HSBC 2004 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

69

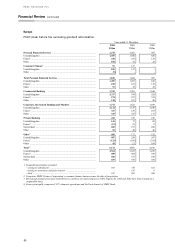

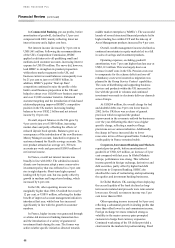

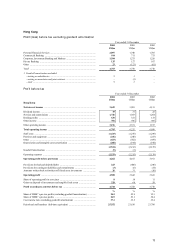

income earnings showed a strong year-on-year

growth reflecting a combination of tightening credit

spreads and strong investor demand for yield in the

low interest rate environment, which boosted sales of

corporate bonds. In line with a greater business focus

on risk management products, revenues from trading

increased, reflecting the benefit successful interest

rate positioning and continued growth in customer

mandates from corporate customers. Additional

growth in revenue resulted from a strong presence in

each of the euro vanilla and structured derivatives

markets.

Fees and commission income decreased by 6 per

cent. Difficult operating conditions in equity markets

resulted in lower commissions and new-issue fees,

but these were partly offset by higher fees from

merger and advisory business as greater focus was

given to HSBC’s core customer sectors and regions.

Fees from debt capital markets activities were also

strong. Generally, fees benefited from the high level

of activity in the primary markets, as customers

sought long-term financing at low interest rates.

Staff costs rose, with higher bonuses reflecting

increased profitability in specific product lines.

Restructuring and research costs of US$24 million

were also incurred to build and reshape HSBC’s

investment banking and equities businesses.

Premises and equipment expenses were lower as a

result of savings in rental payments from the London

office move to Canary Wharf.

Credit experience was generally satisfactory

although new specific provisions were higher,

mainly due to a single name in the engineering

sector which was extensively restructured in the

second half of the year. Corporate weakness in the

power generation sector was also dealt with through

raising additional specific provisions, although these

were partly offset by recoveries in the transport and

telecommunications sectors, as balance sheets were

strengthened.

Gains on investment disposals were lower than

in 2002, mainly due to a reduction in profits from the

disposal of venture capital investments in CCF.

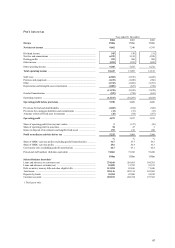

Against the background of a recovery from

recent lows in European stock markets, Private

Banking activities continued to grow during 2003.

Pre-tax profit, excluding goodwill amortisation,

increased by 48 per cent as a result of strong growth

in dealing income, lower costs and the non-

recurrence of contingencies and write downs

in 2002.

Net interest income was broadly in line with

2002. A 30 per cent increase in lending balances was

driven by clients seeking to maximise the overall

earnings potential of their investments by borrowing

to reinvest in higher returning securities. These

additional earnings were mostly offset by a decline

in yield on free funds as lower interest rates

prevailed throughout the year.

Net fees and commissions increased by 2 per

cent to US$556 million. The low interest rate

environment improved the attractiveness of

investment markets, particularly for sophisticated

investors with access to structured products which

offered potentially higher returns than from cash

deposits. Consequently, funds under management

increased by US$20 billion to US$91 billion, with a

move by clients away from liquid positions bringing

in some US$9 billion of new client funds. A strong

rise in discretionary mandates together with client

demand for structured products and HSBC Finance

Corporation’s commercial paper contributed to the

increase. Transaction and safe custody fees rose in

line with the growth in client funds while an

increased focus on product enrichment produced

strong growth in income from structured products. In

Germany, fee income was boosted by the placement

of two new property funds. However, income in

France was weaker as stock market activity

remained subdued.

Volatility in the major currencies resulted in

higher volumes of client transactions in the foreign

exchange markets, and combined with proprietary

equity gains in 2003, contributed to the 37 per cent

improvement in dealing profits to US$94 million.

Total operating expenses, before goodwill

amortisation, fell by 4 per cent to US$709 million.

This was achieved through cost savings realised

following the merger of three banks in Switzerland

in 2002 and lower property expenses.

Provisions for contingent liabilities and

commitments were lower than in 2002, which

included amounts provided for litigation. Amounts

written off fixed asset investments were lower than

in 2002 following a specific write down of a debt

security in 2002. Gains on disposal of investments

and tangible fixed assets increased by 22 per cent to

US$61 million, principally reflecting a gain on a

long-term private placement transaction.