UPS 2009 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2009 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

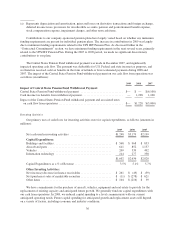

|

|

pension assets, and certain other investments. Fair values are based on listed market prices, when such prices are

available. To the extent that listed market prices are not available, fair value is determined based on other

relevant factors, including dealer price quotations. Certain financial instruments, including over-the-counter

derivative instruments, are valued using pricing models that consider, among other factors, contractual and

market prices, correlations, time value, credit spreads, and yield curve volatility factors. Changes in the fixed

income, equity, foreign exchange, and commodity markets will impact our estimates of fair value in the future,

potentially affecting our results of operations. A quantitative sensitivity analysis of our exposure to changes in

commodity prices, foreign currency exchange rates, interest rates, and equity prices is presented in the “Market

Risk” section of this report.

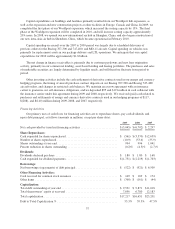

Pension and Postretirement Medical Benefits

As discussed in Note 5 to our consolidated financial statements, we maintain several single-employer

defined benefit and postretirement benefit plans. Our pension and other postretirement benefit costs are

calculated using various actuarial assumptions and methodologies. These assumptions include discount rates,

health care cost trend rates, inflation, rates of compensation increase, expected return on plan assets, mortality

rates, and other factors. Actual results that differ from our assumptions are accumulated and amortized over

future periods and, therefore, generally affect our recognized expense and recorded obligation in such future

periods. We believe that the assumptions utilized in recording the obligations under our plans are reasonable, and

represent our best estimates, based on information as to historical experience and performance as well as other

factors that might cause future expectations to differ from past trends. Differences in actual experience or

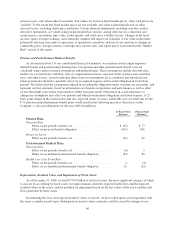

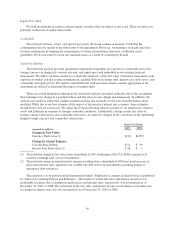

changes in assumptions may affect our pension and other postretirement obligations and future expense. A 25

basis point change in the assumed discount rate, expected return on assets, and health care cost trend rate for the

U.S. pension and postretirement benefit plans would result in the following increases (decreases) on the

Company’s costs and obligations for the year 2009 (in millions):

25 Basis Point

Increase

25 Basis Point

Decrease

Pension Plans

Discount Rate:

Effect on net periodic benefit cost .......................... $ (43) $ 77

Effect on projected benefit obligation ....................... (631) 656

Return on Assets:

Effect on net periodic benefit cost .......................... (41) 41

Postretirement Medical Plans

Discount Rate:

Effect on net periodic benefit cost .......................... (6) 5

Effect on accumulated postretirement benefit obligation ......... (83) 85

Health Care Cost Trend Rate:

Effect on net periodic benefit cost .......................... 4 (4)

Effect on accumulated postretirement benefit obligation ......... 21 (22)

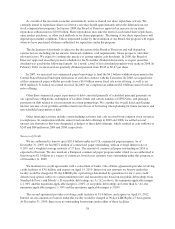

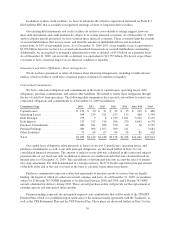

Depreciation, Residual Value, and Impairment of Fixed Assets

As of December 31, 2009, we had $17.979 billion of net fixed assets, the most significant category of which

is aircraft. In accounting for fixed assets, we make estimates about the expected useful lives and the expected

residual values of the assets, and the potential for impairment based on the fair values of the assets and the cash

flows generated by these assets.

In estimating the lives and expected residual values of aircraft, we have relied upon actual experience with

the same or similar aircraft types. Subsequent revisions to these estimates could be caused by changes to our

46