Vodafone 2000 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2000 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

Vodafone AirTouch Plc Annual Report & Accounts for the year ended 31 March 2000

12

Financial Review continued

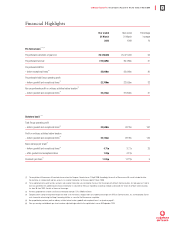

Equity shareholders’ funds

Total equity shareholders’ funds at 31 March 2000 had increased to

£140,833m, compared with £815m at 31 March 1999. The increase

includes the issue of new share capital of £140,037m, primarily

in relation to the merger with AirTouch and the acquisition of

Mannesmann, unvested option consideration of £1,165m in respect

of the merger with AirTouch, a profit for the financial year of £487m

(after goodwill amortisation of £1,712m), offset by dividends paid and

proposed of £620m and an adverse currency translation adjustment in

reserves of £1,130m.

Cash flows and net borrowings

Cash generated from operating activities increased by £1,465m to

£2,510m due primarily to the growth in the Group’s operations and the

inclusion of the operating cash flows of the former AirTouch businesses

following the merger. Other significant cash inflows included £236m in

respect of dividends from joint ventures and associated undertakings,

£1,028m from the disposal of fixed asset investments and loan

repayments, and proceeds of £362m on the exercise of share options

by employees.

The principal cash outflows during the period related to cash

consideration for investment purchases of £4,801m, net capital

expenditure of £1,739m and net interest and other finance charges

of £406m, including dividends paid to minority interests of £93m.

Net capital expenditure of £1,739m is after deducting £279m of

cash receipts in relation to the sub-leasing of certain US

communications towers.

An analysis of net payments made in respect of investments is set out

in the table below.

Net cash outflow – investments £m

AirTouch Communications, Inc. 3,534

CommNet Cellular Inc. 459

J-Phone Group 342

Omnitel 112

Other 354

–––––––––

4,801

–––––––––

As a result of these cash flows, and acquired indebtedness of

£2,133m, net debt at the year end was £6,643m, an increase of

£5,135m from 31 March 1999. A maturity analysis of net debt at

31 March 2000 is shown below.

Net debt – maturity profile

Analysed by repayment year: £m

Less than 1 year 605

Between 1-2 years 481

Between 2-5 years 1,681

More than 5 years 3,876

–––––––––

6,643

–––––––––

Debt repayable within one year in the above analysis is net of cash and

other liquid investments amounting to £189m at 31 March 2000.

£700m of the gross debt maturing within one year was commercial

paper, issued under the Group’s US$15 billion commercial paper

programme. This programme is supported by bank facilities with more

than one year to maturity.

The Group launched a 1.5 billion eurobond issue in October 1999

and a three tranche US$5.25 billion bond in February 2000, with

maturities of between 5 and 30 years, the proceeds from which were

used to refinance short term borrowings.

Future investment

The Group intends to acquire spectrum to operate 3G services.

In April 2000, the largest UK licence available to existing operators

was purchased for £5.964 billion. In 2000/2001, 3G licences are

anticipated to be awarded in Germany, Italy, the Netherlands and

Sweden. The cost of obtaining these licences could be significant.

In 2000/2001, the Group expects to spend in the order of £4 billion on

capital expenditure, excluding 3G licences. The majority of this will be

expended in the EMEA region where capital expenditure will total

approximately £2.5 billion, the increase being largely due to the

addition of the Mannesmann telecommunications’ subsidiaries.

Expenditure in the UK will be less than £1 billion and will total

approximately £0.3 billion in the United States & Asia Pacific region,

the latter being lower than the current year due to the creation of the

Verizon Wireless joint venture in April 2000. It is anticipated that capital

expenditure in 2001/2002 will be slightly higher as 3G networks are

rolled out.

Treasury management and policy

The principal financial risks arising from the Group’s activities are

funding risk, interest rate risk, currency risk and counterparty risk.

The Group’s treasury function provides a centralised service for the

management and monitoring of these risks for all of the Group’s

operations.

Treasury operations are conducted with a framework of policies

and guidelines authorised and reviewed annually by the Board.

The Group accounting function provides regular update reports of

treasury activity to the Board. The Group uses a number of derivative

instruments which are transacted, for risk management purposes only,

by specialist treasury personnel.

There has been no change during the year, or since the year end, to

the types of financial risks faced by the Group or the Group’s approach

to the management of those risks.

Funding and liquidity

The Group has a strong financial position demonstrated by credit

ratings of P-1/F1/A2 short term and A/A/A– long term from Moody’s,

Fitch IBCA Duff & Phelps and Standard and Poor’s, respectively, which

reflect the amended ratings of the Group following the acquisition of

Mannesmann AG and a UK 3G licence. These ratings enable the Group

to access a wide range of debt finance including bonds, commercial

paper and committed bank facilities.