UPS 2009 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2009 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

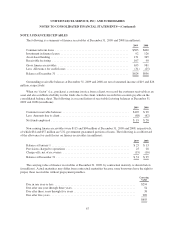

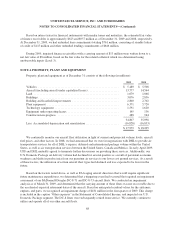

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

depending on the nature of the hedge, changes in its fair value that are considered to be effective, as defined,

either offset the change in fair value of the hedged assets, liabilities, or firm commitments through income, or are

recorded in AOCI until the hedged item is recorded in income. Any portion of a change in a derivative’s fair

value that is considered to be ineffective, or is excluded from the measurement of effectiveness, is recorded

immediately in income.

Recently Adopted Accounting Standards

Provisions within the following accounting standards were adopted during the years covered by these

financial statements:

Financial Instruments: The Financial Accounting Standards Board (“FASB”) issued guidance in February

2007 that gives entities the option to measure eligible financial assets, financial liabilities and firm

commitments at fair value (i.e., the fair value option), on an instrument-by-instrument basis, that are

otherwise not accounted for at fair value under other accounting standards. The election to use the fair value

option is available at specified election dates, such as when an entity first recognizes a financial asset or

financial liability or upon entering into a firm commitment. Subsequent changes in fair value must be

recorded in earnings. Additionally, this guidance allowed for a one-time election for existing positions upon

adoption, with the transition adjustment recorded to beginning retained earnings. We adopted this standard

on January 1, 2008, and elected to apply the fair value option to our investment in certain investment

partnerships that were previously accounted for under the equity method. Accordingly, we recorded a $16

million reduction to retained earnings as of January 1, 2008. These investments are reported in “other

non-current assets” on the consolidated balance sheet.

Compensation-Retirement Benefits: We previously utilized the early measurement date option available in

accounting for our pension and postretirement medical benefit plans, and we measured the funded status of

our plans as of September 30 each year. Under guidance issued by the FASB,we were required to use a

December 31 measurement date for all of our pension and postretirement benefit plans beginning in 2008.

As a result of this change in measurement date, we recorded a cumulative effect after-tax $44 million

reduction to retained earnings as of January 1, 2008.

Beginning in 2009, new guidance was adopted that required disclosures about plan assets of a defined

benefit pension or other postretirement plan, investment policies and strategies, major categories of plan

assets, inputs and valuation techniques used to measure the fair value of plan assets and significant

concentrations of risk within plan assets. These disclosures are provided in Note 5.

Income Taxes: Effective beginning in 2007, guidance issued by the FASB required that we determine

whether a tax position is more likely than not to be sustained upon examination, including resolution of any

related appeals or litigation processes, based on the technical merits of the position. Once it is determined

that a position meets this recognition threshold, the position is measured to determine the amount of benefit

to be recognized in the financial statements. We adopted this new standard on January 1, 2007, and the

cumulative effect of adopting this standard was to recognize a $104 million decrease in the January 1, 2007

balance of retained earnings.

Fair Value Measurements and Disclosures: The FASB issued guidance on fair value measurements that

took effect on January 1, 2008 and are presented in Notes 2, 3, 4, 5, and 14. On January 1, 2009, we

implemented the previously deferred provisions of this guidance for nonfinancial assets and liabilities

recorded at fair value. The accounting requirements for determining fair value when the volume and level of

activity for an asset or liability have significantly decreased, and for identifying transactions that are not

orderly, contained the FASB’s guidance were adopted on April 1, 2009, but had an immaterial impact on

our financial statements.

60