Xcel Energy 2005 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2005 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

12. DERIVATIVE INSTRUMENTS

In the normal course of business, Xcel Energy and its subsidiaries are exposed to a variety of market risks. Market risk is the potential loss

that may occur as a result of changes in the market or fair value of a particular instrument or commodity. Xcel Energy and its subsidiaries

utilize, in accordance with approved risk management policies, a variety of derivative instruments to mitigate market risk and to enhance our

operations. The use of these derivative instruments is discussed in further detail below.

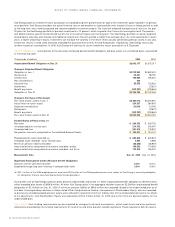

Utility Commodity Price Risk

Xcel Energy’s utility subsidiaries are exposed to commodity price risk in their electric and natural gas

operations. Commodity price risk is managed by entering into both long- and short-term physical purchase and sales contracts for electric

capacity, energy and other energy-related products, and for various fuels used for generation of electricity and in the natural gas utility operations.

Commodity risk also is managed through the use of financial derivative instruments. Xcel Energy’s utility subsidiaries utilize these derivative

instruments to reduce the volatility in the cost of commodities acquired on behalf of our retail customers even though regulatory jurisdiction

may provide for a dollar-for-dollar recovery of actual costs. In these instances, the use of derivative instruments is done consistently with

the state regulatory cost-recovery mechanism. Xcel Energy’s risk-management policy allows it to manage market price risk within each

rate-regulated operation to the extent such exposure exists.

Short-Term Wholesale and Commodity Trading Risk

Xcel Energy’s utility subsidiaries conduct various short-term wholesale and

commodity trading activities, including the purchase and sale of electric capacity, energy and other energy-related instruments. These

activities are primarily focused on specific regions where market knowledge and experience have been obtained and are generally less

than one year in length. Xcel Energy’s risk-management policy allows management to conduct the marketing activity within approved

guidelines and limitations as approved by our risk-management committee, which is made up of management personnel not directly

involved in the activities governed by this policy.

Interest Rate Risk

Xcel Energy and its subsidiaries are subject to the risk of fluctuating interest rates in the normal course of business.

Xcel Energy’s risk-management policy allows interest rate risk to be managed through the use of fixed-rate debt, floating-rate debt and

interest-rate derivatives such as swaps, caps, collars and put or call options.

Foreign Currency Exchange Risk

Due to the discontinuance of NRG and Xcel Energy International’s operations in 2003, as discussed in

Note 2 to the Consolidated Financial Statements, Xcel Energy no longer has material foreign currency exchange risk.

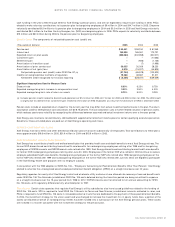

TYPES OF AND ACCOUNTING FOR DERIVATIVE INSTRUMENTS

Xcel Energy and its subsidiaries use a number of different derivative instruments in connection with its utility commodity price, interest rate,

short-term wholesale and commodity trading activities, including forward contracts, futures, swaps and options. All derivative instruments not

qualifying for the normal purchases and normal sales exception, as defined by SFAS No. 133, as amended, are recorded at fair value. The

classification of the fair value for these derivative instruments is dependent on the designation of a qualifying hedging relationship. The fair

values of derivative instruments not designated in a qualifying hedging relationship are reflected in current earnings. This includes certain

instruments used to mitigate market risk for the utility operations and all instruments related to the commodity trading operations. The

designation of a cash flow hedge permits the classification of fair value to be recorded within Other Comprehensive Income, to the extent

effective. The designation of a fair value hedge permits a derivative instrument’s gains or losses to offset the related results of the hedged

item in the Consolidated Statements of Operations, to the extent effective.

SFAS No. 133, as amended, requires that the hedging relationship be highly effective and that a company formally designate a hedging

relationship to apply hedge accounting. Xcel Energy and its subsidiaries formally document hedging relationships, including, among other

factors, the identification of the hedging instrument and the hedged transaction, as well as the risk-management objectives and strategies

for undertaking the hedged transaction. Xcel Energy and its subsidiaries also formally assess, both at inception and on an ongoing basis,

if required, whether the derivative instruments being used are highly effective in offsetting changes in either the fair value or cash flows of

the hedged items.

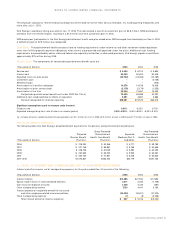

Gains or losses on hedging transactions for the sales of energy or energy-related products are primarily recorded as a component of revenue;

hedging transactions for fuel used in energy generation are recorded as a component of fuel costs; hedging transactions for natural gas

purchased for resale are recorded as a component of natural gas costs; and interest rate hedging transactions are recorded as a component

of interest expense. Certain utility subsidiaries are allowed to recover in electric or natural gas rates the costs of certain financial instruments

purchased to reduce commodity cost volatility.

Qualifying hedging relationships are designated as either a hedge of a forecasted transaction or future cash flow (cash flow hedge), or a

hedge of a recognized asset, liability or firm commitment (fair value hedge). The types of qualifying hedging transactions that Xcel Energy

and its subsidiaries are currently engaged in are discussed below.

CASH FLOW HEDGES

The effective portion of the change in the fair value of a derivative instrument qualifying as a cash flow hedge is recognized in Other

Comprehensive Income, and reclassified into earnings in the same period or periods during which the hedged transaction affects earnings.

The ineffective portion of a derivative instrument’s change in fair value is recognized in current earnings.

Commodity Cash Flow Hedges

Xcel Energy’s utility subsidiaries enter into derivative instruments to manage variability of future cash flows

from changes in commodity prices. These derivative instruments are designated as cash flow hedges for accounting purposes. At Dec. 31, 2005,

Xcel Energy had various commodity-related contracts classified as cash flow hedges extending through 2009. The fair value of these cash

flow hedges is recorded in either Other Comprehensive Income or deferred as a regulatory asset or liability. This classification is based on

64 XCEL ENERGY 2005 ANNUAL REPORT

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS