Pep Boys 2014 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2014 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 31, 2015, February 1, 2014 and February 2, 2013

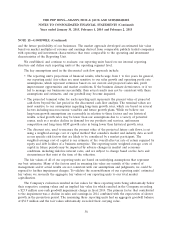

NOTE 16—INTEREST RATE SWAP AGREEMENT (Continued)

subsequent to the previous interest rate swap’s settlement, on October 11, 2012, the Company entered

into two new interest rate swaps for a notional amount of $50.0 million each that together are

designated as a cash flow hedge on the first $100.0 million of the amended and restated Term Loan.

The Company uses interest rate swap agreements to hedge the variability in cash flows related to

interest payments. The interest rate swaps convert the variable LIBOR portion of the interest payments

due on the first $100.0 million of the Term Loan to a fixed rate of 1.86%. As of January 31, 2015 and

February 1, 2014, the fair value of the new swap was a net $0.6 million liability and a net $0.6 million

asset, respectively, recorded within other long-term liabilities and other long-term assets on the balance

sheet.

The Company’s refinancing of the $200.0 million Term Loan on November 12, 2013, which lowered

the interest rate payable by the Company from LIBOR, subject to a 1.25% floor plus 3.75%, to

LIBOR, subject to a 1.25% floor plus 3.00%, had no impact on the Company’s interest rate swap or

hedge accounting.

NOTE 17—FAIR VALUE MEASUREMENTS

The Company’s fair value measurements consist of (a) non-financial assets and liabilities that are

recognized or disclosed at fair value in the Company’s financial statements on a recurring basis (at least

annually) and (b) all financial assets and liabilities.

Fair value is defined as the exit price, or the amount that would be received to sell an asset or

paid to transfer a liability in an orderly transaction between market participants as of the measurement

date. There is a hierarchy for inputs used in measuring fair value that maximizes the use of observable

inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be

used when available. Observable inputs are inputs market participants would use in valuing the asset or

liability developed based on market data obtained from sources independent of the Company.

Unobservable inputs are inputs that reflect the Company’s assumptions about the factors market

participants would use in valuing the asset or liability developed based upon the best information

available in the circumstances. The hierarchy is broken down into three levels. Level 1 inputs are

quoted prices (unadjusted) in active markets for identical assets or liabilities. Level 2 inputs include

quoted prices for similar assets or liabilities in active markets. Level 3 inputs are unobservable inputs

for the asset or liability. Categorization within the valuation hierarchy is based upon the lowest level of

input that is significant to the fair value measurement.

Assets and Liabilities that are Measured at Fair Value on a Recurring Basis:

The Company’s long-term investments and interest rate swap agreements are measured at fair

value on a recurring basis. The information in the following paragraphs and tables primarily addresses

matters relative to these assets and liabilities.

Cash equivalents:

Cash equivalents, other than credit card receivables, include highly liquid investments with an

original maturity of three months or less at acquisition. The Company carries these investments at fair

65