Virgin Media 2014 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2014 Virgin Media annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75

|

|

70

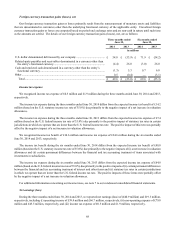

Capitalization

Liberty Global seeks to maintain its debt at levels that provide for attractive equity returns without assuming undue risk. In

this regard, Liberty Global generally seeks to cause our company to maintain our debt at levels that result in a consolidated debt

balance (measured using debt figures at swapped foreign currency exchange rates, consistent with the covenant calculation

requirements of our debt agreements) that is between four and five times our consolidated operating cash flow, although it should

be noted that the timing of financing transactions may temporarily cause this ratio to exceed the targeted range.

As further discussed in note 3 to our condensed consolidated financial statements, we use derivative instruments to mitigate

foreign currency and interest rate risk associated with our debt instruments.

Our ability to service or refinance our debt and to maintain compliance with the leverage covenants in our credit agreements

and indentures is dependent primarily on our ability to maintain or increase the operating cash flow of our operating subsidiaries

and to achieve adequate returns on our property and equipment additions and acquisitions. In addition, our ability to obtain

additional debt financing is limited by the leverage covenants contained in the various debt instruments of our subsidiaries. In

this regard, if our operating cash flow were to decline, we could be required to repay or limit our borrowings under the VM Credit

Facility in order to maintain compliance with applicable covenants. No assurance can be given that we would have sufficient

sources of liquidity, or that any external funding would be available on favorable terms, or at all, to fund any such required

repayment. We do not anticipate any instances of non-compliance with respect to any of our subsidiaries’ debt covenants that

would have a material adverse impact on our liquidity during the next 12 months.

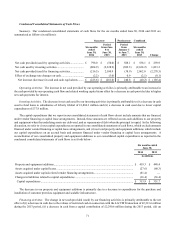

At June 30, 2014, our outstanding consolidated debt and capital lease obligations aggregated £8,221.8 million, including

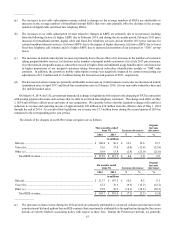

£172.0 million that is classified as current in our condensed consolidated balance sheet and £7,963.0 million that is not due until

2019 or thereafter.

Notwithstanding our negative working capital position at June 30, 2014, we believe that we have sufficient resources to repay

or refinance the current portion of our debt and capital lease obligations and to fund our foreseeable liquidity requirements during

the next 12 months. However, as our maturing debt grows in later years, we anticipate that we will seek to refinance or otherwise

extend our debt maturities. No assurance can be given that we will be able to complete these refinancing transactions or otherwise

extend our debt maturities. In this regard, it is not possible to predict how political and economic conditions, sovereign debt

concerns or any adverse regulatory developments could impact the credit markets we access and, accordingly, our future liquidity

and financial position. However, (i) the financial failure of any of our counterparties could (a) reduce amounts available under

committed credit facilities and (b) adversely impact our ability to access cash deposited with any failed financial institution and

(ii) tightening of the credit markets could adversely impact our ability to access debt financing on favorable terms, or at all. In

addition, sustained or increased competition, particularly in combination with adverse economic or regulatory developments, could

have an unfavorable impact on our cash flows and liquidity.

With the exception of the VM Convertible Notes, all of our consolidated debt and capital lease obligations at June 30, 2014

have been borrowed or incurred by our subsidiaries. For additional information concerning our debt and capital lease obligations,

see note 6 to our condensed consolidated financial statements.