, the Company reduces inventory value by recording a valuation reserve that

represents the estimated future selling price decreases necessary to sell-through any remaining carryover

inventory from the season just passed. The valuation reserve was $9.1 million, $5.4 million and

$6.8 million at January 31, 2009, February 2, 2008 and February 3, 2007, respectively.

Additionally, as part of inventory valuation, an inventory shrink estimate is made each period that

reduces the value of inventory for lost or stolen items. The Company performs physical inventories

throughout the year and adjusts the shrink reserve accordingly. The shrink reserve was $10.8 million,

$11.5 million and $7.7 million at January 31, 2009, February 2, 2008 and February 3, 2007, respectively.

Inherent in the retail method calculation are certain significant judgments and estimates including,

among others, markdowns and shrinkage, which could significantly impact the ending inventory valuation

at cost, as well as the resulting gross margins. An increase or decrease in the inventory shrink estimate of

10% would not have a material impact on the Company’s results of operations.

44

Source: ABERCROMBIE & FITCH CO /DE/, 10-K, March 27, 2009 Powered by Morningstar® Document Research℠