UPS 2005 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2005 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

the claim remains open, trends in health care costs and the results of related litigation. Furthermore, claims may

emerge in future years for events that occurred in a prior year at a rate that differs from previous actuarial

projections. Changes in state legislation with respect to workers compensation can affect the adequacy of our

self-insurance accruals. All of these factors can result in revisions to prior actuarial projections and produce a

material difference between estimated and actual operating results.

We sponsor a number of health and welfare insurance plans for our employees. We use estimates from third

party actuaries to establish the liabilities for these plans. These liabilities and related expenses are based on

estimates of the number of employees and eligible dependents covered under the plans, anticipated medical usage

by participants and overall trends in medical costs and inflation. Actual results may differ from these estimates

and, therefore, produce a material difference between estimated and actual operating results.

Pension and Postretirement Medical Benefits—Our pension and other postretirement benefit costs are

calculated using various actuarial assumptions and methodologies as prescribed by Statement of Financial

Accounting Standards No. 87, “Employers’ Accounting for Pensions” and Statement of Financial Accounting

Standards No. 106, “Employers’ Accounting for Postretirement Benefits Other than Pensions.” These

assumptions include discount rates, health care cost trend rates, inflation, rate of compensation increases,

expected return on plan assets, mortality rates, and other factors. Actual results that differ from our assumptions

are accumulated and amortized over future periods and, therefore, generally affect our recognized expense and

recorded obligation in such future periods. We believe that the assumptions utilized in recording the obligations

under our plans are reasonable based on input from our outside actuaries and other advisors and information as to

historical experience and performance. Differences in actual experience or changes in assumptions may affect

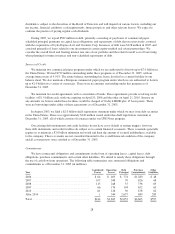

our pension and other postretirement obligations and future expense. A 25 basis point change in the assumed

discount rate, expected return on assets, and health care cost trend rate for the pension and postretirement benefit

plans would result in the following increases (decreases) on the Company’s costs and obligations for the year

2005 (in millions):

25 Basis Point

Increase

25 Basis Point

Decrease

Pension Plans

Discount Rate:

Effect on net periodic benefit cost .......................... $ (54) $ 55

Effect on projected benefit obligation ....................... (548) 571

Return on Assets:

Effect on net periodic benefit cost .......................... (26) 26

Postretirement Medical Plans

Discount Rate:

Effect on net periodic benefit cost .......................... (5) 5

Effect on projected benefit obligation ....................... (77) 79

Health Care Cost Trend Rate:

Effect on net periodic benefit cost .......................... 3 (2)

Effect on projected benefit obligation ....................... 22 (14)

Financial Instruments—As discussed in Notes 2, 3, 8, and 16 to our consolidated financial statements, and

in the “Market Risk” section of this report, we hold and issue financial instruments that contain elements of

market risk. Certain of these financial instruments are required to be recorded at fair value. Fair values are based

on listed market prices, when such prices are available. To the extent that listed market prices are not available,

fair value is determined based on other relevant factors, including dealer price quotations. Certain financial

instruments, including over-the-counter derivative instruments, are valued using pricing models that consider,

among other factors, contractual and market prices, correlations, time value, credit spreads, and yield curve

34