Qantas 2005 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2005 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128

|

|

118

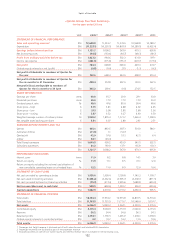

39. Impact of adopting Australian equivalents to

International Financial Reporting Standards continued

(f) OTHER

AASB 2 – Share Based Payments: as permitted by AASB 1 Qantas will not apply AASB 2 retrospectively to share based payments made

prior to 7 November 2002. It will therefore not apply to Entitlements issued under the Qantas Long-Term Executive Incentive Program

(QLTEIP).

AASB 3 – Business Combinations: as permitted by AASB 1 Qantas will apply this standard prospectively. Amortisation of goodwill on

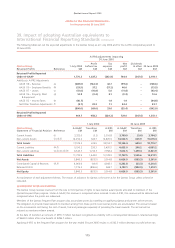

acquisition ceases on 1 July 2004. For the financial year ended 30 June 2005 goodwill amortised under A-GAAP was $28.5 million

(Qantas: $nil) inclusive of $13.4 million goodwill amortisation in Associate and Joint Venture investments.

AASB 121 – Foreign Exchange: as permitted by AASB 1, Qantas will reset the Foreign Currency Translation Reserve to zero on adoption

of this standard.

AASB 123 – Borrowing Costs: as permitted by AASB 123, Qantas will continue to capitalise borrowing costs associated with the

acquisition of qualifying assets such as aircraft and terminals.

AASB 127 – Consolidations: to comply with the intent of Interpretation 112, Qantas will consolidate the Qantas Deferred Share Plan Trust

(QDSPT). The QDSPT holds shares in Qantas on behalf of participants (which are Qantas employees), which will be classified as Treasury

Shares on consolidation.

AASB 136 – Impairment of Assets: under A-GAAP, Qantas used discounted cash flows to assess the value in-use of non-current assets.

Qantas tested all non-current assets for impairment on the transition to A-IFRS regardless of the existence of indicators of impairment.

No change in the carrying value of non-current assets was required on the adoption of AASB 136.

AASB 138 – Intangible Assets: intangible assets with an indefinite life, such as purchased airport landing slots, are not amortised but they

are tested for impairment each reporting period.

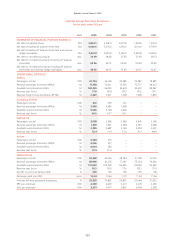

FINANCIAL INSTRUMENTS

The transition to AASB 139 – Financial Instruments: Recognition and Measurement and AASB 132 – Financial Instruments: Disclosure and

Presentation applies to Qantas effective from 1 July 2005. The Group has chosen not to restate comparative information with respect to

AASB 132 and AASB 139.

Qantas risk management practices will continue to be determined on an economic basis under A-IFRS. It is expected that this approach

will result in some transactions failing the AASB 139 hedge effectiveness criteria from time to time. If hedging transactions are deemed

ineffective under AASB 139, changes in the fair value of these transactions are to be recognised in the Statement of Financial Performance

as they occur, potentially causing earnings volatility.

Two areas of Qantas’ risk management practice that are likely to be significantly impacted by the requirements of AASB 139 are options

and fuel hedging.

OPTIONS

AASB 139 requires that the option value be separated into its intrinsic and non-intrinsic components and only the intrinsic value

is designated as a hedging instrument. The intrinsic value of the option must therefore be separated and designated as the hedge

instrument, with all other components of the option value (being primarily time value and volatility) being fair valued to the Statement

of Financial Performance over the life of the option.

Options form a significant part of Qantas’ hedging strategy for foreign exchange revenue, capital expenditure, fuel and interest rate

exposures. The changes in fair value of the non-intrinsic component of an option may cause periods of volatility in the Statement of

Financial Performance for Qantas.

AVIATION FUEL

AASB 139 permits hedge accounting for all financial exposures on a component basis. Non-financial assets or liabilities such as aviation

fuel, however, are treated differently under the Standard. Components of risk embedded in a commodity exposure are specifically

excluded from hedge accounting if hedged separately. Components of aviation fuel expense (for example crude oil) may not be hedged

independently and achieve hedge accounting under AASB 139. The total exposure (ie jet fuel) must be hedged in its entirety.

Qantas expects to achieve hedge accounting for aviation fuel risk management transactions in the majority of instances. However, given

the high volatility of fuel markets, the AASB 139 effectiveness test may not be met from time to time and on these occasions changes

in the fair value of hedging instruments may cause volatility in the Statement of Financial Performance.

Spirit of Australia

~Notes to the Financial Statements~

for the year ended 30 June 2005