HSBC 2004 Annual Report Download - page 331

Download and view the complete annual report

Please find page 331 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

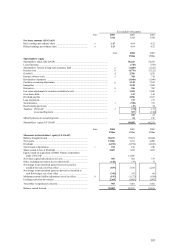

329

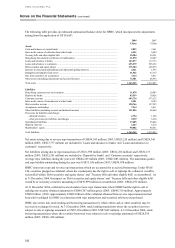

– Each holder of interests in the transferee (i.e. holder of issued notes) has the right to pledge or exchange

their beneficial interests, and no condition constrains this right and provides more than a trivial benefit to the

transferor.

– The transferor does not maintain effective control over the assets through either an agreement that obligates

the transferor to repurchase or to redeem them before their maturity or through the ability to unilaterally

cause the holder to return specific assets, other than through a clean-up call.

– If these conditions are not met the securitised assets should continue to be consolidated.

• Where HSBC retains an interest in the securitised assets, such as a servicing right or the right to residual cash

flows from the special purpose entity, HSBC recognises this interest at fair value on sale of the assets.

• There are no provisions for linked presentation of securitised assets and the related finance.

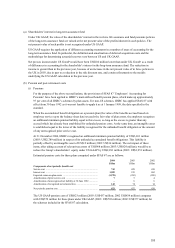

Consolidation of Variable Interest Entities

UK GAAP

• In accordance with FRS 5, entities that fall within the definition of quasi-subsidiaries are consolidated. A quasi-

subsidiary is defined as an entity that is directly or indirectly controlled by HSBC and gives rise to benefits that

are in substance no different from those that would arise were the vehicle a subsidiary. FRS 5 states that this will

arise where HSBC receives the benefits of the net assets of the entity and is exposed to the risks inherent in those

net assets.

US GAAP

• FASB Interpretation 46 (revised December 2003) ‘Consolidation of Variable Interest Entities’ (‘FIN 46R’ ),

which became fully effective for HSBC from 1 January 2004, requires consolidation of Variable Interest Entities

(‘VIEs’ ) in which HSBC is the primary beneficiary and disclosures in respect of all other VIEs in which it has a

significant variable interest.

• A VIE is an entity in which equity investors do not hold an investment with the characteristics of a controlling

financial interest or do not have sufficient equity at risk for the entity to finance its activities. HSBC is the

primary beneficiary of a VIE if its variable interests absorb a majority of the entity’ s expected losses. Variable

interests are contractual, ownership or other pecuniary interests in an entity that change with changes in the fair

value of an entity’ s net assets exclusive of variable interests. If no party absorbs a majority of the entity’ s

expected losses, HSBC consolidates the VIE if it receives a majority of the expected residual returns of the

entity.

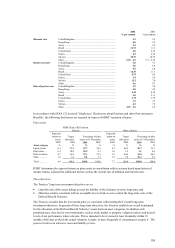

Restructuring provisions

UK GAAP

• In accordance with FRS 12 ‘Provisions, contingent liabilities and contingent assets’ , provisions are made for any

direct costs and net future operating losses arising from a business that management is committed to restructure,

sell or terminate, has a detailed formal plan to exit, and has raised a valid expectation of carrying out that plan.

• In accordance with SSAP 24 ‘Accounting for pension costs’ , the cost of additional pension benefits that accrue

to employees made redundant are spread over the remaining service lives of existing employees in line with

other actuarial adjustments.

US GAAP

• SFAS 146 ‘Accounting for Costs Associated with Exit or Disposal Activities’ , requires that the fair value of a

liability for a cost associated with an exit or disposal activity be recognised when the liability is incurred.

Accordingly, provisions are recognised upon the implementation of the restructuring plan.

• SFAS 88 ‘Employers’ Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for

Termination Benefits’ requires that the present value of expected employee termination benefits payable

pursuant to a contractual or legal obligation be recognised when it is probable that employees will be entitled to

benefits and the amounts can be reasonably estimated. Generally, this would be when management commits to a

plan of termination that identifies the number of employees to be terminated, their job classification or functions