HSBC 2004 Annual Report Download - page 163

Download and view the complete annual report

Please find page 163 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

161

In view of the high levels of personal

indebtedness in many of the world’ s leading

economies, guidelines for the restructuring of

customer facilities in the event of financial difficulty

have been reinforced.

In the US, the strength of the housing market

continued unabated, driven mainly by affordability.

Low interest rates, lower transaction costs and

increased availability of credit all fuelled the rise in

demand. However, recent rises in interest rates are

likely to affect growth adversely and add pressure to

some borrowers, particularly in certain overpriced

locations. The portfolios, however, remain

geographically diverse and are secured largely by

senior lien positions.

Although increased mortgage borrowing has

contributed to the record level of consumer debt,

levels have largely stabilised and are expected to

decline gradually, as incomes rise sufficiently to pay

down debt, notwithstanding higher interest rates.

Against this background, delinquency rates fell

across the majority of portfolios during 2004 and

trends in lending quality showed an improvement.

Personal lending in the UK also continued to

grow strongly, particularly in the mortgage market.

This secured portfolio, representing 55 per cent of

total lending to personal customers in the UK,

continued to suffer negligible delinquency and

losses. The unsecured portfolio also continued to

expand both through organic growth and with the

acquisition of Marks and Spencer Financial Services,

which added US$5.3 billion to the portfolio in

November 2004. Underwriting criteria were

regularly reviewed to ensure that they remained

appropriate in prevailing market conditions, which

have seen a steady rise in personal bankruptcies and

delinquencies over the course of the year.

With consumer spending rising in Hong Kong

and the levels of bankruptcies and unemployment

both falling, the improvement in the personal

portfolios, which first became evident during the

second half of 2003, continued throughout 2004.

With ongoing property price increases a feature of

2004, the most notable trend was the continued

reduction in the level of negative equity on mortgage

balances, which is now at modest levels.

Across the other geographical regions the

position remained relatively stable, although HSBC

continued to monitor carefully those portfolios that

have the greatest potential for future economic

stress. Delinquency and loss trends differed across

jurisdictions, reflecting these varied conditions.

Risk elements in the loan portfolio

The following disclosure of credit risk elements

reflects US accounting practice and classifications:

• loans accounted for on a non-accrual basis;

• accruing loans contractually past due 90 days or

more as to interest or principal; and

• troubled debt restructurings not included in the

above.

In accordance with UK accounting practice, a

number of operating companies suspend interest

rather than ceasing to accrue. This additional

category is also reported below, as are assets

acquired in exchange for advances.

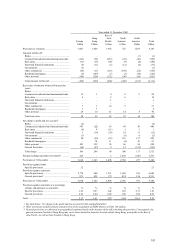

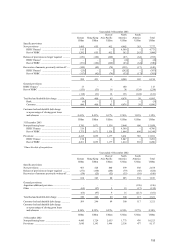

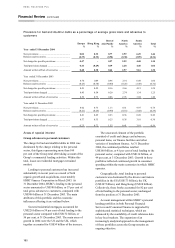

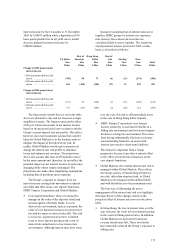

Non-performing loans and advances1

At 31 December

2004

US$m

2003

US$m

Banks ........................................ 25 24

Customers

– HSBC Finance ....................... 4,201 4,706

– Other HSBC............................ 9,058 10,344

13,259 15,050

Total non-performing loans

and advances........................... 13,284 15,074

Total provisions cover as a

percentage of non-performing

loans and advances ................. 95.5% 91.0%

1 Net of suspended interest.

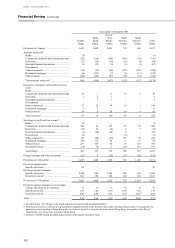

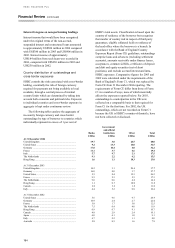

Non-performing customer loans1 and related

specific provisions outstanding by geographical

segment

2004 2003

Non-

performing

loans

Specific

provisions

Non-

performing

loans

Specific

provisions

US$m US$m US$m US$m

Europe ...... 6,065 4,036 5,701 3,554

Hong

Kong ...... 773 331 1,671 629

Rest of

Asia-

Pacific .... 1,180 791 1,538 981

North

America . 4,583 4,420 5,444 5,184

South

America 658 522 696 530

13,259 10,100 15,050 10,878

1 Net of suspended interest.

Total non-performing loans to customers decreased

by US$1,791 million during the year. At

31 December 2004, non-performing loans

represented 1.9 per cent of total lending compared