HSBC 2004 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

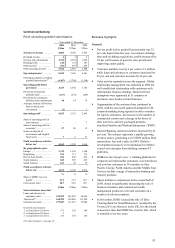

49

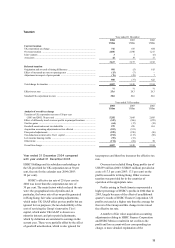

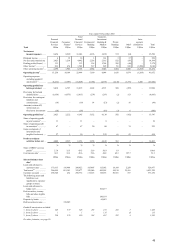

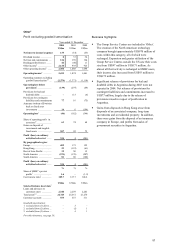

Consumer Finance

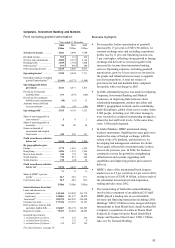

Profit excluding goodwill amortisation Business highlights

Year ended

31 December

2004420035

US$m US$m

Net interest income ................................. 11,176 8,289

Dividend income ....................................... 912

Net fees and commissions ......................... 1,893 1,219

Other income ............................................ 1,004 674

Other operating income ............................. 2,906 1,905

Operating income .................................... 14,082 10,194

Operating expenses excluding goodwill

amortisation1 ......................................... (4,997) (3,397)

Operating profit before provisions1 ....... 9,085 6,797

Provisions for bad and doubtful debts ....... (5,457) (4,575)

Operating profit1 ..................................... 3,628 2,222

Gains on disposal of investments and

tangible fixed assets .............................. 39 3

Profit on ordinary activities

before tax1 ............................................ 3,667 2,225

By geographical region:

Europe ....................................................... 91 157

North America .......................................... 3,576 2,068

Profit on ordinary activities

before tax1 ............................................ 3,667 2,225

%%

Share of HSBC’ s pre-tax profits1 .............. 18.9 15.5

Cost:income ratio1 ..................................... 35.5 33.3

US$m US$m

Selected balance sheet data7

Loans and advances to customers (net) ..... 137,100 116,409

Total assets8 ............................................... 163,420 145,383

Debt securities in issue .............................. 115,668 110,905

Goodwill amortisation:

1excluded from (1) above ........................ 519 379

For other footnotes, see page 59.

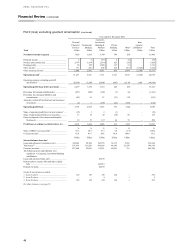

• Consumer Finance reported a pre-tax profit, before

goodwill amortisation, of US$3,667 million, of

which US$1,126 million was an additional quarters’

contribution. Excluding this, and at constrant

exchange rates, pre-tax profit grew by 13 per cent to

US$2,541 million.

• In September 2004, HSBC extended its brand across

a number of its Consumer Finance businesses in the

US. In early 2005, the rebranding efforts will

continue with the rebranding of HSBC Finance

Corporation’ s vehicle finance and credit cards

businesses. The branch based Consumer Finance

business will retain the HFC and Beneficial brands,

accompanied by the endorsement signature,

‘Member HSBC Group’ .

• In December 2004, Household International, Inc.

merged with its wholly owned subsidiary and

changed its name to HSBC Finance Corporation. The

name change was a continuation of the rebranding of

the Household businesses to the HSBC brand. These

actions were taken to establish a single brand in

North America to create a stronger platform to

advance growth across all HSBC business lines.

• Strong improvement was seen in credit quality,

driven by the economic upturn, improved origination

quality, growth in the relative proportion of secured

receivables, improved collection activity, and the

effect on product mix of HSBC Finance

Corporation’ s move into prime and near-prime

markets. Improvements were seen across most

products and in a number of key indicators. The rate

of improvement began to slow in the second half of

the year reflecting the maturing of the portfolio, less

robust employment growth and rising energy prices.

• Loans and advances to customers grew by 18 per

cent to US$137.1 billion, mainly driven by strong

organic loan growth in mortgages and vehicle

finance.

• Expansion into prime and near-prime markets in the

US contributed to strong growth in customer loan

balances, particularly in the mortgage business.

Residential mortgage balances increased from

US$46.1 billion at the end of 2003 to

US$60.8 billion by the end of 2004.