HSBC 2004 Annual Report Download - page 351

Download and view the complete annual report

Please find page 351 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

349

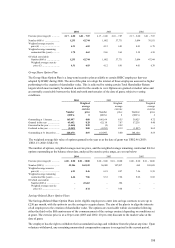

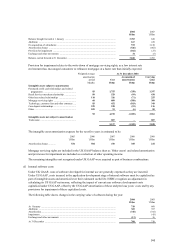

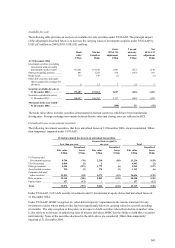

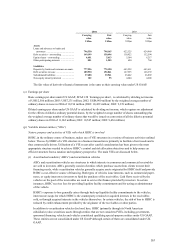

allowances) totalling US$115 million (2003: US$231 million), of which, US$7 million (2003: US$49 million)

expire within two to five years and US$108 million (2003: US$182 million) expire in 5 years or more.

(m) Loans and advances

SFAS 114 ‘Accounting by creditors for impairment of a loan’ was amended by SFAS 118 ‘Accounting by

creditors for impairment of a loan – income recognition and disclosures’ . SFAS 114 addresses accounting by

creditors for impairment of a loan by specifying how allowances for credit losses for certain loans should be

determined. A loan is impaired when it is probable that the creditor will be unable to collect all amounts in

accordance with the contractual terms of the loan agreement. Impairment is measured based on the present value

of expected future cash flows discounted at the loan’ s effective rate or, as an expedient, at the fair value of the

loan’ s collateral. Leases, smaller-balance homogeneous loans and debt securities are excluded from the scope of

SFAS 114.

At 31 December 2004, HSBC estimated that the difference between the carrying value of its loan portfolio on the

basis of SFAS 114 and its value in HSBC’ s UK GAAP financial statements was such that no adjustment to net

income or shareholders’ equity was required.

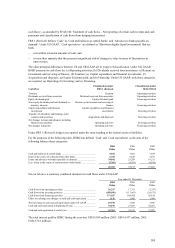

Impaired loans are those reported by HSBC as non-performing. The value of such loans at 31 December 2004

was US$13,284 million (2003: US$15,074 million). Of this total, loans which were included within the scope of

SFAS 114 and for which a provision has been established amounted to US$6,780 million (2003: US$8,810

million). The impairment reserve in respect of these loans estimated in accordance with the provisions of

SFAS 114 was US$3,981 million (2003: US$4,709 million). During the year ended 31 December 2004, impaired

loans, including those excluded from the scope of SFAS 114, averaged US$13,739 million (2003: US$12,215

million) and interest income recognised on these loans was US$184 million (2003: US$230 million; 2002:

US$258 million).

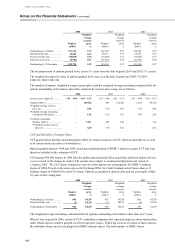

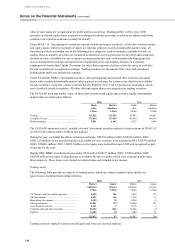

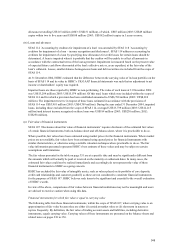

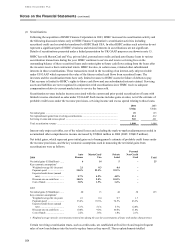

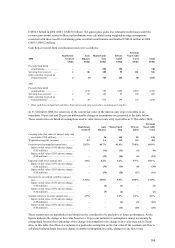

(n) Fair value of financial instruments

SFAS 107 ‘Disclosures about fair value of financial instruments’ requires disclosure of the estimated fair values

of certain financial instruments, both on-balance-sheet and off-balance-sheet, where it is practicable to do so.

Where possible, fair values have been estimated using market prices for the financial instruments. Where market

prices are not available, fair values have been estimated using quoted prices for financial instruments with

similar characteristics, or otherwise using a suitable valuation technique where practicable to do so. The fair

value information presented represents HSBC’ s best estimate of these values and may be subject to certain

assumptions and limitations.

The fair values presented in the table on page 351 are at a specific date and may be significantly different from

the amounts which will actually be paid or received on the maturity or settlement dates. In many cases, the

estimated fair values could not be realised immediately and accordingly do not represent the value of these

financial instruments to HSBC as a going concern.

HSBC has excluded the fair value of intangible assets, such as values placed on its portfolio of core deposits,

credit card relationships and customer goodwill, as these are not considered to constitute financial instruments

for the purposes of SFAS 107. HSBC believes such items to be significant and essential to the overall evaluation

of HSBC’ s worth.

In view of the above, comparisons of fair values between financial institutions may not be meaningful and users

are advised to exercise caution when using this data.

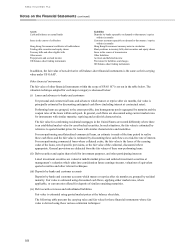

Financial instruments for which fair value is equal to carrying value

The following table lists those financial instruments, within the scope of SFAS 107, where carrying value is an

approximation of fair value because they are either (i) carried at market value or (ii) short term in nature or

reprice frequently. By definition, the fair value of trading account assets and liabilities, including derivative

instruments, equals carrying value. Carrying values of these instruments are presented on the balance sheets and

related notes on pages 238 to 356.