Quest Diagnostics 2008 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2008 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

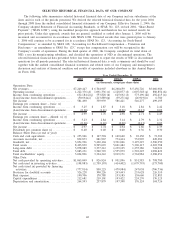

information technology. Clinical testing is generally categorized as clinical laboratory testing and anatomic

pathology services. Clinical laboratory testing is performed on blood and body fluids, such as urine. Anatomic

pathology services are performed on tissues, such as biopsies, and other samples, such as human cells. With the

acquisition of AmeriPath Group Holdings, Inc. (“AmeriPath”) in May 2007, we have become the world’s premier

cancer diagnostics company, focused on anatomic pathology including dermatopathology and molecular

diagnostics and are now able to provide interpretive consultation through the largest medical and scientific staff

in the industry, with approximately 900 M.D.s and Ph.D.s primarily located in the United States. In addition, we

are the leading provider of gene-based testing and other esoteric testing, risk assessment services for the life

insurance industry and testing for drugs-of-abuse. We are also a leading provider of testing for clinical trials. The

Company’s diagnostics products business, which includes the operations of HemoCue, Enterix and certain of

Focus Diagnostics’ operations, manufactures and markets diagnostic test kits and specialized point-of-care testing.

Through our MedPlus subsidiary, we empower healthcare organizations and clinicians with state-of-the-art

information technology solutions that can improve patient care and medical practice.

We have established operations in Gurgaon, India, where we will offer many of our services. The diagnostic

testing business in India is poised for rapid expansion. We see significant opportunities for us to strengthen the

delivery of healthcare services in India utilizing our quality diagnostics and technology expertise.

Six Sigma and Standardization Initiatives/Efforts to Improve Operating Efficiency

The diagnostic testing industry is labor intensive. Employee compensation and benefits constitute

approximately one-half of our total costs and expenses. Cost of services consists principally of costs for

obtaining, transporting and testing specimens. Selling, general and administrative expenses consist principally of

the costs associated with our sales and marketing efforts, billing operations (including bad debt expense), and

general management and administrative support. In addition, performing diagnostic testing involves significant

fixed costs for facilities and other infrastructure required to obtain, transport and test specimens. Therefore,

relatively small changes in volume can have a significant impact on profitability in the short-term.

A large portion of our costs are fixed, making it more challenging to fully mitigate the profit impact of lost

volume in the short term. In July 2007, we announced a program to adjust our cost structure while maintaining

and, in some cases improving, service levels. During 2008, we continued to take actions which have enabled us

to improve margins as a percentage of revenues over the course of the year and achieve a level which exceeded

that of the prior year. As we exited 2008, we estimate that our program has resulted in over $300 million of

annualized cost reductions, and we expect that our program will result in $500 million of annualized cost

reductions as we exit 2009.

We intend to become recognized as the quality leader in the healthcare services industry through utilizing

the Six Sigma approach and Lean Six Sigma principles. Six Sigma is a management approach that enhances

quality and requires a thorough understanding of customer needs and experience, root cause analysis, process

improvements and rigorous tracking and measuring of key metrics. Lean Six Sigma streamlines processes and

eliminates waste. We utilize the Six Sigma approach and Lean Six Sigma principles to increase the efficiency of

our operations and to reduce operating cost. We have utilized Six Sigma to implement the initiatives which are

part of our cost reduction program and provide a better customer experience. These initiatives relate to

standardizing our operations and processes, and adopting identified company best practices. One of these key

initiatives is to deploy Lean Six Sigma in our laboratories to realize productivity gains. Additionally, we expect

to realize efficiencies in other areas by better aligning our service capacity with patient and sample flows. We

are driving more of our purchasing through master contracts to take better advantage of our scale. We are

expanding the use of customer connectivity which reduces costs in specimen data entry and billing, and helps

lower our bad debt. We are improving the efficiency of our logistics routes using advanced route optimization

tools and we have streamlined our management structure and administrative functions to improve efficiency and

increase focus. As additional detailed plans to implement these opportunities are approved and executed, some

will result in charges to earnings associated with the implementation. These charges may be material to the

results of operations and cash flows in the periods recorded or paid.

Recent Acquisitions

The clinical testing industry in the United States remains fragmented and highly competitive. Our growth

will be comprised of a combination of organic and acquired growth. We expect to continue to selectively

evaluate potential acquisitions of domestic clinical laboratories that can be integrated into our existing

laboratories, thereby increasing access for patients and enabling us to reduce costs and improve efficiencies.

While over the long term we believe positive industry factors in the United States diagnostic testing industry and

44