Saks Fifth Avenue 2010 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2010 Saks Fifth Avenue annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

|

|

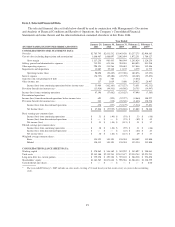

$87.5 million. The Company had $412.4 million of availability under the facility as of January 29, 2011. The

availability is based primarily on current levels of inventory, less outstanding letters of credit. The amount of

cash on hand and borrowings under the facility are influenced by a number of factors, including sales, inventory

levels, vendor terms, the level of capital expenditures, cash requirements related to financing instruments, and the

Company’s tax payment obligations, among others.

CAPITAL STRUCTURE

The Company continuously evaluates its debt-to-capitalization ratio in light of business and economic

trends, interest rate levels, and the terms, conditions and availability of capital in the capital markets. As of

January 29, 2011, the Company’s capital and financing structure was comprised of a revolving credit agreement,

senior unsecured notes, convertible senior unsecured notes, and capital and operating leases. As of January 29,

2011, total funded debt (including the equity component of the convertible notes) was $549.3 million,

representing a decrease of $26.4 million from the balance of $575.7 million at January 30, 2010. This decrease in

debt was primarily the result of the payment of $22.9 million of senior notes that matured in December 2010, the

repurchase of $0.8 million of the Company’s 7.0% senior notes that mature in 2013, and a net decrease in capital

lease obligations of $2.7 million. Additionally, the debt-to-capitalization ratio decreased to 32.9% in 2010 from

36.1% in 2009.

Senior Revolving Credit Facility

As of January 29, 2011, the Company maintained a senior revolving credit facility maturing in 2013, which

is secured by inventory and certain third party credit card accounts receivable. Borrowings are limited to a

prescribed percentage of eligible inventories and receivables. There are no debt ratings-based provisions in the

revolving credit facility. The facility includes a fixed-charge coverage ratio requirement of 1.0 to 1.0 that the

Company is subject to only if availability under the facility becomes less than $87.5 million. As of January 29,

2011, the Company was not subject to the fixed charge coverage ratio requirement. The facility contains default

provisions that are typical for this type of financing, including a provision that would trigger a default of the

facility if a default were to occur in another debt instrument resulting in the acceleration of more than $20 million

in principal of that other instrument. Borrowings under the facility bear interest at a per annum rate of either

LIBOR plus a percentage ranging from 3.5% to 4.0%, or at the higher of the prime rate and federal funds rate

plus a percentage ranging from 2.5% to 3.0%. Letters of credit are charged a per annum fee equal to the then

applicable LIBOR borrowing spread (for standby letters of credit) or the applicable LIBOR spread minus 0.50%

(for documentary or commercial letters of credit). The Company also pays an unused line fee ranging from 0.5%

to 1.0% per annum on the average daily unused revolver.

As of January 29, 2011, the Company had no outstanding borrowings under the revolving credit facility.

The senior revolving credit facility has a maximum capacity of $500 million.

Senior Notes

As of January 29, 2011, the Company had $145.6 million of senior notes outstanding, excluding the

convertible notes, comprising three separate series having maturities ranging from 2011 to 2019 and interest rates

ranging from 7.00% to 9.88%, of which $141.6 million mature in October 2011. The terms of each senior note

call for all principal to be repaid at maturity. The senior notes have substantially identical terms except for the

maturity dates and interest rates payable to investors. There are no financial covenants or debt-rating triggers

associated with these notes and each senior note contains limitations on the amount of secured indebtedness the

Company may incur.

In December 2010, the Company paid $22.9 million upon maturity of its 7.5% senior notes.

In May 2010, the Company repurchased $0.8 million of its 7% senior notes that mature in December 2013.

The repurchase of these notes resulted in an immaterial loss on extinguishment of debt.

28