Toyota 2007 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2007 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

120 ANNUAL REPORT 2007

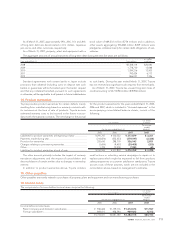

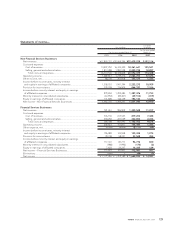

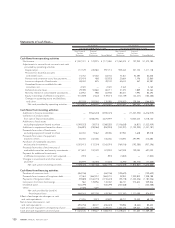

U.S. dollars

Yen in millions in millions

For the year

ended

For the years ended March 31, March 31,

2005 2006 2007 2007

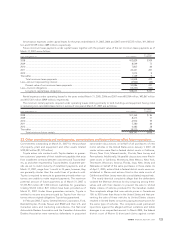

Minimum pension liability adjustments, included in other

comprehensive income...................................................................... ¥9,780 ¥4,937 ¥3,499 $29

The minimum pension liability recognized as of March 31, 2007 was eliminated upon the adoption of the provisions regarding

recognition of funded status and disclosure under FAS 158.

Weighted-average assumptions used to determine benefit obligations as of March 31, 2006 and 2007 are as follows:

March 31,

2006 2007

Discount rate ................................................................................................................................................ 2.6% 2.7%

Rate of compensation increase .................................................................................................................. 0.1–11.0% 0.1–10.0%

Weighted-average assumptions used to determine net periodic pension cost for the years ended March 31, 2005, 2006 and 2007

are as follows:

For the years ended March 31,

2005 2006 2007

Discount rate.......................................................................................................................... 2.2% 2.6% 2.6%

Expected return on plan assets ............................................................................................ 2.1% 2.9% 3.0%

Rate of compensation increase ............................................................................................ 0.5–9.7% 0.1–9.7% 0.1–11.0%

The estimated prior service costs, net actuarial loss and net

transition obligations that will be amortized from accumulated

other comprehensive income into net periodic pension cost

during the year ending March 31, 2008 are ¥(17,300) million

($(147) million), ¥3,400 million ($29 million) and ¥1,900 million

($16 million), respectively.

Prior to the adoption of the provisions regarding recognition

of funded status and disclosure under FAS 158 as of March 31,

2007, Toyota had recorded a minimum pension liability for

plans where the accumulated benefit obligation net of plan

assets exceeded the accrued pension and severance costs. The

minimum pension liability amount at March 31, 2006 was

¥43,980 million. Changes in the minimum pension liability are

reflected as adjustments in other comprehensive income for the

years ended March 31, 2005, 2006 and 2007 as follows:

The expected rate of return on plan assets is determined

after considering several applicable factors including, the com-

position of plan assets held, assumed risks of asset manage-

ment, historical results of the returns on plan assets, Toyota’s

principal policy for plan asset management, and forecasted

market conditions.

Toyota’s pension plan weighted-average asset allocations as

of March 31, 2006 and 2007, by asset category are as follows:

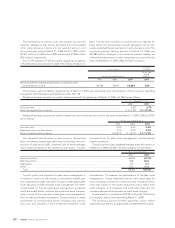

Toyota’s policy and objective for plan asset management is

to maximize returns on plan assets to meet future benefit pay-

ment requirements under risks which Toyota considers permissible.

Asset allocations under the plan asset management are deter-

mined based on Toyota’s plan asset management guidelines

which are established to achieve the optimized asset composi-

tions in terms of the long-term overall plan asset management.

Prior to making individual investments, Toyota performs in-depth

assessments of corresponding factors including risks, transac-

tion costs and liquidity of each potential investment under

consideration. To measure the performance of the plan asset

management, Toyota establishes bench mark return rates for

each individual investment, combines these individual bench

mark rates based on the asset composition ratios within each

asset category, and compares the combined rates with the

corresponding actual return rates on each asset category.

Toyota expects to contribute ¥132,447 million ($1,122 million)

to its pension plan in the year ending March 31, 2008.

The following pension benefit payments, which reflect

expected future service, as appropriate, are expected to be paid:

Plan assets at March 31,

2006 2007

Equity securities ........................................................................................................................................... 68.2% 67.2%

Debt securities ............................................................................................................................................. 18.8 20.8

Real estate .................................................................................................................................................... 0.5 0.7

Other ........................................................................................................................................................... 12.5 11.3

Total .......................................................................................................................................................... 100.0% 100.0%