Panera Bread 2015 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2015 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

34

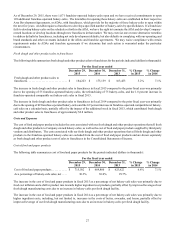

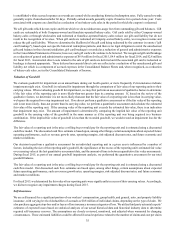

Revolving Credit Agreements

On November 30, 2012, we entered into a credit agreement, or the 2012 Credit Agreement, with Bank of America, N.A. and other

lenders party thereto. The 2012 Credit Agreement provided for an unsecured revolving credit facility of $250 million that would

have become due on November 30, 2017. As of December 30, 2014, we had no balance outstanding under the 2012 Credit

Agreement. On July 16, 2015, we terminated the 2012 Credit Agreement and entered into a new credit agreement, or the 2015

Credit Agreement, with Bank of America, N.A., as administrative agent, swing line lender and L/C issuer, and each lender from

time to time party thereto. The 2015 Credit Agreement provides for an unsecured revolving credit facility of $250 million that

will become due on July 16, 2020, subject to acceleration upon certain specified events of default, including breaches of

representations or covenants, failure to pay other material indebtedness or a change of control, as defined in the 2015 Credit

Agreement. We may select interest rates under the credit facility equal to, at our option, (1) the Eurodollar rate plus a margin

ranging from 1.00 percent to 1.50 percent depending on our consolidated leverage ratio or (2) the highest of (a) the Bank of America

prime rate, (b) the Federal funds rate plus 0.50 percent or (c) the Eurodollar rate plus 1.00 percent, plus a margin ranging from

0.00 percent to 0.50 percent depending on our consolidated leverage ratio. Our obligations under the 2015 Credit Agreement are

guaranteed by certain of our direct and indirect subsidiaries. The 2015 Credit Agreement allows us from time to time to request

that the credit facility be further increased by an amount not to exceed, in the aggregate, $150 million, subject to the arrangement

of additional commitments with financial institutions acceptable to us and Bank of America. As of December 29, 2015, we had

no balance outstanding under the 2015 Credit Agreement.

The 2014 Term Loan Agreement, 2015 Term Loan Agreement and 2015 Credit Agreement contain customary affirmative and

negative covenants, including covenants limiting liens, dispositions, fundamental changes, investments, indebtedness, and certain

transactions and payments. In addition, such term loan and credit agreements contain various financial covenants that, among

other things, require us to satisfy two financial covenants at the end of each fiscal quarter: (1) a consolidated leverage ratio less

than or equal to 3.00 to 1.00, and (2) a consolidated fixed charge coverage ratio of greater than or equal to 2.00 to 1.00. As of

December 29, 2015, we were, and expect to remain, in compliance with all covenant requirements.

Critical Accounting Policies & Estimates

Our discussion and analysis of our consolidated financial condition and results of operations is based upon the consolidated

financial statements and notes to the consolidated financial statements, which have been prepared in accordance with generally

accepted accounting principles in the United States of America, or GAAP. The preparation of the consolidated financial statements

requires us to make estimates, judgments and assumptions, which we believe to be reasonable, based on the information available.

These estimates and assumptions affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosures

of contingent assets and liabilities. Variances in the estimates or assumptions used to actual experience could yield materially

different accounting results. On an ongoing basis, we evaluate the continued appropriateness of our accounting policies and

resulting estimates to make adjustments we consider appropriate under the facts and circumstances.

We have chosen accounting policies we believe are appropriate to report accurately and fairly our consolidated operating results

and financial position, and we apply those accounting policies in a consistent manner. We consider our policies on accounting

for revenue recognition, valuation of goodwill, self-insurance, income taxes, lease obligations, and impairment of long-lived assets

to be the most critical in the preparation of the consolidated financial statements because they involve the most difficult, subjective,

or complex judgments about the effect of matters that are inherently uncertain. There have been no material changes to our

application of critical accounting policies and significant judgments and estimates that occurred during fiscal 2015.

Revenue Recognition

We recognize revenues from net bakery-cafe sales upon delivery of the related food and other products to the customer. Revenues

from fresh dough and other product sales to franchisees are recorded upon delivery of the fresh dough and other products to

franchisees. Sales of soup and other branded products sold outside our bakery-cafes are recognized upon delivery to customers.

Royalties are generally paid weekly based on a percentage of net franchisee sales specified in each ADA (generally five percent

of net sales). Royalties are recognized as revenue in the period in which the sales are reported to have occurred based on contractual

royalty rates applied to the net franchise sales. Franchise fees are generally the result of the sale of area development rights and

the sale of individual franchise locations to third parties. The initial franchise fee is typically $35,000 per bakery-cafe to be

developed under the ADA. Of this fee, $5,000 is generally paid at the time of signing of the ADA and is recognized as revenue

when it is received as it is non-refundable and we have to perform no other service to earn this fee. The remainder of the fee is

paid at the time an individual franchise agreement is signed and is recognized as revenue upon the opening of the corresponding

bakery-cafe. Franchise fees also include information technology-related fees for access to and the usage of proprietary systems.

We maintain a customer loyalty program through which customers earn rewards based on registration in the program and purchases

at our bakery-cafes. We record the full retail value of loyalty program rewards as a reduction of net bakery-cafe sales and a liability