US Cellular 2011 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2011 US Cellular annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

UNITED STATES CELLULAR CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND RECENT ACCOUNTING

PRONOUNCEMENTS (Continued)

Cash and Cash Equivalents

Cash and cash equivalents include cash and short-term, highly liquid investments with original maturities

of three months or less.

Short-Term and Long-Term Investments

As of December 31, 2011 and 2010, U.S. Cellular had $127.0 million and $146.6 million in Short-term

investments and $30.1 million and $46.0 million in Long-term investments, respectively. Short-term and

Long-term investments consist of certificates of deposit (short-term only), U.S. treasuries and corporate

notes, all of which are designated as held-to-maturity investments, and are recorded at amortized cost in

the Consolidated Balance Sheet. The corporate notes are guaranteed by the Federal Deposit Insurance

Corporation. For these investments, U.S. Cellular’s objective is to earn a higher rate of return on funds

that are not anticipated to be required to meet liquidity needs in the near term, while maintaining a low

level of investment risk. See Note 4—Fair Value Measurements for additional details on Short-term and

Long-term investments.

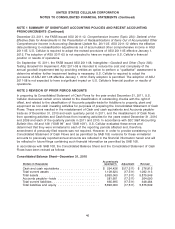

Accounts Receivable and Allowance for Doubtful Accounts

Accounts receivable primarily consist of amounts owed by customers for wireless services and

equipment sales, by agents for sales of equipment to them and by other wireless carriers whose

customers have used U.S. Cellular’s wireless systems.

The allowance for doubtful accounts is the best estimate of the amount of probable credit losses related

to existing accounts receivable. The allowance is estimated based on historical experience and other

factors that could affect collectability. Accounts receivable balances are reviewed on either an aggregate

or individual basis for collectability depending on the type of receivable. When it is probable that an

account balance will not be collected, the account balance is charged against the allowance for doubtful

accounts. U.S. Cellular does not have any off-balance sheet credit exposure related to its customers.

The changes in the allowance for doubtful accounts during the years ended December 31, 2011, 2010

and 2009 were as follows:

(Dollars in thousands) 2011 2010 2009

Beginning balance ................................ $25,816 $ 26,624 $ 8,372

Additions, net of recoveries ........................ 62,157 76,292 107,991

Deductions .................................... (64,436) (77,100) (89,739)

Ending balance .................................. $23,537 $ 25,816 $ 26,624

Inventory

Inventory primarily consists of wireless devices stated at the lower of cost or market, with cost

determined using the first-in, first-out method and market determined by replacement costs or estimated

net realizable value.

Fair Value Measurements

Under the provisions of GAAP, fair value is a market-based measurement and not an entity-specific

measurement, based on an exchange transaction in which the entity sells an asset or transfers a liability

(exit price). The provisions also establish a fair value hierarchy that contains three levels for inputs used

in fair value measurements. Level 1 inputs include quoted market prices for identical assets or liabilities

37