Oracle 2008 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2008 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

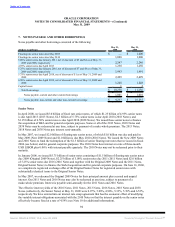

ORACLE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

May 31, 2009

Business Combinations: In December 2007, the FASB issued Statement No. 141 (revised 2007), Business

Combinations. The standard changes the accounting for business combinations including the measurement of

acquirer shares issued in consideration for a business combination, the recognition of contingent

consideration, the accounting for pre-acquisition gain and loss contingencies, the recognition of capitalized

in-process research and development, the accounting for acquisition related restructuring liabilities, the

treatment of acquisition related transaction costs, and the accounting for income tax valuation allowances and

other income tax uncertainties, amongst other impacts. In April 2009, the FASB issued FSP

No. FAS 141(R)-1 Accounting for Assets Acquired and Liabilities Assumed in a Business Combinations That

Arise from Contingencies. FSP No. FAS 141(R)-1 amends and clarifies the accounting for acquired

contingencies and is effective upon the adoption of Statement 141(R). We will adopt Statement 141(R) and

the related Staff Position in fiscal 2010 and believe that the adoption of Statement 141(R) will result in the

recognition of certain types of expenses in our results of operations that were previously capitalized pursuant

to pre-adoption accounting standards, amongst other potential impacts. A discussion of the more significant

items of Statement 141(R) that could materially affect our consolidated financial statements and our

accounting policy for these items is included in our discussion of “Significant Accounting Policies—Business

Combinations” above.

Accounting and Reporting of Noncontrolling Interests: In December 2007, the FASB issued Statement

No. 160, Noncontrolling Interests in Consolidated Financial Statements, an amendment of ARB No. 51. In

fiscal 2010, we will adopt Statement 160 and generally believe it will not materially affect our consolidated

financial statements. Upon our adoption of Statement 160, we will retrospectively classify noncontrolling

(minority) interest positions of consolidated entities as a separate component of consolidated stockholders’

equity from the equity attributable to Oracle’s stockholders for all periods presented. Net income and

comprehensive income will be attributed to Oracle stockholders and the noncontrolling interests. In addition,

Statement 160 requires that any change in our ownership of a majority-owned subsidiary be prospectively

accounted for as an equity transaction provided that we retain control of the subsidiary. This requirement is a

change to current practice whereby gains or losses may be recognized on the sales of our interests in a

subsidiary, regardless of whether we maintain control. While we have not recognized any material gains or

losses on such ownership sales during fiscal 2009, 2008 or 2007, the timing and amount of any future gains or

losses on sales of our ownership interests in our subsidiaries could be materially affected as a result of our

fiscal 2010 adoption of Statement 160.

Fair Value Measurements: In September 2006, the FASB issued Statement No. 157, Fair Value

Measurements. Statement 157 defines fair value, establishes a framework for measuring fair value and

expands fair value measurement disclosures. In February 2008, the FASB issued FASB Staff Position

No. FAS 157-1, Application of FASB Statement No. 157 to FASB Statement No. 13 and Other Accounting

Pronouncements That Address Fair Value Measurements for Purposes of Lease Classification or

Measurement under Statement 13 and FASB Staff Position No. FAS 157-2, Effective Date of FASB Statement

No. 157. Collectively, the Staff Positions defer the effective date of Statement 157 to fiscal years beginning

after November 15, 2008 for nonfinancial assets and nonfinancial liabilities except for items that are

recognized or disclosed at fair value on a recurring basis at least annually, and amend the scope of Statement

157. In October 2008, the FASB issued FASB Staff Position FAS 157-3, Determining the Fair Value of a

Financial Asset When the Market for That Asset Is Not Active, which clarified the application of how the fair

value of a financial asset is determined when the market for that financial asset is inactive. FSP

No. FAS 157-3 was effective upon issuance, including prior periods for which financial statements had not

been issued. In April 2009, the FASB issued FASB Staff Position No. FAS 157-4, Determining Fair Value

When the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identifying

Transactions That Are Not Orderly. FSP FAS 157-4 amends Statement 157 to provide additional guidance on

determining fair value when the volume and level of activity for the asset or liability have significantly

decreased when compared with normal market activity for the asset or liability. FSP FAS 157-4 is effective

for interim and annual reporting periods ending after June 15, 2009 with early adoption permitted for periods

ending after March 15, 2009. As described in Note 4, we have adopted Statement 157 and the related FASB

staff positions except for FSP No. FAS 157-4 and those items specifically deferred under FSP

No. FAS 157-2. We do not believe the full

87

Source: ORACLE CORP, 10-K, June 29, 2009 Powered by Morningstar® Document Research℠