Nordstrom 2011 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2011 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

|

|

36

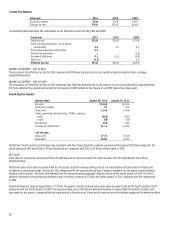

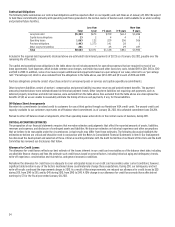

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

Dollars in millions

INTEREST RATE RISK

We are exposed to interest rate risk primarily from changes in short-term interest rates. As of January 28, 2012, we had cash and cash equivalents

of $1,877, which generate interest income at variable rates, and gross credit card receivables of $2,074, which generate finance charge income at a

combination of fixed and variable rates. Additionally, we have long-term debt of $3,647, including $500 that bears interest at floating LIBOR-based rates

and is scheduled to mature in April 2012. Interest rate fluctuations can affect our interest income, credit card revenues and interest expense. See Note 3:

Accounts Receivable and Note 8: Debt and Credit Facilities in Item 8 for additional information.

We use sensitivity analyses to measure and assess our interest rate risk exposure. For purposes of presenting the potential earnings effect

of a reasonably possible hypothetical change in interest rates from our reporting date, we utilized two sensitivity scenarios: (i) linear growth of

approximately 140 basis points over the year, and (ii) linear decline of approximately 20 basis points over the year, due to the fact that current interest

rates are at or near historically low levels. Other key parameters and assumptions in our sensitivity analyses include the average cash and cash

equivalents balance, average credit card receivables balance and no new floating rate debt issuance. The first hypothetical scenario would result in an

approximate $10 increase in future earnings, while the second hypothetical scenario would not have a material effect on future earnings.

We occasionally enter into interest rate swaps typically to convert fixed-rate debt to variable-rate debt. We did not have interest rate swaps on our debt

as of January 28, 2012, although we continue to amortize, as a reduction of interest expense, the remaining adjustment to long-term debt originating

from gains realized on previously designated fair value hedges. For our long-term fixed-rate debt, our exposure to interest rate changes is limited to

the change in fair value of the debt. As of January 28, 2012, the fair value of our fixed-rate debt was $3,652.

FOREIGN CURRENCY EXCHANGE RISK

The majority of our revenues, expenses and capital expenditures are transacted in U.S. dollars. However, we periodically enter into merchandise

purchase orders denominated primarily in Euros. From time to time we may use forward contracts to hedge against fluctuations in foreign currency

prices. As of January 28, 2012, we had no outstanding forward contracts.