Quest Diagnostics 2008 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2008 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

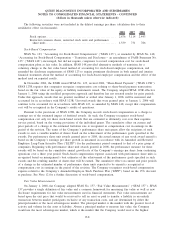

The following securities were not included in the diluted earnings per share calculation due to their

antidilutive effect (in thousands):

2008 2007 2006

Stock options....................................................... 2,676 3,114 2,443

Restricted common shares, restricted stock units and performance

share units ....................................................... 1,339 731 786

Stock-Based Compensation

SFAS No. 123, “Accounting for Stock-Based Compensation” (“SFAS 123”), as amended by SFAS No. 148,

“Accounting for Stock-Based Compensation – Transition and Disclosure – an amendment of FASB Statement No.

123” (“SFAS 148”) encouraged, but did not require, companies to record compensation cost for stock-based

compensation plans at fair value. In addition, SFAS 148 provided alternative methods of transition for a

voluntary change to the fair value based method of accounting for stock-based employee compensation, and

amended the disclosure requirements of SFAS 123 to require prominent disclosures in both annual and interim

financial statements about the method of accounting for stock-based employee compensation and the effect of the

method used on reported results.

In December 2004, the FASB issued SFAS No. 123, revised 2004, “Share-Based Payment” (“SFAS 123R”).

SFAS 123R requires that companies recognize compensation cost relating to share-based payment transactions

based on the fair value of the equity or liability instruments issued. The Company adopted SFAS 123R effective

January 1, 2006 using the modified prospective approach and therefore has not restated results for prior periods.

Under this approach, awards that are granted, modified or settled after January 1, 2006 will be measured and

accounted for in accordance with SFAS 123R. Unvested awards that were granted prior to January 1, 2006 will

continue to be accounted for in accordance with SFAS 123, as amended by SFAS 148, except that compensation

cost will be recognized in the Company’s results of operations.

Pursuant to the provisions of SFAS 123R, the Company records stock-based compensation as a charge to

earnings net of the estimated impact of forfeited awards. As such, the Company recognizes stock-based

compensation cost only for those stock-based awards that are estimated to ultimately vest over their requisite

service period, based on the vesting provisions of the individual grants. The cumulative effect on current and

prior periods of a change in the estimated forfeiture rate is recognized as compensation cost in earnings in the

period of the revision. The terms of the Company’s performance share unit grants allow the recipients of such

awards to earn a variable number of shares based on the achievement of the performance goals specified in the

awards. For performance share unit awards granted prior to 2008, the actual amount of any stock award earned is

based on the Company’s earnings per share growth as measured in accordance with its Amended and Restated

Employee Long-Term Incentive Plan (“ELTIP”) for the performance period compared to that of a peer group of

companies. Beginning with performance share unit awards granted in 2008, the performance measure for these

awards will be based on the cumulative annual growth rate of the Company’s earnings per share from continuing

operations over a three year period. Stock-based compensation expense associated with performance share units is

recognized based on management’s best estimates of the achievement of the performance goals specified in such

awards and the resulting number of shares that will be earned. The cumulative effect on current and prior periods

of a change in the estimated number of performance share units expected to be earned is recognized as

compensation cost in earnings in the period of the revision. The Company recognizes stock-based compensation

expense related to the Company’s Amended Employee Stock Purchase Plan (“ESPP”) based on the 15% discount

at purchase. See Note 12 for a further discussion of stock-based compensation.

Fair Value Measurements

On January 1, 2008, the Company adopted SFAS No. 157, “Fair Value Measurements” (“SFAS 157”). SFAS

157 provides a single definition of fair value and a common framework for measuring fair value as well as new

disclosure requirements for fair value measurements used in financial statements. Fair value measurements are

based upon the exit price that would be received to sell an asset or paid to transfer a liability in an orderly

transaction between market participants exclusive of any transaction costs, and are determined by either the

principal market or the most advantageous market. The principal market is the market with the greatest level of

activity and volume for the asset or liability. Absent a principal market to measure fair value, the Company

would use the most advantageous market, which is the market that the Company would receive the highest

F-8

QUEST DIAGNOSTICS INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(dollars in thousands unless otherwise indicated)