Pep Boys 2014 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2014 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 31, 2015, February 1, 2014 and February 2, 2013

NOTE 1—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

ASU 2013-11 states that an unrecognized tax benefit should be presented in the financial statements as

a reduction to a deferred tax asset for a net operating loss carryforward or a tax credit carryforward, if

available at the reporting date under the applicable tax law to settle any additional income taxes that

would result from the disallowance of a tax position. If the tax law of the applicable jurisdiction does

not require the entity to use, and the entity does not intend to use, the deferred tax asset for such

purpose, the unrecognized tax benefit should be presented in the financial statements as a liability. The

amendments in this ASU are effective for fiscal years, and interim periods within those years, beginning

after December 15, 2013. The adoption of ASU 2013-11 did not have a material impact on the

Company’s consolidated financial statements.

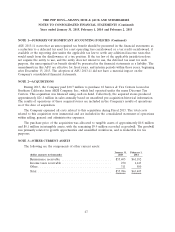

NOTE 2—ACQUISITIONS

During 2013, the Company paid $10.7 million to purchase 18 Service & Tire Centers located in

Southern California from AKH Company, Inc., which had operated under the name Discount Tire

Centers. This acquisition was financed using cash on hand. Collectively, the acquired stores produced

approximately $26.1 million in sales annually based on unaudited pre-acquisition historical information.

The results of operations of these acquired stores are included in the Company’s results of operations

as of the date of acquisition.

The Company expensed all costs related to this acquisition during Fiscal 2013. The total costs

related to this acquisition were immaterial and are included in the consolidated statement of operations

within selling, general and administrative expenses.

The purchase price of the acquisition was allocated to tangible assets of approximately $0.8 million

and $0.1 million in intangible assets, with the remaining $9.9 million recorded as goodwill. The goodwill

was primarily related to growth opportunities and assembled workforces, and is deductible for tax

purposes.

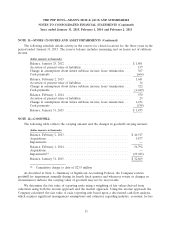

NOTE 3—OTHER CURRENT ASSETS

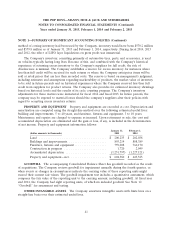

The following are the components of other current assets:

January 31, February 1,

(dollar amounts in thousands) 2015 2014

Reinsurance receivable ............................ $55,405 $61,182

Income taxes receivable ............................ 270 1,643

Other ......................................... 311 580

Total ......................................... $55,986 $63,405

47