Oracle 2008 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2008 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

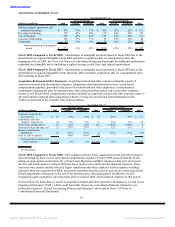

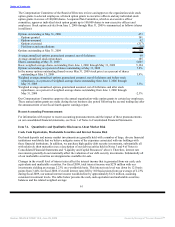

interest rates for our investment portfolio at May 31, 2009. The cash, cash equivalent and marketable

securities balances are recorded at their fair values at May 31, 2009.

May 31, 2009

Fair Value of

Available-for-Sale Weighted Average

(Dollars in millions) Securities Interest Rate

Cash and cash equivalents $ 8,995 0.83%

Marketable securities 3,629 1.14%

Total cash, cash equivalents and marketable securities $ 12,624 0.92%

Interest Expense Risk

Our borrowings as of May 31, 2009 were $10.2 billion, consisting of $9.2 billion of fixed rate borrowings and

$1.0 billion of floating rate senior notes that are due in May 2010 and bear interest at a floating rate equal to

three-month LIBOR plus 0.06% per year (0.97% at May 31, 2009). We have entered into an interest rate swap

arrangement to manage the economic effect of variable interest obligations associated with our 2010 floating

rate senior notes so that the interest payable on the senior notes effectively became fixed at a rate of 4.59%,

thereby reducing the impact of future interest rate changes on our future interest expense. We do not use

interest rate swap arrangements for trading purposes. The critical terms of the interest rate swap agreement

and the 2010 senior notes match, including the notional amounts, interest rate reset dates, maturity dates and

underlying market indices. Accordingly, we have designated the swap as a qualifying instrument and are

accounting for the swap as a cash flow hedge pursuant to FASB Statement No. 133, Accounting for

Derivative Instruments and Hedging Activities. The unrealized losses on the swap are included in

accumulated other comprehensive income and the corresponding fair value payable is included in other

current liabilities in our consolidated balance sheet. The periodic interest settlements, which occur at the same

interval as the interest payment and reset dates as the 2010 senior notes, are recorded as interest expense.

Foreign Currency Risk

Foreign Currency Transaction Risk

We transact business in various foreign currencies and have established a program that primarily utilizes

foreign currency forward contracts to offset the risks associated with the effects of certain foreign currency

exposures. Under this program, increases or decreases in our foreign currency exposures are offset by gains or

losses on the foreign currency forward contracts that we enter into to mitigate the possibility of foreign

currency transaction gains or losses. These foreign currency exposures typically arise from intercompany

sublicense fees and other intercompany transactions. Our forward contracts generally have terms of 90 days

or less. We do not use foreign currency forward contracts for trading purposes. All outstanding foreign

currency forward contracts are marked to market at the end of the period with unrealized gains and losses

resulting from fair value changes included in non-operating income, net (the effective portion of our Yen net

investment hedge described below is included in stockholders’ equity). Our ultimate realized gain or loss with

respect to currency fluctuations will depend on the currency exchange rates and other factors in effect as the

contracts mature. The notional amounts of foreign currency forward contracts to purchase and sell

U.S. Dollars in exchange for other major international currencies were $860 million and $1.1 billion,

respectively, and to purchase Euros in exchange for other major international currencies was €142 million

($198 million), as of May 31, 2009. The net unrealized gains of our outstanding foreign currency forward

contracts were $2 million at May 31, 2009. Net foreign exchange transaction (losses) gains included in

non-operating income, net in the accompanying consolidated statements of operations were $(65) million,

$17 million and $17 million in fiscal 2009, 2008 and 2007, respectively.

Foreign Currency Translation Risk

Fluctuations in foreign currencies impact the amount of total assets and liabilities that we report for our

foreign subsidiaries upon translation of these amounts into U.S. Dollars. In particular, the amount of cash,

cash equivalents and marketable securities that we report in U.S. Dollars for a significant portion of the cash

held by these

62

Source: ORACLE CORP, 10-K, June 29, 2009 Powered by Morningstar® Document Research℠